Enterprise Common Business Reporting Model

Andrew Noble and I wrote the essay below and seem to each reach two conclusions:

- Financial reporting more naturally belongs in a computer assisted digital world than in a paper-based or what amounts to “e-paper” based world. (Also, maybe loose the report and embrace the information hypercube. Algorithmic regulation is an idea whose time has come.)

- XBRL-based reports enhanced by SBRM logic and the notion of a powerful but safe and reliable logical system model provides an excellent foundation for what amounts to an “Enterprise Common Business Reporting Model”.

Here is the full essay:

A general purpose financial statement is itself not an “economic entity”. This is similar to how a “map” is not the same thing as the territory the map represents.

A general purpose financial statement is a high-fidelity representation of information about an economic entity that tries to be as true and fair as possible following a set of agreed upon accounting assumptions (e.g. going concern, recognition, measurement, and so forth). The general purpose financial report is a model that represents the financial position and financial condition of that economic entity.

Businesses, banks that provide businesses capital, equity markets that provide capital, and regulators have been using this financial reporting “system”, "the model", for quite some time. And so, over the years they have been agreeing on and tuning this model. This has been going on for years and years. Standards setters act as referees.

The model is not perfect. Stakeholders within this system have complaints. For example, the historical cost assumption is questioned because of the big gap in book values as contrast to market value. Or, the equity markets say they want more information about non-financial items. As such, the standards setters make adjustments to the rules such as adding fair value measurement rules to the system. No stakeholder of this systems gets 100% of what they desire, but the system works fairly well and is slowly adjusted to make the system work better.

And so, the system and the model exist in a state of perpetual refinement.

What we are doing with XBRL is to take this model which here-to-for has been represented on a piece of paper or a piece of “e-paper” and putting that existing model into machine-readable form. XBRL is a purpose-built syntax for representing financial or nonfinancial information in machine-readable form. XBRL is not the only syntax that can do this. The semantic web stack’s RDF/OWL/SHACL could be used, or Prolog, or other ontology-like thing. To be effective, that syntax needs to be able to capture the currently used model effectively and, in some way, make the system better, faster, and cheaper.

What is particularly interesting with respect to the model of a financial report is that it has a lot of very nice “features” that make it incredibly amenable to being represented logically using a model and worked on with a computer. First, the model is based on the “double-entry bookkeeping model” (DEBITS = CREDITS) which provides what amounts to a parity check that can be used to detect errors and distinguish an unintended error from an intended error (i.e. fraud). Second, the model is based on the accounting equation, “Assets = Liabilities + Equity” which adheres to that same double entry bookkeeping model which provides what can be called “scaffolding” or “keystones” for the financial reporting model. Third, every financial reporting scheme created provides a conceptual framework (i.e. US GAAP, IFRS, IPSAS, GAS, FAS, FRF for SMEs, etc.) which defines a set of core “elements of a financial statement” used within that financial reporting scheme (e.g. assets, liabilities, equity, comprehensive income, investments by owners, distributions to owners, revenues, expenses, gains, losses) that reconcile to the accounting equation, expand that high-level scaffolding as required by that financial reporting scheme, intentionally interrelated those core elements which cause what is referred to as “articulation[4]” where the core financial statements (balance sheet, income statement, changes in equity, cash flow statement) are all carefully “intertwined” which provides yet another layer of quality control.

Finally, such a financial reporting scheme is a very narrow use case as contrast to a broad general use case. Those that operate within this system using this model within this very narrow and well-defined domain are all highly trained “experts”. Certified Public Accountants (CPAs) or Chartered Accountants (CAs) have four or more years of specific university training and are required to take a national certification exam and are certified. Certified Financial Analysts (CFAs), likewise take many of the same university courses as CPAs and also pass a rigorous and comprehensive certification exam. Further, these experts have been honing, and honing, and honing their common understanding of “terms” and “associations between terms” and “structures” and “assertions” for over a hundred years now. All this information has been documented in the Accounting Standards Codification (ASC) for US GAAP or the IFRS standards for IFRS, etc. If you compare and contrast the different financial reporting schemes, they are far more similar than they are different.

What I am pointing out here is that financial reporting is not like all other reporting domains or others trying to exchange information within their respective domain. There are other domains that likewise have experts within their domains, good boundaries, etc. And there are other domain still where the users are not experts, they have no specific common training, and the domains they are trying to represent with ontology-like things are very broad and so they tend to struggle to create a common model. And because the user base is so broad, the domain is so broad, it is no wonder that they cannot agree on a model, believe that there is no “perfect way to represent the truth…”, and are not really motivated by any specific goal or objective to agree so they tend to get stuck in philosophical debates.

Users of financial reporting schemes already understand that the goal is to agree and to create something that works. The financial reporting model already works. What is different now is that before the agreement was achieved using best practices and paper-based reports that were not machine-readable. But now, many of these reports are readable by machines and a skillful craftsman using the right tools can poke and prod financial reports and understand things that were impossible to understand before because performing tasks manually was so time consuming and costly. This opens up a whole new world of possibilities.

Something that seems to be true is that this financial reporting system appears to have been designed for something like a computer all along. But computers did not exist in 1211 when double entry bookkeeping was invented, or in 1494 when it was documented by Luca Pacioli, or in 1929 after the stock market crash when US GAAP was established, or computers were not widely used in 1973 when they began creating IFRS. So, financial reporting was being practiced using paper or what amounts to “e-paper” which is not machine readable. But financial reporting schemes have now found their rightful home here in the digital age or information age or what some people are calling the fourth industrial revolution or the age of artificial intelligence.

It is far more natural for financial reporting to be practiced using computers than using paper.

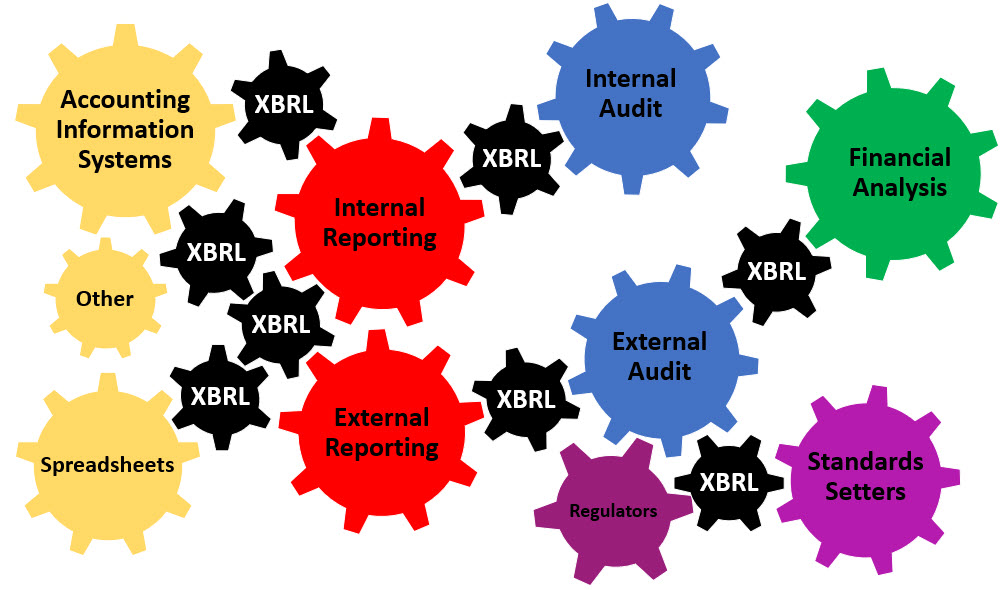

Financial reporting is central to all enterprise reporting. This is because enterprises live or die based on their financial performance. Enterprise information systems are primarily configured to capture the activities of the enterprise and in general, all enterprise activities ultimately trickle down to being reportable activities. Even if reporting is not explicitly financial reporting, information contained in the reports should conform to the general enterprise information model and the reports should be structured in a semantically consistent manner for each and within each enterprise. It's therefore imperative that any reporting model consider the flow of information through an enterprise and ensure that the model is general enough to handle the reporting of all enterprise information and is specific enough to handle the special case requirements of financial reporting.

It would be absurd for each individual enterprise to be forced to use one common semantic model for all of their internal and external reporting. It would be likewise absurd for each individual enterprise to develop their own unique reporting model. A middle ground is for all three needs to be met with one common reporting scheme that was configurable for each individual enterprise, a proven and rock-solid model that each enterprise did not have to independently invent, and a global open standard model that met the needs of the enterprise but also the needs of the global financial reporting supply chains that exist.

XBRL plus the ideas of the Standard Business Report Model (SBRM) could be that enterprise global standard common business report model. That model does not require the use of the XBRL technical syntax internally, but it does allow it and for the logical model of whatever syntax is used, say RDF/OWL/SHACL or Prolog or really any other syntax, to be converted to the same logical model used by XBRL. That is what the Special Theory of Machine-based Automated Communication of Semantic Information of Financial Statements tries to point out.

(Click image for larger view)

To understand more, consider watching the video playlist that helps you understand the financial report logical system. Or, maybe read this.

#################################

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

7 References

7 References

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to FriendReferences (7)

-

Response: 5 best Keyword tools for SEO

Response: 5 best Keyword tools for SEO -

IACVE offers different types of best advanced digital marketing courses and digital marketing certificate courses and you can ask our professional teacher about digital marketing courses. Delhi has become the hub of digital marketing courses and students from different states are joining the digital marketing course online or offline. You can ...

-

Response: Indian Federation of Yoga (IFY)Diploma in Yoga - Indian Federation of Yoga designed course Diploma in Yoga is one of the best yoga course and that gives in-depth training in yoga theory and practise. This course is intended for students who desire to pursue a career as a yoga teacher or who want to expand ...

-

Response: Limited Company RegistrationThe process of forming a new company in India under the Companies Act, 2013 or the Companies Act, 1956 is known as new company registration. A Certificate of Incorporation, which attests to the company’s legal status, must be obtained from the Registrar of Companies (RoC) as part of the registration procedure. ...

-

Response: Social Media Marketing Trends

-

Response: Indian Federation of YogaDiploma in Yoga in Himachal The Comprehensive Guide to Diploma in Yoga Offered by the Indian Federation of Yoga Yoga, an ancient practice with roots deep in Indian tradition, has gained global recognition for its holistic approach to physical and mental well-being. Recognizing the increasing interest and demand for a structured ...

-

Response: Top Project management softwareExplore the Best Enterprise Project Management Tools. Get insights into the leading Enterprise PPM software for strategic project portfolio management optimization.

Reader Comments