Reporting Approaches + XBRL Approaches + Implementation Approaches

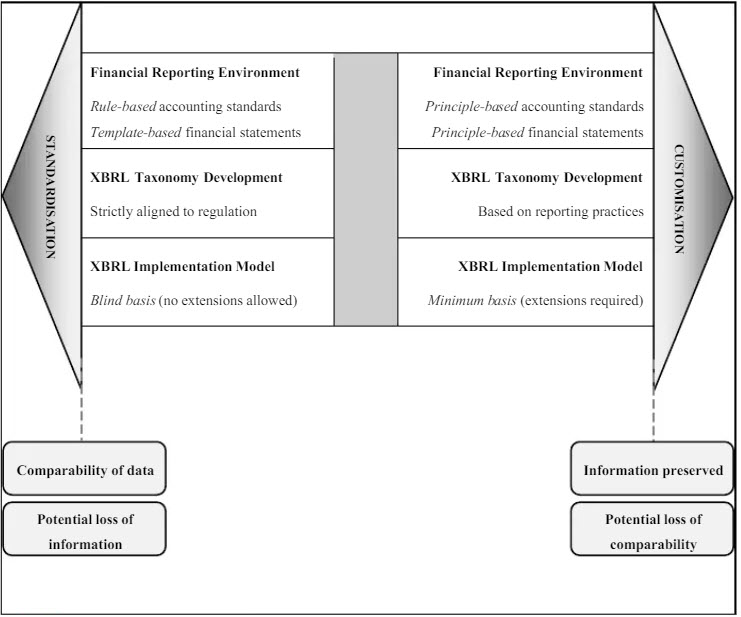

I ran across a very good academic paper that was published in 2013. The title of the paper is Critical Reflection on XBRL: A “Customisable Standard” for Financial Reporting? In the paper they compare two approaches for creating XBRL taxonomies and reports and they provide the following graphic from page 126 of that paper. They call the approaches "Standardization" which means a forms-based implementation with no extensions allowed and "Customization" which means extensions are allowed. Then at the bottom they provide information about the resulting ability to consume reported information and the idiosyncratic details provided within the report.

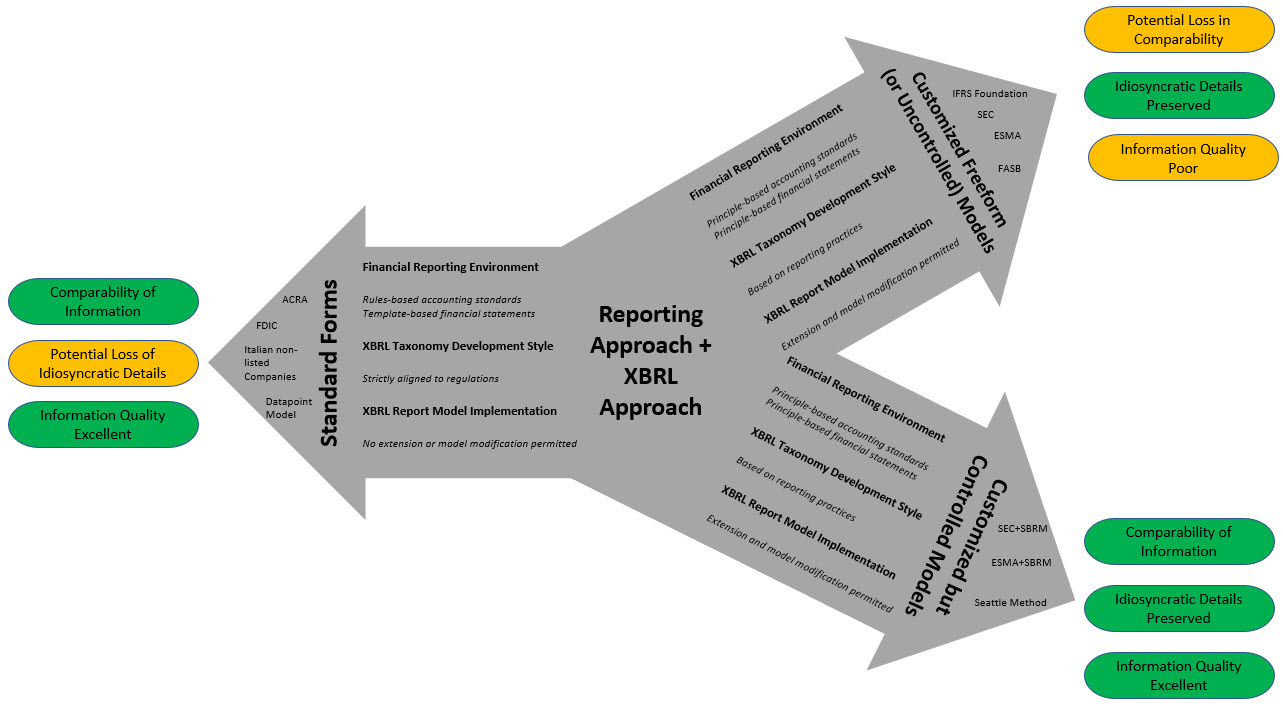

That is a good graphic, but the graphic is incomplete. And so I created my own graphic inspired by the graphic provided in the above academic paper. What I did was break the "Customization" down into two distinct parts:

- "Freeform Model" is where an implementer allows extensions to taxonomy report elements and to the creation of a report model but DOES NOT PROVIDE MECHANISMS TO CONTROL the extensions or reconfigurations to keep them within permitted boundaries.

- "Controlled Model" is also where an implementer allows extensions to taxonomy report elements and to the creation of a report model and ALSO PROVIDES A MECHANISM TO CONTROL the extensions and reconfigurations of the report model in order to keep them within permitted and expected boundaries.

This graphic is my enhanced version of what the paper above provides. I have also color coded the consequences of the implementation decision:

Granted, the Seattle Method did not exist in 2013 when that academic paper was written. But now it does exist.

Today, most existing XBRL implementations use the Standard Forms approach. Those that do allow for customization do not control the report model customization well, if at all really; as a result they have quality issues.

#################

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

1 Reference

1 Reference

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to FriendReferences (1)

-

Response: famous celebrities

Response: famous celebrities

Reader Comments