Intelligent XBRL-based Financial Reporting Maturity Levels

I have made the comparison of digital blueprints, CAD, and digital financial reports before. Ask yourself a question: How useful would a digital CAD blueprint be if that blueprint had errors? If a construction contractor put together a building with a blueprint that had errors, or if someone tried to assemble an iPhone with pieces designed with blueprints that had errors, or if information was supplied to a numerically controlled machine that creates engine parts; how would that work out?

Clearly errors in XBRL-based digital financial reports would cause similar problems when investors, analysts, regulators, and others used information from the report.

So, how exactly does a digital CAD drawing achieve high quality? Why can CAD work as a global standard for the design, engineering, and creation supply chain; but XBRL-based digital financial reports have to be so error prone? What causes the difference?

How can it be that draftsmen, architects, engineers, designers, and others can successfully create near error-free digital blueprints but accounting professionals cannot create near error-free digital financial reports? Why is that?

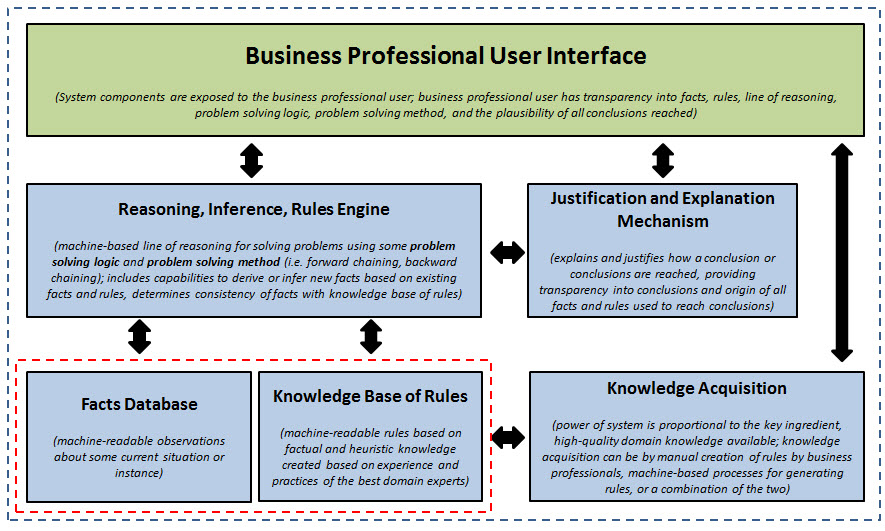

Like many things, intelligent XBRL-based digital financial reporting will evolve and go through different maturity levels. Just like CAD, an intelligent XBRL-based digital financial report is a knowlege based system. Such a system has specific parts. This diagram outlines those parts and shows the relations between each part of a knowledge based system:

(Click image for larger view)

(Click image for larger view)

Here is an overview of each part part of a knowledge based system such as an intelligent XBRL-based digital financial report:

- Database of facts: A database of facts is a set of observations about some current situation or instance. The database of facts is "flexible" in that they apply to the current situation. The database of facts is machine-readable. An XBRL instance is a database of facts.

- Knowledge base (rules): A knowledge base is a set of universally applicable rules created based on experience and knowledge of the practices of the best domain experts generally articulated in the form of IF…THEN statements or a form that can be converted to IF...THEN form. A knowledge base is "fixed" in that its rules are universally relevant to all situations covered by the knowledge base. Not all rules are relevant to every situation. But where a rule is applicable it is universally applicable. All knowledge base information is machine-readable. An XBRL taxonomy is a knowledge base. Business rules are declarative in order to maximize use of the rules and make it easy to maintain business rules. Knowledge that makes up the knowledge base is acquired using manual or automated knowledge acquisition processes.

- Reasoning engine: A reasoning engine provides a machine-based line of reasoning for solving problems. The reasoning engine processes facts in the fact database, rules in the knowledge base. A reasoning engine is also an inference engine and takes existing information in the knowledge base and the database of facts and uses that information to reach conclusions or take actions. The inference engine derives new facts from existing facts using the rules of logic. The reasoning engine is a machine that processes the information. An XBRL Formula processor, if built correctly, can be a reasoning engine and can perform logical inference.

- Justification and explanation mechanism: When an answer to a problem is questionable, we tend to want to know the rationale behind the answer. If the rationale seems plausible, we tend to believe the answer. The justification and explanation mechanism explains and justifies how a conclusion or conclusions are reached. It walks you through which facts and which rules were used to reach a conclusion. The explanation mechanism is the results of processing the information using the rules processor/inference engine and justifies why the conclusion was reached. The explanation mechanism provides both provenance and transparency to the user of the expert system.

These four pieces are exposed to the users of the knowledge based system within software applications that is used by a business professional.

Software applications must provide all of these pieces. The law of irreducible complexitystates basically that "A single system which is composed of several interacting parts that contribute to the basic function, and where the removal of any one of the parts causes the system to effectively cease functioning." That means that each of the parts in the diagram need to exist for the system of an XBRL-based digital financial report to work correctly.

Further, the system must be usable by business professionals. The law of conservation of complexity essentially states, "Every software application has an inherent amount of irreducible complexity. That complexity cannot be removed from the software application. However, complexity can be moved. The question is: Who will have to deal with the complexity? Will it be the application user, the application developer, or the platform developer which the application leverages?"

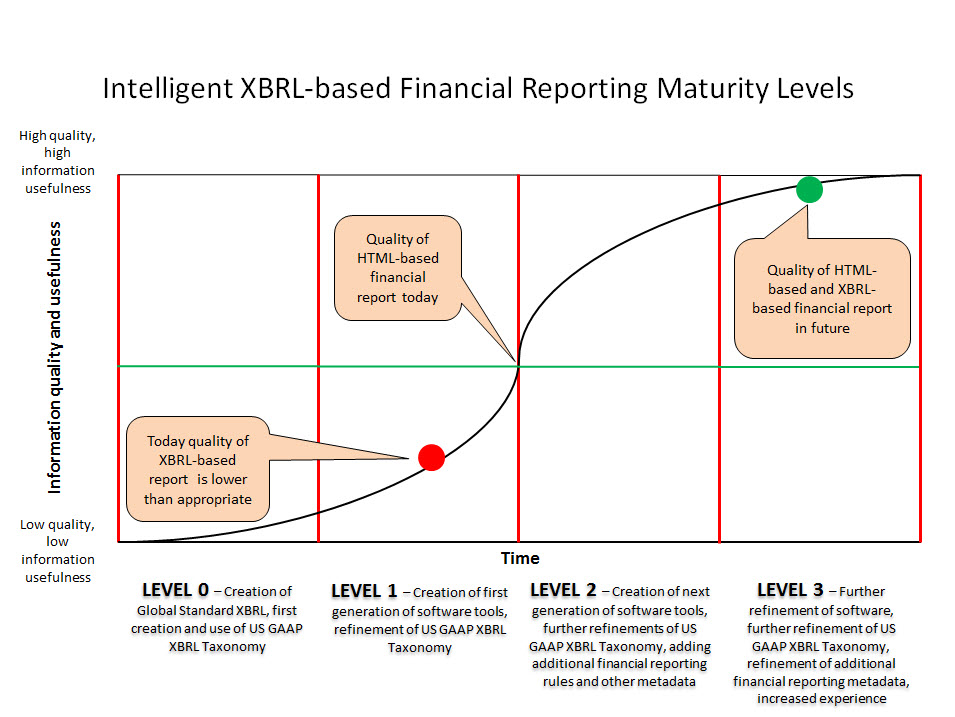

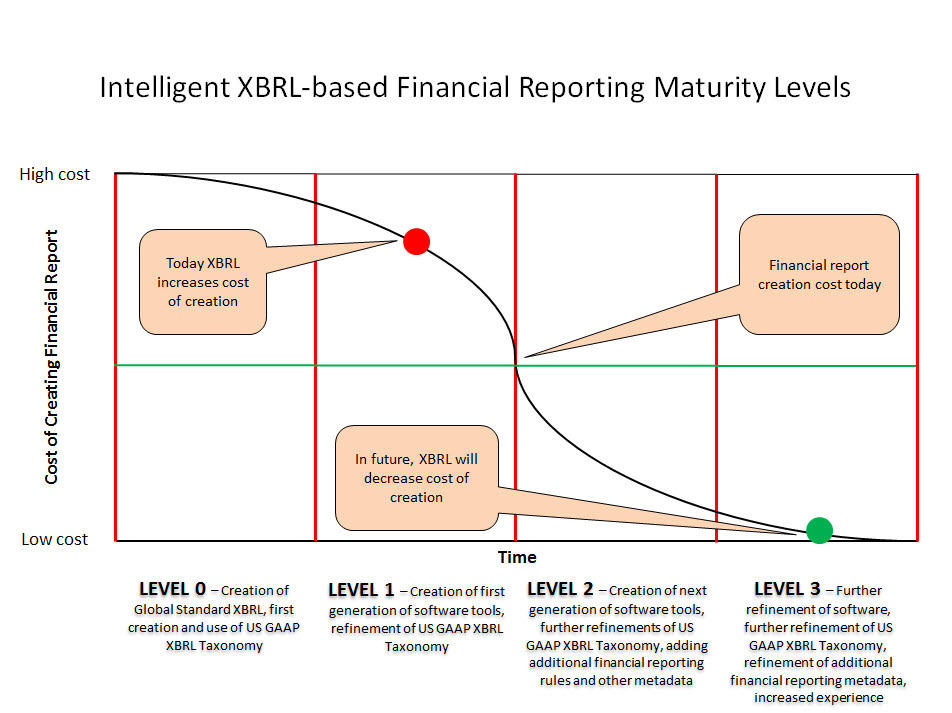

Today's software applications do not provide all of these parts completely or in a form that is usable by business professionals creating intelligent XBRL-based digital financial reports. But when software does provide all of these pieces, two pivots will occur. The two graphics below show that the benefits of XBRL-based digital financial reporting will flip the dynamics of the financial reporting process. A disruptive innovation will occur. The barbaric processes used to create financial reports today will evolve and be replaced by new, better, faster, and cheaper processes.

These three things need to occur:

- More business domain knowledge in machine-readable form put into the knowledge base (rules).

- Better software applications which more precisely provide all the components of a knowledge based system in a form useable by business professionals.

- Business professionals need to learn a handful of things about knowledge engineering so that they don't need to rely of knowledge engineers or information technology professionals to create financial reports.

Quality pivot:

(Click image for larger view)

(Click image for larger view)

Cost pivot:

(Click image for larger view)

(Click image for larger view)

Blueprints made the flip to digital in the 1980s and 1990s. Do you believe these changes are possible for financial reporting?

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments