Conceptual Legos and the Universe of Discourse

A significant problem that professional accountants have with XBRL is that they don't understand the moving pieces of the conceptual model, the "Conceptual Legos" that make up the pieces of an XBRL-based digital financial report.

If you don't understand the higher-level conceptual model then the model is defined in solely syntactic terms and as such do not have any meaning until they are given some interpretation. That interpretation is the semantics of the model.

How hard is it for you to interpret the information in the graphic below? (Click the image, and a larger view will be provided.) It is probably pretty easy for either accountants or even non-accountants to interpret that information. That graphic is driven by 100% pure XBRL. Now, the application processing the information is driven by some additional information about business reports, the multidimensional model. That helps software render the information. The multidimensional model provides information that gets things into the right rows, columns, and cells.

(Click image for larger view)

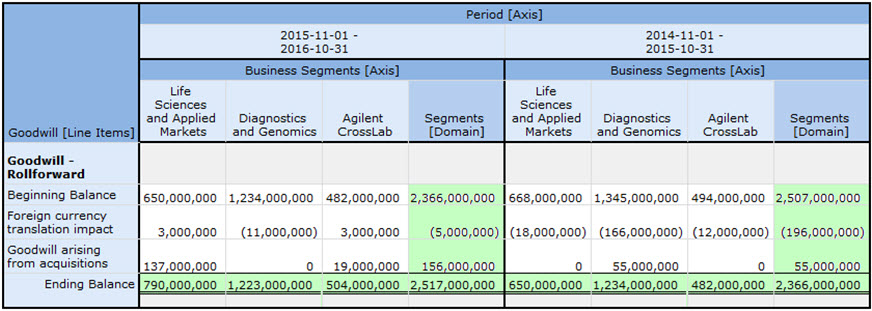

(Click image for larger view)

Now, the report fragment above happens to be a disclosure of the goodwill roll forward, the changes in goodwill from each balance sheet beginning balance to each ending balance.

Not surprisingly, reports contain lots of report fragments. Those report fragments represent lots of different disclosures. Many of those disclosures are roll forwards. Others are roll ups. I gave the terms "roll forward" and "roll up" and similar patterns in the organization of reported disclosures a name; I call them concept arrangement patterns.

If you scan this document that contains descriptions of about 65 or so financial disclosures, you will see lots of different roll forwards, roll ups, and other concept arrangement patterns. If you look at each of those disclosures and the one shown above, you see cells colored GREEN which represents a mathematical computation. Every roll forward actually mathematically rolls forward. That is shown be the GREEN cells in the last row of that disclosure. This particular roll forward also cross-casts shown by the other GREEN cells. I gave this cross-cast a name also, I call it a member arrangement pattern.

I documented all these terms that I refer to in this Introduction to the Conceptual Model of a Digital Financial Report.

A Universe of Discourse is the set of all things under consideration during a discussion, examination, or study.

A universe of discourse is also the set of all objects or entities that is defined by a conceptual model. XBRL-based digital financial reporting is NOT "conceptually promiscuous"; you simply cannot just add new pieces to the conceptual model. Now, don't get confused here. The conceptual model is the shape of the information you put into the model. Remember, the same XBRL technical syntax can be used to define both US GAAP and IFRS financial reporting schemes. US GAAP and/or IFRS concepts (and other stuff) is what goes INTO the conceptual model. US GAAP and IFRS share the same business report and financial report conceptual model.

Now, you don't want all this to be a mess and you want a consistent interpretation of the conceptual model, so you define rules. Why? Because rules prevent anarchy. See XBRL-based digital financial reporting principle #3: "Anarchy is defined as 'a situation of confusion and wild behavior in which the people in a country, group, organization, etc., are not controlled by rules or laws.' Rules prevent anarchy."

Rules assert knowledge. For example, "Assets = Liabilities and Equity" (i.e. the accounting equation) is both a rule and knowledge. Constraints are restrictions on existing knowledge. Constraints can be used to detect incomplete information. Constraints can be used to check knowledge for inconsistencies and contradictions. Rules all follow the same rules of logic.

The rules of logic are a common denominator for a universe of discourse, or sometimes referred to as a domain. Business professionals interact with the conceptual model using the semantic level of these "Conceptual Legos" logical pieces software applications expose that are understandable by the user of the software system. Business professionals don't interact with the technical syntax.

The system is not a "black box", rather the system is transparent do that the business professional using the system and understands what the system is doing.

Digital financial reporting requires that every business user of the system share the same universe of discourse, the same fundamental conceptual model, and the same logical rules. The goal is that every interpretation of the conceptual model is consistent with the intended interpretation of the conceptual model. The conceptual model is formal, the conceptual model is definable, and the conceptual model has a finite set of shapes.

When a software developer puts all these pieces together correctly, what do you get? You get easy to use software and zero defect digital financial reports. Software is easy to use because it is simple. Not simplistic, simple. Simple means you work hard to keep complexity to a minimum. See the Law of Conservation of Complexity. Reports don't have defects because humans augmented by machines that leverage rules watch over the creation of the report.

Here is an example of such software. That is just a robust proof of concept to test all these ideas. More software is on the way!

Pretty good stuff, huh! Well, I cannot take any credit for it. These ideas come from Blockly which came from Scratch. I am simply applying those ideas to financial reports.

Charlie

Charlie

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments