Understanding the Importance of Triple-Entry Accounting

Between 5,000 and 10,000 years ago farmers in Mesopotamia, where agriculture was born, used physical object to count crops and animals . The distinction between types of crops or animals was made by using different types and shapes of objects.

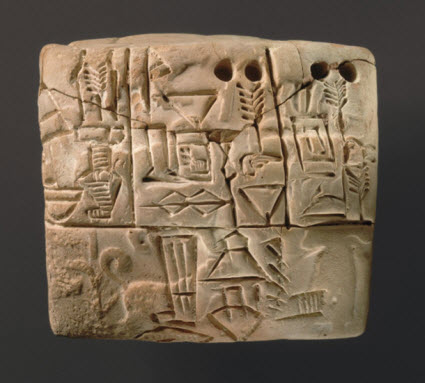

Then, in about 3200 BC, around 5,000 years ago, the first spreadsheet was invented. These farmers began documenting information using clay tablets in the earliest form of human writing ever discovered called Cuneiform. They partitioned their clay tablet into rows, columns, and cells. These farmers used single-entry accounting.

Source: Metropolitan Museum

Source: Metropolitan Museum

In 1211 AD a bank in Florence, Italy was the first documented use of double-entry accounting. Between 1299 AD and 1300 AD double-entry accounting came of age. In 1494 AD during the Renaissance, Venetian mathematician and Franciscan friar Luca Pacioli published a book, Summa de arithmetica, geometria. Proportioni et proportionalita (Sum of Arithmetic, Geometry, Proportion and Proportionality). That book documented the double-entry approach bookkeeping and recommended that others use this approach. The double-entry approach allowed for better error detection and the ability to differentiate unintended errors from fraud. Accountants adopted that new approach.

Most recently there are discussions about immutable mutual digital distributed ledgers using cryptographic technologies. One technology that can be used to implement a digital distributed ledger is blockchain. People are calling this "triple-entry accounting". Some say that triple-entry is the most important invention in 500 years. Basically what triple-entry does is create a link between the two double-entry systems documenting that the transactions in the two systems go together.

There is a little bit of a dispute around the true meaning of "triple-entry". Yuji Ijiri was first credited with using the term but the blockchain folks seem to have perhaps redefined the terma bit. I am using the term "triple-entry" as the blockchain people and Ian Grigg tend to use the term.

Here is the bottom line:

- A single-entry is not much more than a glorified list.

- Double-entry is in essence posting a transaction to two different single-entry ledgers with different parties responsible for each ledger. When you use a double-entry ledger what the transaction represents has to be explained by reasoning, the two transactions logically go together. Removing or changing part of the transaction will make the transaction illogical. Double-entry allows for the detection of errors and the differentiation of an unintentional error from fraud.

- Triple-entry further builds on double-entry in that triple-entry links a transaction in two double-entry ledgers and the link is publicly available for all to see the transaction. You are still able to explain the reasoning behind the entry but additionally the transaction is visable for all to see which makes it very tough to lie since others are watching. It would be illogical for the transaction to not be reflected the same in both ledgers.

With the volume of transactions growing and complexity increasing; triple-entry accounting intuitively seems like a potentially valuable tool. Perhaps those experimenting with triple-entry accounting might come up with something useful.

################################

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments