Understanding the Role of an [Axis] in an SEC XBRL Filing

If you look within SEC XBRL filings you can see that their creators still have confusion about what exactly an [Axis] does.

As explained in on the SEC XBRL Financial Filing Glossary and Logical Model, an axis is:

A means of providing information about the characteristics of a fact reported within a business report.

Nothing scary or technical about that explanation and that is all an axis really is. Now, some people refer to an axis or [Axis] as seen in XBRL taxonomies using other terms which can make them seem confusing. Some common terms are: dimension as used in the XBRL Dimensions specification, aspect as used in the XBRL Formulas specification, measure as used in the multidimensional model and in the Business Reporting Logical Model, to name most. I will use [Axis] as used in the US GAAP Taxonomy and in SEC XBRL financial filings.

But what exactly does an [Axis] do? Walking through this will make exactly what an [Axis]. Consider the following two facts:

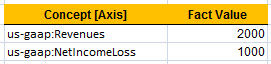

The two facts have values. What do those values mean? Well, you don't really know, you need more information. So, you add an [Axis] to provide additional characteristics. Now, consider this next screen shot:

So above, I added the Concept [Axis] and provided values for each fact to both explain and differentiate the two fact values. The value of an [Axis] is called a [Member]. We still don't have quite all of the information we need yet, this next screen show will make that clear:

So now we are getting closer and closer to something which is becoming useful. Knowing the period and the entity reporting the fact, in the case of SEC XBRL financial filings the CIK number, is commonly desired. In fact, it is so common that XBRL requires these three [Axis] on every single fact: the concept, the period, and the reporting entity.

But, do we have enough information? Well, that depends. Take a look at the next screen shot and we will bring up a few more things about an [Axis].

XBRL provides the ability to add even more, in fact any number of, [Axis]. Here we added the business segment [Axis] and indicated that our fact values both relate to the the consolidated entity.

When do you know if you have enough [Axis]? Well, that is dependent on whether you have communicated all the business information you are required to communicate. A fact is comprised of a value and all the characteristics which describe that value. There is nothing technical about what an [Axis] does so don't let a poor software implementation or some consultant who speaks using $150 an hour jargon tell you any differently. Yes, it really is that simple and straight forward.

Rather than complicating this explanation with more details, I will call this good. You can find more definitions of the report elementswhich make up an SEC XBRL financial filing in that same glossary.

I will go into some of the more common mistakes I am seeing in SEC XBRL financial filings later.

Charlie

in Modeling Business Information Using XBRL

|

Charlie

in Modeling Business Information Using XBRL

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments