Does Anyone Else Grasp the Importance of This?

This page details what I explained in this blog post. I am curious as to whether anyone else grasps the importance of what I am seeing here: (if this makes sense to you, please let me know; if not, let me know what might be missing)

- Take a set of journal entries. Here they are in machine readable XBRL Global Ledger format and Plain Text Accounting format. Here is the same information in human readable Excel and PDF.

- Import the journal entries into an accounting system such as Ledger, hledger, my Microsoft Access Database, or any other accounting system for that matter. You can then do things with that information.

- Within the accounting system you can generate things like a trial balance of accounts (status of each account), a roll forward for each account (impact of transactions on account), filter information using the information provided in the journal entries.

- But, the accounts are a flat list.

- You can get a trial balance of accounts. You can get a summary of the changes grouped by the type of change. You can put those two together and get a roll forward of each and every balance sheet account: Cash and cash equivalents; Receivables; Inventories; PPE; Accounts payable; Long-term debt; Retained earnings.

- However, if you use information such as that provide in an XBRL taxonomy, about the model of a report; you can both organize the accounts into a hierarchy and control the process of creating such a hierarchy. Here is that XBRL taxonomy schema in machine readable form.

- Using only the journal entries and the XBRL taxonomy for the report you can generate a machine readable report; here is that XBRL instance. (Less than 100 lines of code were used to generate the information that makes up the XBRL instance, mainly a bunch of SQL INSERT statements.)

- The machine-readable journal entries, machine-readable report model, machine-readable reported facts, and machine-readable rules enable the automation of many audit tasks. For example, this analysis of transaction change codes by account is consistent with expected relations matrix was created simply by reading the XBRL-based journal entries. Variance analysis, peer analysis, many account analysis steps, and many other internal audit and external audit tasks and processes can be effectively automated.

- A software application can turn that XBRL instance into a human readable report. Here is that same report formatted as Inline XBRL. The report could be static like a traditional financial report or dynamic (think pivot table).

- If you don't like the auto-generated human readable report you can do a little more work to specify formatting; then you can generate a pixel perfect human readable rendering that is also machine readable. You can also generate PDF (that is from another example) if you desire using a similar process. (I don't have an example, but you could also generate a Microsoft Word document in this manner.)

- Both the Inline XBRL and the Raw XBRL enable information to be reliably extracted from the reports for down stream processes such as analysis of the information.

- This entire process is controlled and monitored by machine readable rules that will point out any mistakes in the information to the extent that machine-readable rules exist. Mathematical computations are monitored by rules, rules, and more rules. Structural rules monitor the information structure. Disclosure rules (i.e. reporting checklist) monitor what is disclosed as contrast to what is required. The more machine-readable rules, the more work can be automated.

- Quality control checks and third-party checks can be done using the machine-readable journal entries and reports to automate a portion of those processes.

- Professional accountants can focus on value-add activities such as financial analysis and less on the gruesome, grueling, monotonous, repetitive tasks.

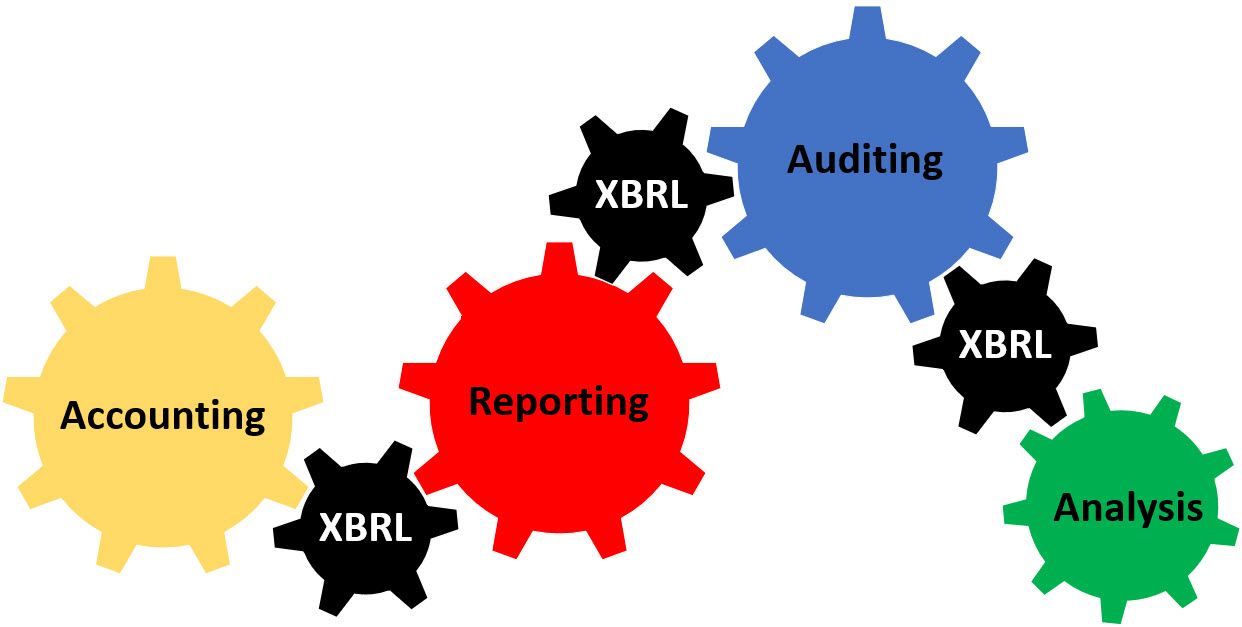

This simple example has all the moving parts of a larger set of journal entries and a larger report, say the 10-K financial reports for a company like Microsoft. Apple, Amazon, Facebook, Google, and Salesforce all work the same way.

BOTTOM LINE: This is a demonstration of how to automate accounting, reporting, auditing, and analysis processes using the global standard XBRL and the Standard Business Report Model (SBRM). This example has 100% of the required information (i.e. metadata) to move from journal entries to report. This process was created in a Microsoft Access database application using mainly SQL queries and basic VBA programming. Likewise, all the rules used in the control/monitoring process were created in Microsoft Access. Off-the-shelf software for working with XBRL ran the rules. Four different software applications get identical results (XBRL Cloud XRun, XBRL Cloud web service, UBmatrix, Pesseract).

For more information see here and here. Information quality matters. Expose the hidden data factory that corrects errors.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments