Subjects, predicates, objects. Sentences, statements, arguments. Where do you start? The first step is to get the jargon correct. This website seems good, Sentence Basics.

There are several areas of knowledge that use the term "sentence" and "statement": linguistics, English, philosophy, computer science, logic. Other similar words are used to describe statements like "claim" and "proposition" and "assertion" and "declaration". Trying to sort this out can be confusing.

When you throw in the notion of "fact" and "opinion" all this becomes even more complicated for people to get their heads around.

Fundamentally, a statement is ONE TYPE of sentence. We are more interested in "statements" than "sentences". Here is why. A sentence is a group of words that usually have a subject, verb (a.k.a. predicate) and information about the subject. A sentence can be a question, a command, or a statement.

An argument is at least two sentences where one of the sentences is a conclusion. For example, "IF it is raining THEN you will get wet."

We are interested in the formal logical technical definition of statement. Here is information from a paper that distinguishes between sentences, statements, and arguments:

A statement is defined as that which is expressible by a sentence and is either true or false.

The criterion of being either true or false is one thing that served to identify the informative use of language. Questions, commands, performatives, and expressions of feeling are neither true nor false.

Statements are logical entities; sentences are grammatical entities.

Not all sentences express statements and some sentences may express more than one statement. A statement is a more abstract entity than even a sentence type. It is not identical with the sentence used to express it.

In this respect, a sentence is like a numeral and a statement is like a number. Each of the following can be used to express the same thing.

In logic, a statement is understood to be "a meaningful declarative sentence that is true or false, or a proposition which is the assertion that is made by (i.e., the meaning of) a true or false declarative sentence.

For our purposes, we need to understand that we are talking about logical statements that is a formal decarative sentence that is either true or false. This is important because once you understand what a logical statement is you can then begin to understand logical connections (logical operators) and logic gates.

Why is this important?

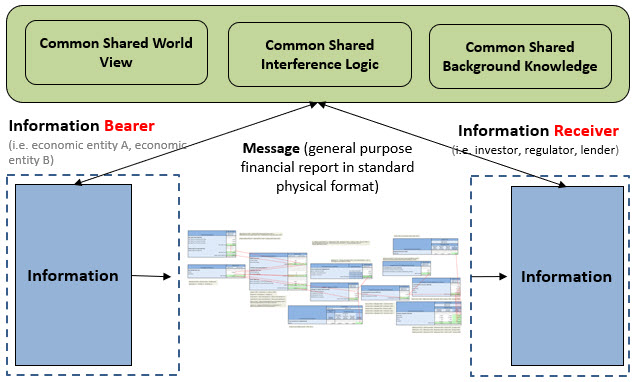

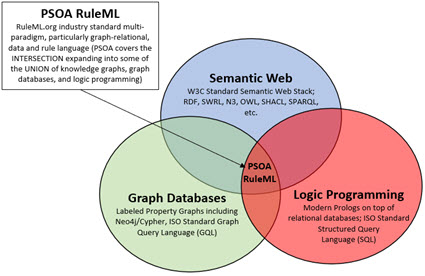

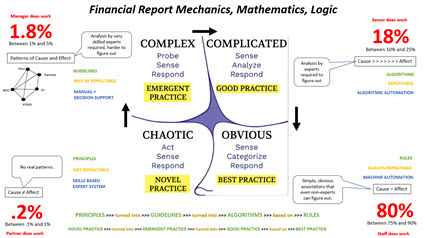

I refer to all this as Computational Professional Services. (There might be a better term, but that is the term I am currently using.

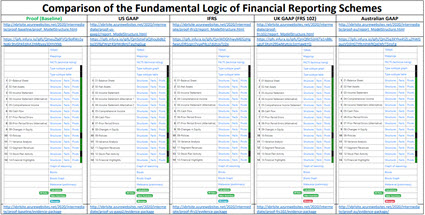

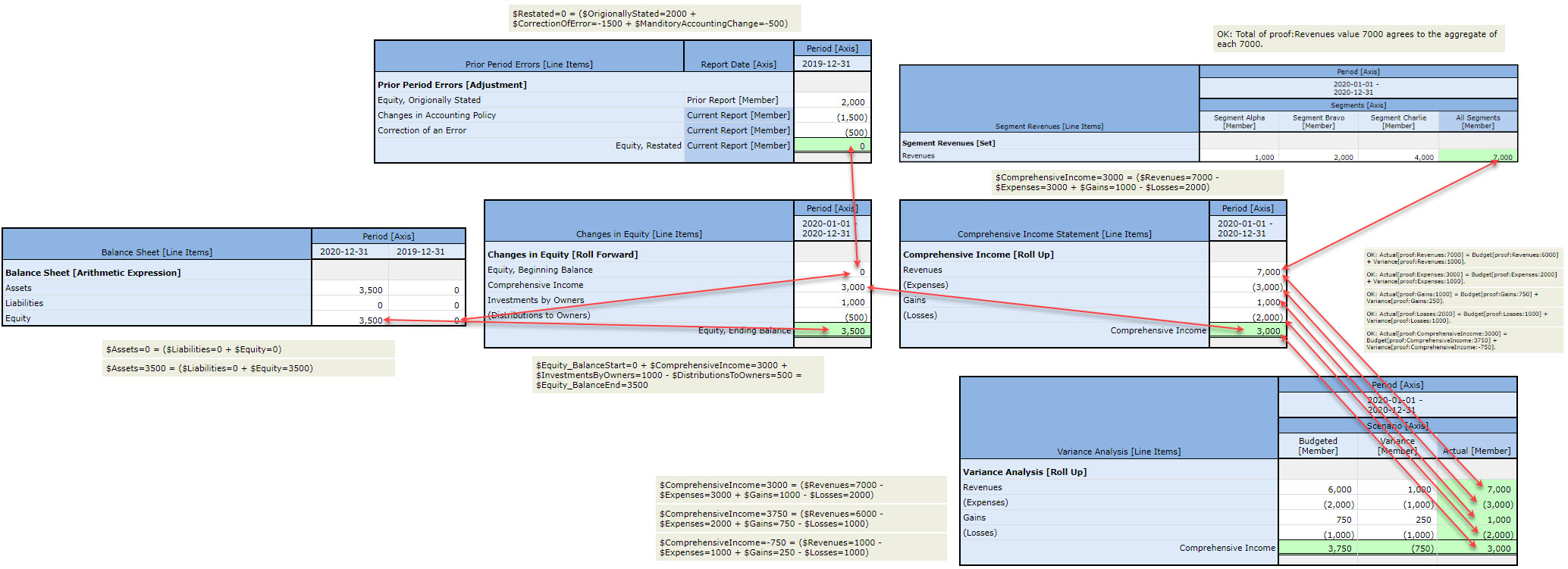

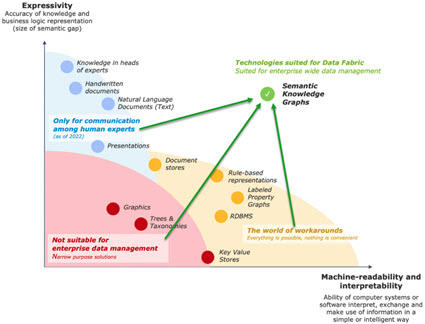

Financial accounting, reporting, auditing, and analysis is transitioning from analog to digital. For that to occur, knowledge in the heads of experts needs to be put into machine readable form by those experts. Machine learning will never create what needs to be created to make this work effectively. Yes, after a solid gounding has been created (training data) then machine learning can supplement that initial knowledge represented by knowledgable experts.

Express knowledge in machine readable form:

Implementation of knowledge graphs:

Extent to which knowledge can be represented in machine readable form: (sensemaking)

Which path will you take?

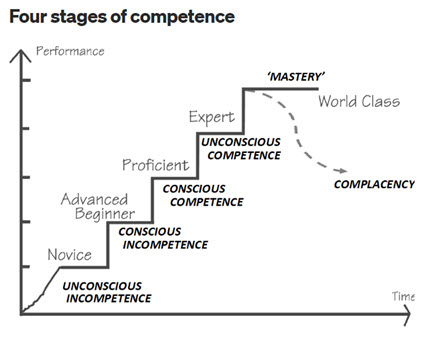

Start here! Take charge of your future. There are no short cuts.

]]>