BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from October 6, 2019 - October 12, 2019

PWC to Invest $3 Billion in Upgrading Skills

Accounting Today, PwC invests $3B in "New World, New Skills" Program:

Big Four firm PwC is launching a new program, entitled “New World, New Skills,” that will focus on the growing mismatch between people’s existing skills and the new skills demanded by the digital economy. The firm will invest $3 billion over the next four years in upskilling — primarily in training PwC staff, but also in developing and sharing technologies to support clients and communities.

The digital revolution requires a skills revolution. The skills revolution is about helping people build their digital awareness, understanding and skills to fully participate in the digital world — and it needs to start now.

Do you want to upgrade your skills? It is time for professional accountants to understand digital financial reporting. Start here, Artificial Intelligence and Knowledge Engineering in a Nutshell. Also see Digital Maturity.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Proving Accounting, Structural, Mathematical, and Other Logic of XBRL-based Financial Reports

There are nine specific identifiable situations which occur in XBRL-based financial reports which cause accounting logic, mathematical logic, structural logic, or other types of logical errors. The document Proving Accounting, Structural, Mathematical, and Other Logic of XBRL-based Financial Reports explains each of these situations and explains how to eliminate the situation.

Here is a summary of the nine situations:

- Using an existing base taxonomy concept intended to represent one class of concept inadvertently to represent some other class of concept.

- Lack of clarity of the meaning of extension concepts.

- Unreported high-level subtotals.

- Variability allowed for reporting high-level accounting relationships.

- High-level financial report line item inconsistencies and contradictions.

- Presentation relations model structure relations illogical.

- Verification that each report fragment is created correctly.

- Mathematical relations are not explained using machine-readable rules and then verified against that machine-readable explanation.

- Verification that each report fragment that is required to be disclosure exists within the financial report.

All of these nine situations are observable in the thousands and thousands of XBRL-based financial reports that have been submitted to the U.S. Securities and Exchange Commission. XBRL Cloud provides what the call the Edgar Dashboard which shows summaries for many of these situations.

It is highly likely that ESMA is going to repeat many of these same sorts of errors. While the ESMA has done some additional things such as added anchoring, they have not consciously engineered a system which eliminates each of these situations. Therefore, they will experience errors and quality issues.

Consider something. Let us turn all of this around. Let us wonder what might happen if someone implemented XBRL-based financial reporting, they used an architecture similar to the SEC, they adjusted the SEC architecture to add the features articulated in the PDF that explains how to eliminate all of those situations/issues. Perhaps they add a few additional best practices that have been proven over the past 10 years of submitting XBRL-based reports to the SEC.

What would you get? Well, you would get a much better system that has higher quality XBRL-based reports. This video walks you through how software can leverage rules and use automated machine-based processes to (a) explain what "correct" looks like, verify that a report is consistent with that explanation, and (c) be used by those wishing to extract information from such report effectively and reliably.

This video playlist shows a working proof of concept that demonstates XBRL-based financial reporting does not need to be "technical" and "complex". It actually can be simple and elegant.

#########################

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

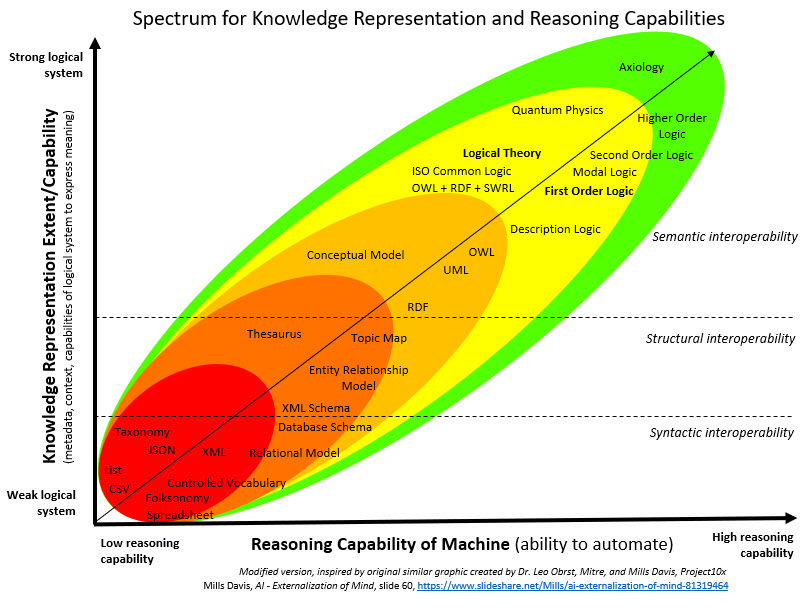

Revisiting the Knowledge Representation Spectrum

I discussed the knowledge spectrum and reasoning capacity in another blog post several years ago. It is time to have another look.

This graphic from Mills Davis' presentation AI - Externalization of the Mind, slide 66, depicts the relationship between knowledge representationn and reasoning capacity:

(Click image for larger view)

So, there is a little more to achieving the capability of a machine to reason. Yes, you do need an approach to representing knowledge such that a machine, such as a computer, can leverage that knowledge to perform useful work.

- You need a global standard technical format to represent the knowledge. (i.e. XBRL)

- You need standard models that you use to represent the knowledge. (i.e. business report model)

- You need to put knowledge into that format using that model. (i.e. FRF for SMEs; US GAAP)

- You need standard software that can read the knowledge that exists in that technical format and perform the required work. (i.e. Pesseract; XBRL Query; XBRL Cloud)

- You need to prove interoperability between standard software. (i.e. comparison of Pesseract, XBRL Query, XBRL Cloud; conformance suite)

Once you have all five things above, then you simply have a commodity; you have all the pieces of the "mouse trap" (law of irreducible complexity). One should be able to demonstrate why the system works. Here is my demonstration: machine-readable | human readable.

A kluge, a term from the engineering and computer science world, refers to something that is convoluted and messy but gets the job done. Anyone can create something that is complex. But it is hard work to create something that is simple.

Welcome to the Fourth Industrial Revolution! Do you and your organization have the digital maturity necessary to compete? Are you a novice or an expert? What will you create? What role will you play? Do you need to improve your digital maturity?

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

33 References

| Email

| Print

33 References

| Email

| Print