Universal Digital Financial Reporting Framework

Welcome to a more modern era of accounting, reporting, auditing, and analysis! This will be an era of continuous accounting, continuous reporting, smart regulation, algorithmic regulation, artificial intelligence assisted audits, always on audit, computational professional services.

The Universal Digital Financial Reporting Framework is an XBRL-based approach to creating both human-readable and machine-readable general purpose financial statements. It is a de facto standard approach based on the best practices learned from creating XBRL-based reports which have been submitted to the SEC and the ESMA and attempting to extract information from the reports effectively. The framework uses the best practices and avoids the bad practices. The framework is proven and rigorously tested. The framework and method can be used to automate the entire record to report process.

Accounting was built for the computer age in 1211 AD, long before mechanical computers actually existed, by a bank in Florence which was the first to use the double entry accounting system. Friar Luca Pacioli was the first to document that double entry method in 1494 AD and the double entry method became wide spread, used around the world. Two advantages of double entry accounting had over single entry accounting were (a) superior error detection capabilities and (b) the ability to distinguish an unintentional error from an intentional error (i.e. fraud).

But it was not until electronic computers were invented that accounting had the machine driven environment it truly needed to take advantage of double entry accounting’s real features. Before electronic computers were invented, human “computers” entering transactions manually into paper ledgers. This was limiting.

To see the advantage computer accounting provided one need only look at the growth in global commerce since the computer was invented. Consider the size of global multinational enterprise today. Would that size of organization even be possible if computers did not exist? Very doubtful.

While the tools have changed, the mentality of the accountant has not really changed that much. Accountants continue to be constrained by their “paper-based” medieval thinking about how to approach financial accounting, reporting, auditing, and analysis. That mentality will eventually change. That change might be slow. But it will occur.

The Universal Digital Financial Reporting Framework is needed today so that accountants are not overwhelmed by the ever increasing volume and complexity of financial transactions.

Auditing is already broken, people just don’t seem to recognize that yet. Accountants might even be in denial. New ideas are necessary. The Fourth Industrial Revolution is a real thing.

To understand XBRL-based digital financial reporting it helps to think of it in terms of levels similar to how levels are helpful in understanding the capabilities of self driving cars. Here is an overview of the levels related to financial reporting as I see them: (An example of each level is provided and here are more details about the levels; this VIDEO explains the levels; this PDF presentation explains the levels)

- Level 0: Not machine readable.

- Level 1: Machine readable, nonstandard, structured for presentation.

- Level 2: Machine readable, nonstandard, structured for meaning, no taxonomy (a.k.a. dictionary), no rules, no report model.

- Level 3: Machine readable, global standard syntax, structured for meaning, with taxonomy (a.k.a. dictionary), incomplete rules, incomplete high-level report model. (Level3a shows XBRL calculations also removed)

- Level 4: Machine readable, global standard syntax, structured for meaning, with taxonomy (a.k.a. dictionary), complete set of rules provided, incomplete high-level report model.

- Level 5: Machine readable, global standard syntax, structured for meaning, with taxonomy (a.k.a. dictionary), complete set of rules provided, complete global standard high-level report model, yields PROVEN properly functioning system and UNDERSTANDABLE report information.

- Level 6: All of Level 5 PLUS blockchain-anchored XBRL to increase trust.

- Level 7: All of Level 6 PLUS blockchain-anchored transactions and events.

What is important to understand is that anything less than LEVEL 5 simply cannot work for financial reporting schemes like US GAAP, IFRS, UK GAAP. To understand why, read the Essence of Accounting.

Proof that Level 3 (incomplete set of rules) does not work is provided by my quarterly measurements for about six years, measurements provided by XBRLogic, measurements provided by XBRL Cloud, measurements provided by the XBRL US Data Quality Committee, Toppan Merrill urging companies to take quatliy seriously, and plenty of other information. Proof that Level 4 (incomplete high-level model) does not work can be understood by trying to extract information from XBRL-based reports.

For XBRL-based digital financial reporting to even get out of the gates and to be considered for use in the enterprise, it actually needs to work and it needs to provide some sort of benefit. "Bolting on" XBRL at the end of an already outdated work flow simply will not do the trick.

To learn more start with Essentials of XBRL-based Digital Financial Reporting.

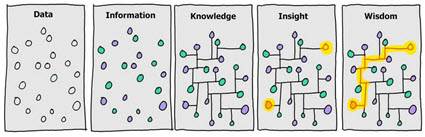

The excellent graphic below helps to explain the levels. Level 1 is like the "Data" image below. Level 5 is like "Knowledge" image. Levels 2, 3, and 4 relates to leaving out some important information or knowledge. It is only with Level 5 that you can achieve Insight and Wisdom.

################################

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments