BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Gamified Incentive Model

It all started with John von Neumann and Oskar Morgenstern's Theory of Games and Economic Theory. Now it is commonly referred to game theory or gamification. Gamification is defined by Wikipedia as follows: (emphasis is mine)

Gamification is the strategic attempt to enhance systems, services, organisations and activities in order to create similar experiences to those experienced when playing games in order to motivate and engage users.

Gamified incentive models seem to be a way to understand the economics of digital for CPAs.

A game is defined as: Any interaction between multiple parties in which each party's payoff is affected by the decisions of others.

Here is more information:

- Game Theory Explained in One Minute

- Gamification Done Right - The Do's and Don'ts

- 10 Examples of Gamification for Employee Engagement

More to come.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Roadmap to XBRL-based Digital Financial Reporting Mastery

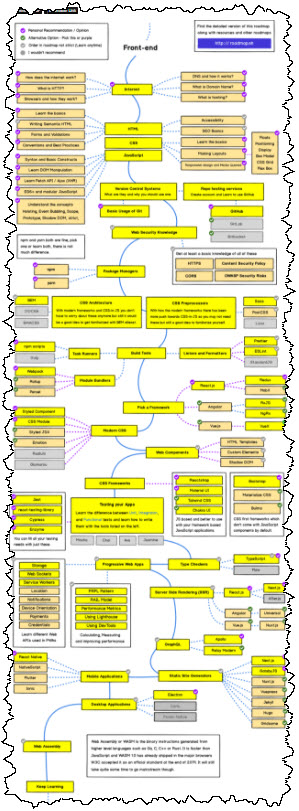

This is really interesting. I got an email that had a link to The Self-taught UI/UX Designer Roadmap in 2021. That web page also mentions the Roadmap to Becoming a Web Developer in 2021. What I really like is the organization, in particular these graphics:

What I need to do is create a Roadmap to XBRL-based Digital Financial Reporting Mastery and perhaps even offer a certificate when the roadmap is complete. This would be "a deep dive guide on teaching yourself XBRL-based digital financial reporting from zero knowledge to a full-time role."

Here is the content for the roadmap, Mastering XBRL-based Digital Financial Reporting. I just have to organize it.

Stay tuned!

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Financial Report Levels

I initially provided this summary of financial report levels in another blog post: (An example of each level is provided and here are more details about the levels; this VIDEO explains the levels; this PDF presentation explains the levels)

- Level 0: Not machine readable.

- Level 1: Machine readable, nonstandard, structured for presentation.

- Level 2: Machine readable, nonstandard, structured for meaning, no taxonomy (a.k.a. dictionary), no rules, no report model.

- Level 3: Machine readable, global standard syntax, structured for meaning, with taxonomy (a.k.a. dictionary), incomplete rules, incomplete high-level report model. (Level3a shows XBRL calculations also removed)

- Level 4: Machine readable, global standard syntax, structured for meaning, with taxonomy (a.k.a. dictionary), complete set of rules provided, incomplete high-level report model.

- Level 5: Machine readable, global standard syntax, structured for meaning, with taxonomy (a.k.a. dictionary), complete set of rules provided, complete global standard high-level report model, yields PROVEN properly functioning system and UNDERSTANDABLE report information.

- Level 6: All of Level 5 PLUS blockchain-anchored XBRL to increase trust.

- Level 7: All of Level 6 PLUS blockchain-anchored transactions and events.

I have revised the financial report levels slightly to make them more understandable. This is the revised set of financial report levels:

- Level 0: Not machine readable.

- Level 0a:Nonstandard syntax, nonstandard meaning.

- Level 1: Standard syntax, structured for presentation.

- Level 2: Standard syntax, structured for meaning.

- Level 3: Standard syntax + Dictionary of Terms.

- Level 4: Standard syntax + Dictionary of Terms + Associations between Terms + Rules

- Level 5: Standard syntax + Dictionary of Terms + Associations between Terms + Rules + Model. (Complete, consistent, precise)

- Level 6: All of Level 5 PLUS blockchain-anchored XBRL to increase trust.

- Level 7: All of Level 6 PLUS blockchain-anchored transactions and events.

Level 5 is the minimum that will work for XBRL-based digital financial reporting when report creators are permitted to modify the report model. To understand all of this I recommend the following three documents:

- Essence of Accounting

- Understanding Method (Abridged)

- Essentials of XBRL-based Digital Financial Reporting

Those three documents will help you understand the dynamics of financial information.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

New Rules for the New Economy

In his book, New Rules for the New Economy, its author Kevin Kelly helps you wrap your head around how the future will likely work. Many things in the new economy (i.e. economics of digital) will not work like they did in the old economy. Believing that things will work the same is a fundamental mistake. This is Kelly's description of the book:

The thesis of New Rules for the New Economy is that we are now living in an economy based on ideas and communication rather than energy and atoms. Further, this "new" economy has distinct laws or rules so it behaves differently than the previous industrial economy. To do well in the new regime, we need to grasp the new dynamics of information. I reduce the emerging principles to 10 guidelines, and suggest a few strategies for businesses based on each principle.

(You can get the book on Amazon here. You can download the free PDF here.)

Here is a summary of the rules:

- Embrace the Swarm.

- Increasing Returns.

- Plentitude, Not Scarcity.

- Follow the Free.

- Feed the Web First.

- Let Go at the Top.

- From Places to Spaces.

- No Harmony, All Flux.

- Relationship Tech.

- Opportunities Before Efficiencies.

Accounting, reporting, auditing, and analysis are evolving. Be sure to read my blog post The Economics of Digital for CPAs. Understand the role of XBRL in this new economy. Understand how to use XBRL-based financial reports effectively. The old industrial economy and the new information economy will not work the same. We all need to grasp the dynamics of information.

Don't think data, think information. Big, big changes are on the way.

#############################

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Calls to Improve Financial Disclosure

Accountants and others have been talking about improving financial disclosure practices my entire career as an accountant. But few things really seem to change. Here are some of the proposals to improve financial disclosure that I am aware of: (in no particular order)

- A Comprehensive Business Reporting Model (CBRM) (CFA Institute 2007)

- Improving business reporting-- a customer focus (AICPA 1994)

- Principles of Disclosure (IFRS Foundation 2017)

- Better Communication in Financial Reporting (IFRS Foundation 2017)

- A Matter of Principles, Future of Corporate Reporting (FRC 2020)

- FASB sees flexibility, relevance as cures to disclosure overload (FASB 2012)

- Will Simpler Also be Better (Journal of Accountancy 2012)

There are plenty of other reports.

If you have not noticed, I am big on frameworks. The CFA institute paper makes the following statement on page 2:

A conceptual framework for business reporting must provide a sound foundation for every accounting standard, proposal, and interpretation. We believe, however, that a properly conceived and executed framework should serve also as a benchmark by which the quality of a proposed standard may be judged. The framework should guide standard setters in their deliberations on the development of new reporting pronouncements, but it should also provide a template for assessing whether the standard-setting work is finished or remains deficient in one or more material aspects.

I agree that a conceptual framework and principles are important. Both the IFRS Foundation and FASB have conceptual frameworks for financial reporting. But those conceptual frameworks need to be refined and tuned for digital.

The CFA Institute paper makes very specific observations. For example from page 5:

The extreme degree and inconsistent pattern of aggregation and netting of items in the statements—along with the obscured, even opaque, articulation of the financial statements—make such analysis ineffective or impossible.

Do reporting entities play games with their financial disclosures? What do you think?

The CFA Instutute paper goes on to list and explain the following 12 concepts (or principles):

- The primary financial statements must provide the information needed by equity investors, creditors, and other suppliers of risk capital.

- In financial reporting, standard-setting, as well as statement preparation, the entity must be viewed from the perspective of an investor in the common equity issued by the company.

- Fair value information is the most relevant information for financial decision making.

- Recognition and disclosure must be determined by the relevance of the information to investment decision making and not based upon measurement reliability alone.

- All transactions and events must be recognized as they occur in the financial statements.

- Investors’ information requirements must determine the materiality threshold.

- Financial reporting must be neutral.

- All changes in net assets, including changes in fair values, must be recorded in a single financial statement, the Statement of Changes in Net Assets Available to Common Shareowners.

- The cash flow statement provides information essential to the analysis of a company and should be prepared using the direct method only.

- Changes affecting each of the financial statements should be reported and explained on a disaggregated basis.

- Individual line items should be reported based upon the nature of the items rather than by the function for which they are used.

- Disclosures must provide the additional information investors require to understand the items recognized in the financial statements, their measurement properties, and their risk exposures.

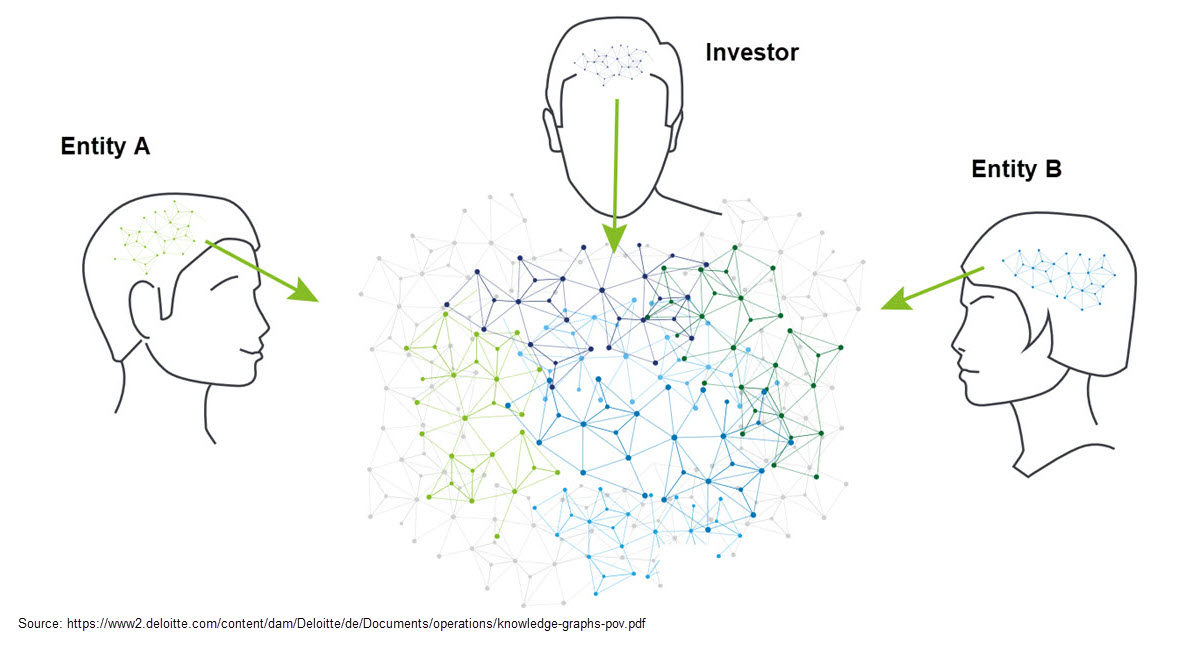

In my view, those concepts (or principles) are a little bit in favor of the needs if investors. Not a lot and perhaps not without a little bit of justification because investors are one of the primary use cases for financial reports. In my blog post Understanding the Role of XBRL I provide this excellent graph created by Deloitte: (click the image for a larger view, or click here to go to Deloitte's paper)

What I can say is the following: Prudence dictates that using financial information from a general purpose financial report should not be a guessing game.

More to come so stay tuned.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print