A SWIFT Institute paper, A Critical and Empirical Examination of Currently-Used Financial Data Collection Processes and Standards, provides a framework for analyzing and assessing financial data standards and gives XBRL good marks.

The paper examines common financial data standards in use today: FIX, FpML, ISO 15022/ISO 20022, XBRL, and the US CFTC's Swaps Data Repositories' data. The authors endeavored to develop a framework to assess the quality of a data standard that would work across a variety of standards. Using that framework they evaluate each of these common financial data standards. XBRL received good marks particularly among the semantically complex standards.

The 37 page paper is worth reading. The paper shows a maturing of the way people think about standards. There are three noteworthy items I would like to point out:

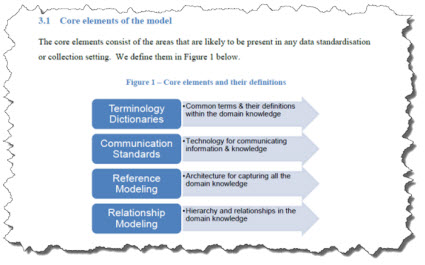

Core elements of the model

The core elements of the assessment model are terminology dictionaries, communications standards, reference modeling, and relationship modeling. This points out that things like the US GAAP XBRL Taxonomy are far more than "dictionaries" which is how the typical business professional thinks about such things.

(Click image to open paper at this section, page 10)

(Click image to open paper at this section, page 10)

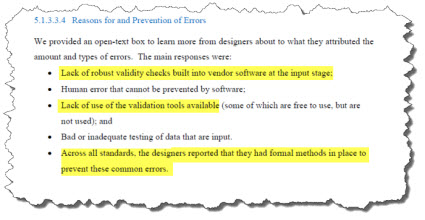

Reasons for and Prevention of Errors

The paper points out specific reasons for errors and how to prevent such errors which impact the quality of information and therefore impact the usefulness of information. The lack of validity checks by software vendors when information is being input tops the list of reasons for errors. Not using validity checks that do exist also made it to the list.

(Click image to open paper at this section, page 26)

(Click image to open paper at this section, page 26)

Stakeholder harmony vs dissonance

The paper provides excellent definitions of "harmony" and "dissonance" and explains the relationship between stakeholder harmony and information quality. A specific example will help one understand why this is extremely important. A common obstacle in the creation of a standard is agreeing on concepts and relations between concepts of the standard, the fundamental accounting concept relations is a good example of that. Overcoming disagreements between stakeholders and even within groups of stakeholders is important. Agreement between stakeholder groups and within stakeholder groups contributes to harmony. Lack of agreement contributes to dissonance.

So I refer to "stakeholder harmony vs dissonance" as a "communications problem". Stakeholders need a framework for agreeing. The paper does not explicitly define "stakeholder". I believe that what is meant by the term "stakeholder" is anyone that has a vested interest. Another term for stakeholder is "constituent". A "constituent" is a component part of something. A first step, if not the first step, of arriving at harmony is outlining the perceptions, positions, and risks of each constituency or stakeholder group.

Another important part is providing a conceptual framework for thinking about the system. For example, both US GAAP and IFRS have a conceptual framework for thinking about financial reporting. That includes a set of principles or assumptions or a world view. For example, accounting has a set of principles.

From a financial reporting perspective, this is why the XBRL-based digital financial reporting principles are important and why it is important for accounting professionals to understand knowledge engineering basics. This framework for agreeing which helps the communications process increases harmony and decreases dissonance. This is about bringing the system into balance, creating the appropriate equilibrium. Today, too many of the important moving parts are unconscious to stakeholder groups.

Tools such as the framework for assessing the quality of standards contribute to enabling business domains consciously moving to the appropriate equilibrium. Effectively working standards are important in today's digital age.