I have put together a mechanism for understanding, testing, and even agreeing on the meaning conveyed by an XBRL-based financial report and the underlying XBRL taxonomy for any financial reporting scheme. What I have done is take what I call my PROOF representation which I am calling a baseline representation and then represented that same meaning using the US GAAP XBRL Taxonomy information, the IFRS XBRL Taxonomy information, UK GAAP (FRS 102) XBRL Taxonomy, and Australian IFRS XBRL Taxonomy. Here are all representations: (to learn how to interpret these, please see this tutorial)

- PROOF BASELINE using my XBRL Taxonomy (Updated 2020-12-30)

- PROOF information represented using US GAAP XBRL Taxonomy (2019)

- PROOF information represented using IFRS XBRL Taxonomy (2020)

- PROOF information represented using UK GAAP (FRS 102) Taxonomy (2019) (work in progress)

- PROOF information represented using Australian (AU) IFRS XBRL Taxonomy (2020)

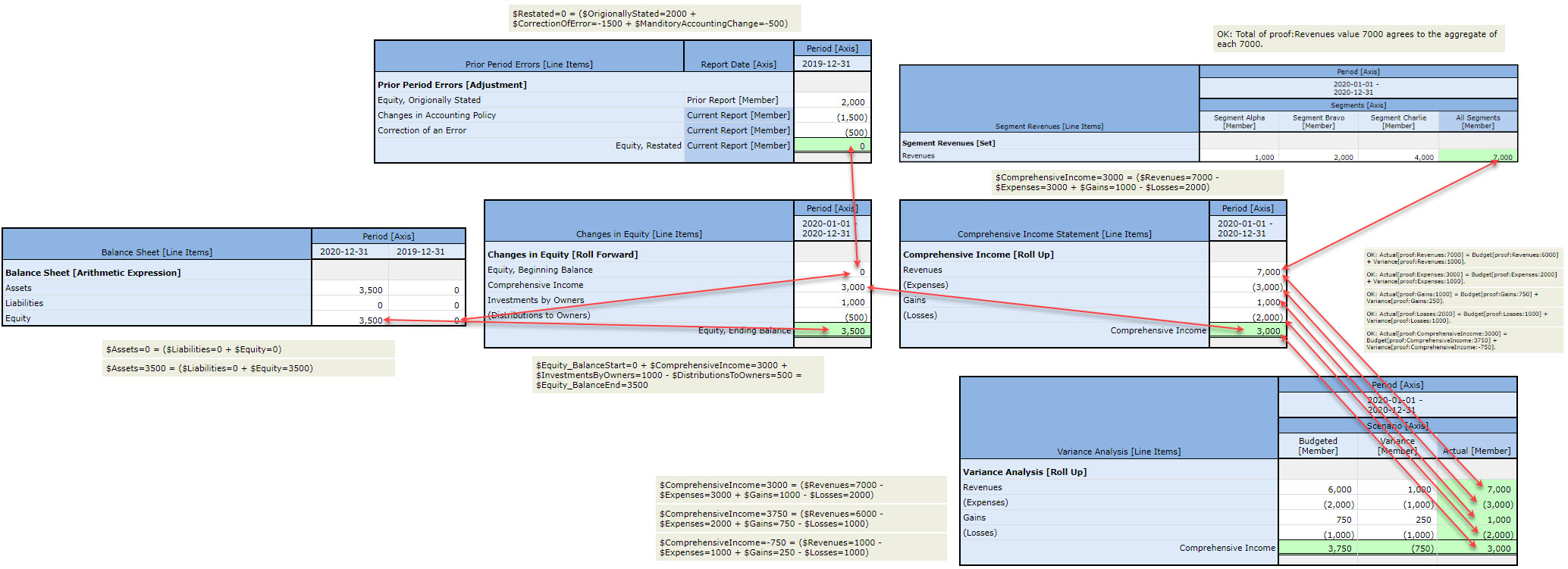

My focus is primarily on the mathematical connections between the different structures of a report. You can understand these relations if you are not an accountant via this graphic: (click the image for a larger view)

Understanding and expressing these mathematical needs to be provided for in XBRL-based taxonomies for financial reporting and not a guessing game that accountants must individually figure out. What I have works. There could be other ways to achieve everything I am achieving. You really cannot deny the use cases! All this will be represented in machine-readable form including the terms and rules (those are prototypes for US GAAP). This is what I have this far.

Roll ups tend to be pretty well understood by those creating XBRL-based financial reports. Roll forwards are probably well understood, but their are some idiosyncrasies people tend to miss. Member aggregations are less well understood. Adjustments which reconcile an originally stated balance to a restated balance seem to be misunderstood. Variance which reconciles an actual balance to a budget or forecast (i.e. a different reporting scenario). Effectively these are all sets of information that have some logical and mathematical relationship(s) within the set. There are a few other information patterns that exist in XBRL-based reports but tend to be less problematic.

All of these information patterns are explained in this document, Concept Arrangement Patterns, and this document, Member Arrangement Patterns.

More information coming with regard to this comparison/contrast of US GAAP and IFRS taxonomies and reconciling them to required financial reporting semantics.

#####################