BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from July 28, 2019 - August 3, 2019

Understanding Logic Basics

Different domains such as philosophy, computer science, and knowledge engineering use different terminology to describe and discuss logic which can be quite confusing and make these things harder to understand. Below are the common fundamental terms that I came up with based on what others are using in an attempt to come up with a best practices summary of this terminology.

Logic is a set of principles that forms a framework for correct reasoning. Logic is a process of deducing information correctly. Logic is about the correct methods that can be used to prove a statement is true or false. Logic tells us exactly what is meant. Logic allows systems to be proven. Using logic information can be created that is understandable both to humans and to machines.

- A logical system or formal system is a set of terms, relations, assertions, and a world view that is proven to be consistent, valid, complete, sound, and fully expressed. An ontology-like thing can define a logical system. A financial report is a type of logical system.

- A model, or conceptual model or conceptualization, describes a possible world. There exists some set of all possible models that can be used to describe real worlds that could exist.

- A logical statement is a sentence that carries information that is either true or false. Terms, relations and assertions are all forms of statements which provide information about a logical system. A statement, a statement of fact, and a fact mean the same thing. Questions, commands, and opinions are not logical statements. All statements have a truth value with respect to some model.

- Axioms, theorems, and restrictions are all types of assertions.

- An axiom is a type of statement that describes self-evident logical statements related to a logical system that no one would argue with.

- A theorem is a type of statement that is a logical deduction which can be proven by constructing a chain of reasoning by applying axioms or other theorems in the form of IF…THEN statements.

- A restriction is a constraint or limit usually mandated by some sort of authority.

- A rule is a synonym for assertion with respect to some model of the real world that could possibly exist (i.e. you cannot create rules that are true in worlds that can never exist).

- A conditional statement is a type of statement that has an IF…THEN type format. Look at a statement as being a piece of information that is either correct or incorrect.

- Logical entailment, or logical consequent, is when a logical statement follows from another statement or set of statements. Synonyms for logical entailment include logical inference or logical deduction. Accountants sometimes use the term impute. The rules of inference provide a system in which we can produce new information (statements) from known information (statements).

- The connectors AND, OR, and NOT are used to combined statements to create compound statements.

Logic gates are building blocks of a digital system. Terms, relations, and assertions of some logical system can be determined to be logically consistent or inconsistent with some logical system.

Professional accountants have an innate understanding of logic. Having a bit more formal understanding will help professional accountants thrive in the digital age and what is being called the fourth industrial revolution.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Barriers to Financial Reporting Automation are Really all in the Mind

This article by Michael Berrington, Director at IFRS SYSTEM and Financial Reporting Specialists, Barriers to automating financial reporting, hits the nail squarely on the head:

“In most cases the barriers to financial reporting automation are really all in the mind.”

You can read the article yourself to get the details.

Here is everything you need to know to have an intelligent conversation about digital financial reporting. Recognize that expert systems for creating financial reports will be created. Artificial intelligence will be assisting auditors (AI assisted audits). Accounting bots will be a reality. The Finance Factory will be created. The Fourth Industrial Revolution is a real thing.

And so HOW will all this come to be? Brick-by-brick, that is how it will be created. Lots of tasks could be candidates for automation:

(Click image for larger view)

Brick-by-brick, much like building a house, business domain experts and software engineers can create tools that automate certain types of tasks in some process. Humans encode information, represent knowledge, and share meaning using machine-readable terms, relations, assertions, patterns, languages, and logic (i.e. ontology-like things). That will be the way an increasing number of work tasks will be performed to complete accounting, reporting, auditing, and analysis tasks in a digital environment. Lean six sigma techniques and philosophies will help keep process quality high. The result will be more efficient and more effective processes.

If you want to make sure you get your foundation right and want to understand the moving pieces of the puzzle, I would suggest that you have a look at Artificial Intelligence and Knowledge Engineering Basics in a Nutshell.

This is another good article.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

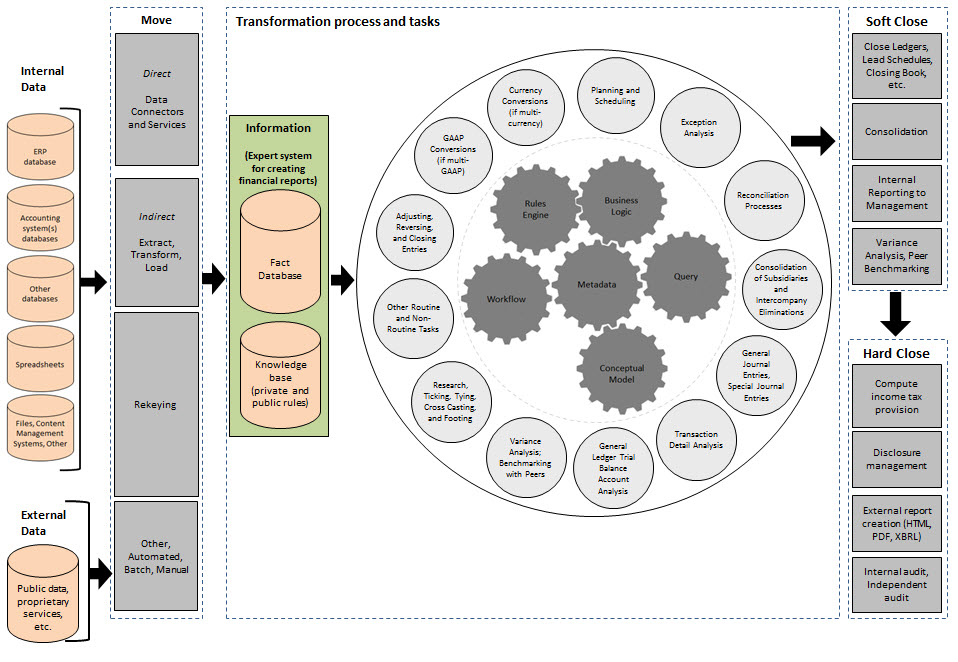

Central Role Played by Ontology-like Things and Other Metadata

If you understand how computers work; then you will recognize that ontology-like things and other such metadata will play a central role in accounting, reporting, auditing, and analysis in a digital environment. Properly created ontology-like things and other metadata will supercharge accounting, reporting, auditing, and analysis. Consider this diagram:

(Click image for larger view)

If there is any question in your mind about this, I would encourage you to read the following documents:

- Demystifying the Role of Ontologies in XBRL-based Digital Financial Reporting: Helps you understand that XBRL taxonomies and other such ontology-like things will be enhanced.

- Leveraging Functional Components for XBRL-based Digital Financial Reporting: Helps you understand how software applications utilize ontology-like things and other metadata.

- Deloitte's vision of "The Finance Factory": Deloitte has an excellent vision; but how exactly are they going to actually turn that vision into reality? Ontology-like things and other metadata.

- Data Curation: Weaving Raw Data Into Business Gold (Part 1): Explains how curated metadata and other such ontology-like things turn raw material such as crude oil into high-octane racing fuel.

Once you see the "magic" working, it will be easy to understand all of this. For now, you can fiddle around with my prototype ontology-like thing and other metadata. Also, here is some additional brainstorming related to these ideas.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print