When a system is working right, it creates a virtuous cycle.

The terms virtuous cycle and vicious cycle refer to complex chains of events that reinforce themselves through a feedback loop.

- A virtuous cycle has favorable results.

- A vicious cycle has detrimental results.

The Financial Accounting Foundation (FAF) uses the notion of a virtuous cycle and feedback loop to show the value of quality accounting standards and financial information that is clear, concise, comparable, relevant and representationally faithful:

The Financial Accounting Standards Board (FASB) uses the notion of a virtuous cycle to point out the value of technology to investors:

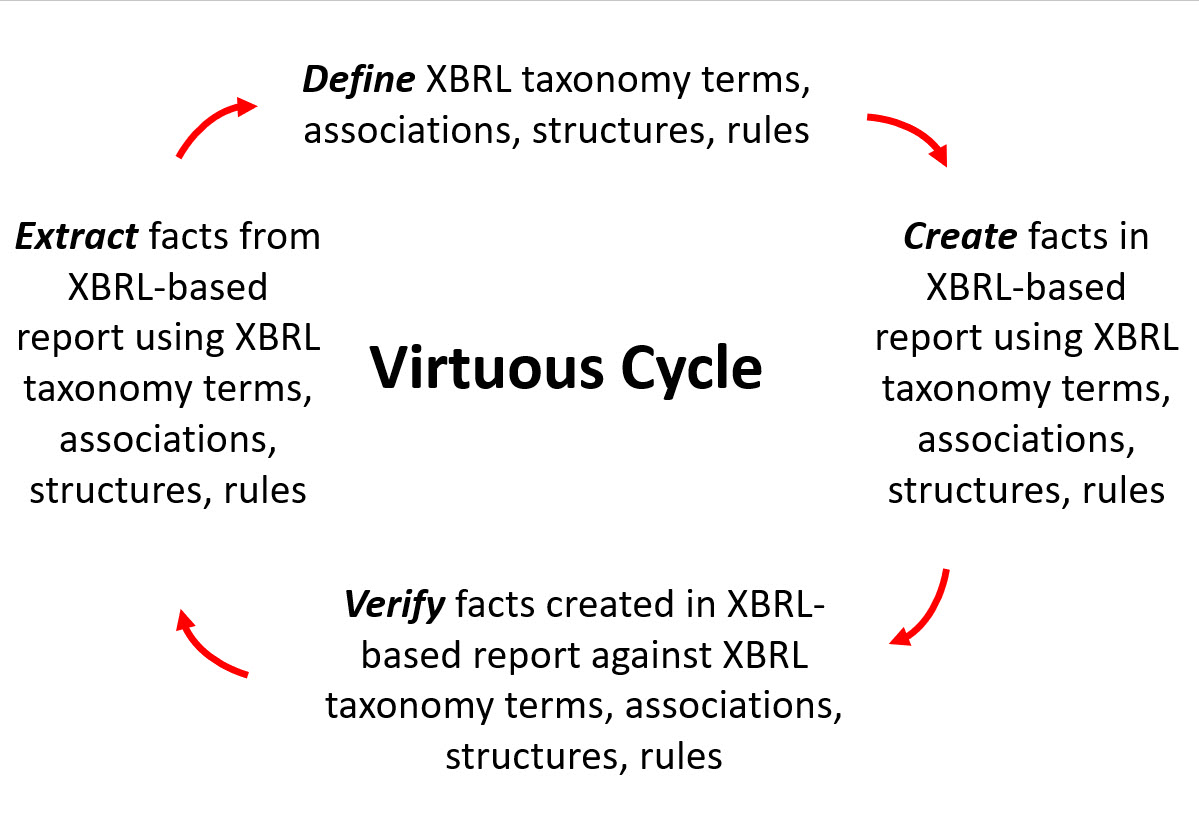

Here is another virtuous cycle to consider: a proper functioning financial report logical system. Here is what I mean.

I created a prototype XBRL taxonomy for financial reporting by a not-for-profit organization. My intension was to create everything that is necessary to help me make sure I created the report correctly. Rather than using a "pick list" type of approach that the US GAAP and IFRS XBRL taxonomies use; I used a model based approach. I considered all the dynamics that impact a financial report logical system.

What I found is that the system created in that manner provides a virtuous cycle, a feedback loop, that helps make defining XBRL taxonomies, creating reports, verifying reports, and extracting information from reports all work more effectively.

Rather than viewing these tasks as individual silos; if viewed as a system all this becomes quite obvious.

As authors Gerald C. Kane, Anh Nguyen Phillips, Jonathan R. Copulsky, and Garth R. Andrus point out in their book The Technology Fallacy, it is a myth that technology is behind digital transformation. People are behind such transformations. The authors define digital maturity as follows:

Digital maturity is primarily about people and the realization that effective digital transformation involves changes to organizational dynamics and how work gets done.

The technology and know-how exists to make XBRL-based digital financial reporting work effectively. The question is does the will exist. It really would not take much to turn the existing vicious cycle of quality problems related to XBRL-based financial reports submitted to the SEC into a virtuous cycle.

The question is not "if" this virtuous cycle will ever be created, it is more a matter of "when" and "who" will be the first.

This YouTube video, Virtuous Cycle, provides a bit more detail should you be interested.