The FASB provides SFAC 6, Elements of Financial Statements, which instantiates and defines 10 classes of elements that are the building blocks of financial statements. In the FASB's own words:

Elements of financial statements are the building blocks with which financial statements are constructed—the classes of items that financial statements comprise.

Those financial statement element classes are: assets, liabilities, equity, comprehensive income, investments by owners, distributions to owners, revenues, expenses, gains, losses.

I have created an enhanced set of elements of financial statements. This is summarized in my document Enhanced US GAAP Financial Statement Elements. My enhanced set builds on what the FASB does, improving it in three ways:

- Machine-readable: It puts these concepts and their definitions in machine-readable form. The FASB only provides them in e-paper (i.e. PDF). I also provide the information in human-readable form.

- Mathematical associations: It puts the elements in context by showing the associations between the concepts.

- Add useful missing information: It adds additional important concepts that are ultimately defined implicitly or explicitly somewhere by the FASB to provide a complete set of core high-level financial report elements.

Basically, I provide a complete, explicit, and machine-readable foundation which can be built upon and leveraged. Here is the summary in both human-readable and machine-readable form:

- Human readable: (Human | Machine) This is a human-readable version you can browse and get an idea as to what is going on.

- Elements (terms) (Human | Machine): These are the elements of a financial statement.

- Associations (Human | Machine): These are the associations between the elements.

- Assertions (Human | Machine): These are the assertions that show the mathematical relations between the financial statement elements.

- Facts (Human | Machine): This is an instance (i.e. report) that tests the terms, associations, and assertions to both provide clarity and prove that everything is working as expected.

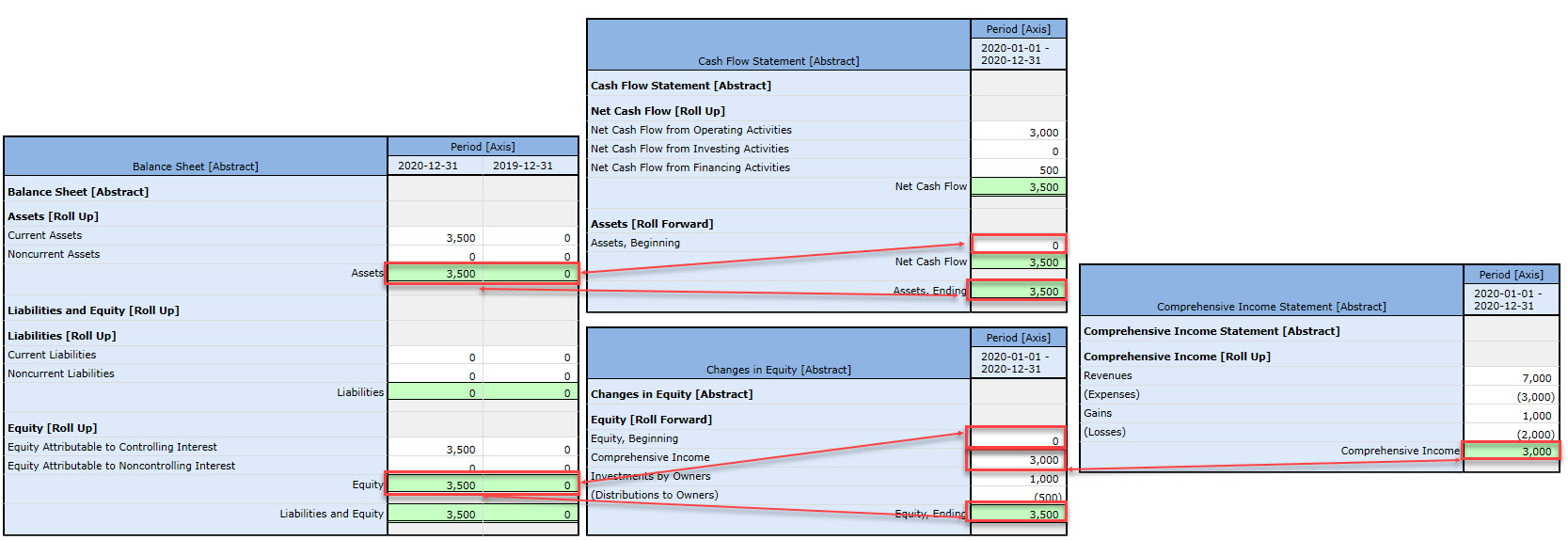

This graphic of the interconnections of the four primary financial statements helps you understand the relationships between the elements.

(Click image for a larger view)

There are a lot of advantages to having this information in machine-readable form. Read the document to understand.

Next up...IFRS, IPSAS, GAS, FRF for SMEs, FAS. Stay tuned! Here is a comparison of the elements of a financial report for a number of financial reporting schemes.