BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from January 1, 2021 - January 31, 2021

Tempered Radicals can Effect Change Without Causing Trouble

In her article, Radical Change, the Quiet Way, Debra Meyerson explains that change is hard; change is messy. If you speak out too loudly you can create resentment towards you. But if you “play by the existing rules” (i.e. remain silent) resentment builds within you. The trick is to rock the boat without being thrown out or falling out of the boat.

Tempered radicals can strike the right balance, making change without causing trouble.

Me, I tend to lack a lot of the "tempered-ness". I tend to be too radical for most people to handle. You don't have to be that way in order to effect change. Change takes time.

For more information see Debra Meyerson's book, Rocking the Boat: How Tempered Radicals Effect Change without Making Trouble.

Representation Theory

In the article The 'Useless' Perspective That Transformed Mathematics Kevin Hartnett explains representation theory thus:

Representation theory is a way of taking complicated objects and “representing” them with simpler objects. The complicated objects are often collections of mathematical objects — like numbers or symmetries — that stand in a particular structured relationship with each other. These collections are called groups. The simpler objects are arrays of numbers called matrices, the core element of linear algebra. While groups are abstract and often difficult to get a handle on, matrices and linear algebra are elementary.

A financial report is a complicated object that can be represented using simpler objects. The Logical Theory Describing Financial Report describes those objects and the relations between the objects.

You can represent all of those objects using XBRL, see this PROOF BASELINE. The PROOF BASELINE can be reconciled to high quality financial reporting schemes such as US GAAP, IFRS, UK GAAP, Australian IFRS, etc.

All this yields a more modern approach to accounting, reporting, auditing, and analysis.

Folks, fundamentally all this is math.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

2 References

|

2 References

|  Email

|

Email

|  Print

Print

Making the Move to Modern Accounting

There are many different ways to describe what is going on in accounting today. One of the better descriptions I have run across is used by Blackline. They call it "making the move to modern accounting" and Blackline provides what they call the modern accounting playbook to help organizations make this move. Here Blackline and SAP explain the benefits. Here Blackline makes the case for continuous accounting.

Others have different descriptions for what is going on. Deloitte calls it "the finance factory". Others refer to what is going on as continuous accounting. Others a finance transformation.

Whatever the term used to describe it, what is going on relates to improving accounting, reporting, auditing, and analysis processes.

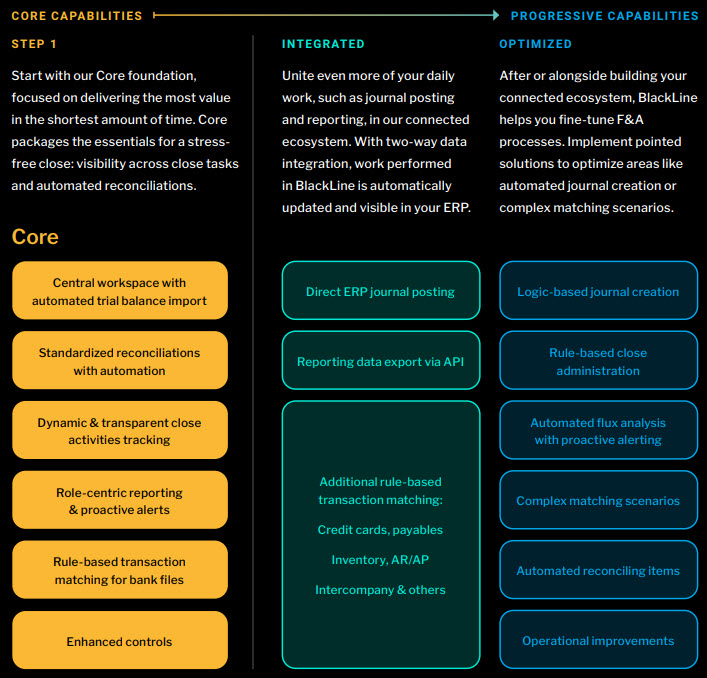

No one really explains HOW to implement "modern accounting" in detail. In their Modern Accounting Playbook on page 3 Blackline does provide the following high-level description:

My focus is the complete process. And my focus is not to make a few incremental changes but rather to rethink accounting, reporting, auditing and analysis. I have successfully automated all the way from initial journal entry to generating the external financial reports and many steps in between using a standards-based best practices based method I have created.

A fundamental mistake that far too many accountants make is not entering information into the accounting system at all or late in the accounting process. As The Knowledge Graph Cookbook: Recipes that Work points out, "The basic rule is that context tagging and classification should take place as soon as possible after the content is created."

My second best prototype of the record-to-report process helps me understand and identify several specific things that are fundamentally missing from the typical current accounting process or cause implementing modern accounting more challenging than it really needs to be. For example:

- Poorly implemented chart of accounts.

- What Workday calls "work tags" are missing from accounting systems.

- Information that explains how to aggregate chart of accounts/trial balance information into the financial report line items, subtotals, and totals is not in the accounting system (typically in a report writer).

- Policies are not in the accounting system.

- Information related to quantitative and qualitative disclosures is not in the accounting system.

- Disclosure checklists are human readable (i.e. not machine readable) and therefore not usable in automated processes.

- Other process control information is not available to processes in machine-readable form.

There are a few other odds and ends that are missing but the above should give you a good idea of what I am talking about.

Further, Blackline's process appears to be proprietary (i.e. does not use global standards such as XBRL). That is excellent for Blackline, but it is not good for consumers.

Finally, I don't hear Blackline or others talk about things like Lean Six Sigma process control techniques and philosophies that help control process quality.

So turning this around; imagine something like Blackline connected to Engine B's notion of an always on audit which is also connected to say Workivia's XBRL-based financial reporting tool which is connected to Mindbridge's AI Assisted Audit tool. Information is exchanged between one tool and another virtually friction free because the XBRL standard technical syntax is used. My record-to-report process prototype shows every detail of how to build this.

In my view, this is what accountants should be asking for. The better the questions accountants ask software vendors the better software those vendors will provide.

If you are a tempered radical that is trying to change your organization ping me if you want a link to my best prototype of record to report.

########################

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print