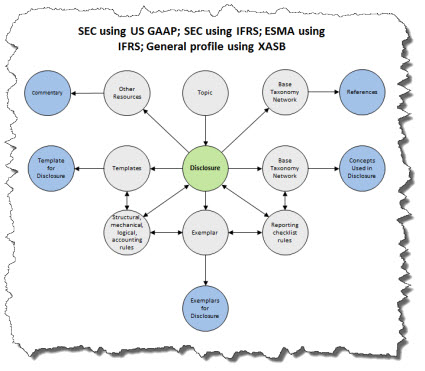

In a prior post, I pointed out the benefits of the notion of a "disclosure". I showed the diagram you see below.

I have expanded that diagram to include actual links to machine-readable metadata and in a separate diagram links to human-readable information that helps you better understand what the diagram is getting at better.

As you learned from reading the document Computer Empathy, computers don't work by magic. What seems to be magic is actually the result of attention to detail, good engineering, a good understanding of a domain of knowledge, and machine-readable metadata.

(Click image to navigate to machine-readable details)

(Click image to navigate to machine-readable details)

(Be sure not to miss the human-readable information. It will give you a sense of what is going on.)

I have been figuring out how to put the puzzle of financial reporting together for several years. The effort started long before Rene van Egmond and I wrote Financial Report Semantics and Dynamics Theory.

I have gone down some wrong paths that have led to dead ends. One dead end was OWL and RDF, basically trying to use the W3C semantic web stack. I found that path too complicated, too low-level, and something that could never be understood by professional accountants. Don't get me wrong, the W3C semantic web stack can work; but I could not make it work.

Another wrong path was creating what amounted to proprietary information formats. That works also, but it made things more complicated than they had to be and you lost the leverage offered by XBRL in some areas.

There were a few other dead ends.

But now, I have a very good framework where all machine-readable information is represented using the XBRL global standard. In my framework there is still one hold out that is represented in RSS. I could, and do, use an XBRL taxonomy schema to essentially provide a "list of options". An economic entity would use ONE item from that RSS list. XBRL does not really have a mechanism for articulating what it is that I want to articulate to the best of my knowledge; but I will check. For now, the single RSS file has to stay.

And so, now pretty much everything in my framework is global standard XBRL.

I added additional items to that "web" I showed in that first diagram. Now everything fits togeter. All the circles are connected but one. The only unconneced circle is the "Model Structure Rules". The reason the model structure rules are not connected is because those rules relate to the report level and not the financial reporting level like all the other information. Model structure relates to the allowed relations between Networks, Tables (hypercubes), Axis (dimensions), Members, Line Items, Concepts (primary items), and Abstracts.

Everything else is financial reporting related.

And while what I am showing in this first diagram relates to US GAAP; the same framework is used for IFRS and for the XASB reportring scheme which I use for testing and prototyping.

Not bad for a CPA. Fact is, there is no software engineer that understands financial reporting enough to do what I was able to do simply by paying attention to the information technology professionals. I honestly could not tell you the difference between "syntax" and "semantics" in 2007. But I fixed that problem by replacing my ignorance with knowledge.

I am now going to refactor the IFRS and XASB reporting scheme profiles to match the US GAAP profile.

Then, let the magic begin. Next step is to use all this metadata in software and show how XBRL-based digital financial reporting does not (a) have to be hard to use and (b) suffer from quality problems like the XBRL-based financial reports which are submitted to the SEC.

Time to disrupt financial reporting and build a modern finance platform because I am personally sick and tired of using outdated, even barbaric, approaches to creating financial reports.

Who else is with me? We have a small but growing group. If you are with me (i.e. you don't want to pave the same old goat path), please find the best information available on this page of my blog.

I still need to explain blocks better, stay tuned...that is next.