XBRL-based Digital Financial Reporting Jump Start

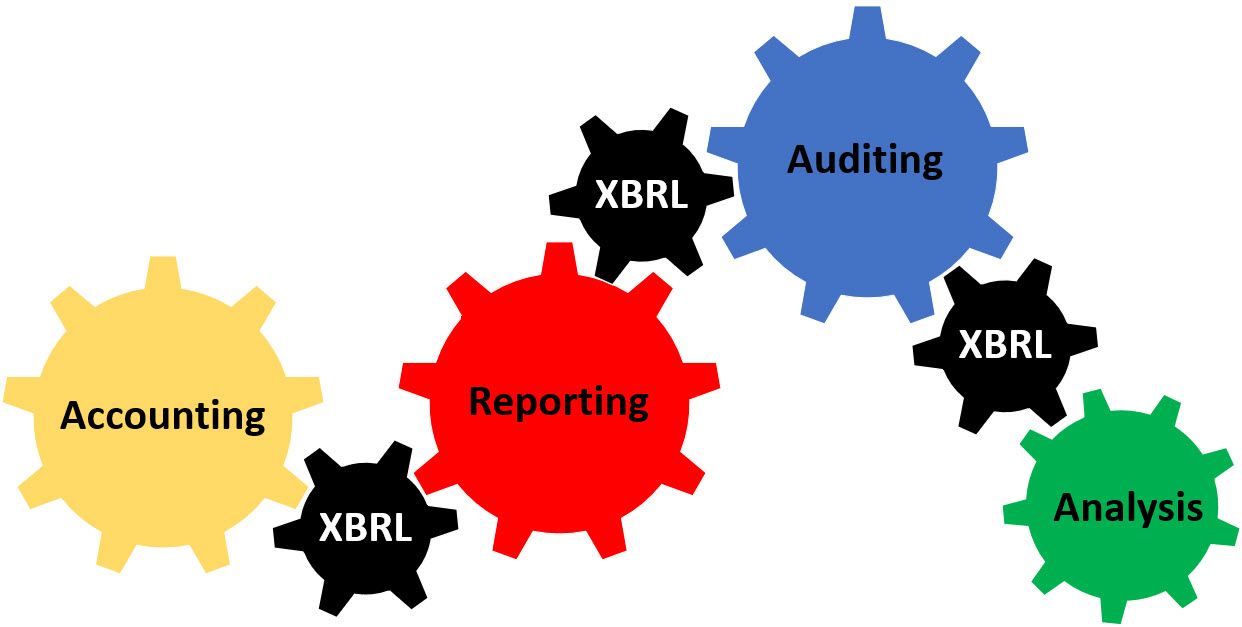

Auditing is broken. Old school financial reporting processes are inefficient. Accounting is inefficient. Analysis tends to be too manual. Accounting, reporting, auditing, and analysis needs to move to 21st century techniques.

Old technologies are making it increasingly difficult to keep up with today’s fast paced information exchange. New technologies such as structured information, artificial intelligence, digital distributed ledgers offer significant and compelling opportunities to make accounting, reporting, auditing, and analysis tasks and processes more efficient and effective. But figuring out how to employ these new technologies and finding people with the necessary skills and experience to analyze systems and fix problems can be challenging. What if there were a standards-based proven best practices method you could use to improve your productivity?

The difference between "custom", a "product", and a "commodity" is explained in this blog post, Properties of Products. In summary,

- Custom: Means unique to each individual customer. No attempt is made to standardize.

- Product: Found repeatable patterns (clusters), created a product for each pattern. Standards can be used. (As Malcom Gladwell explained in a TED Talk, "The answer is that there is no best pickle or spaghetti sauce. But there are best clusters of pickles and spaghetti sauces.")

- Commodity: Generalize the product so much that it is fungible, indistinguishable. Standards can be used.

An XBRL-based digital financial report should be indistinguishable in terms of quality. Are their customers that consciously want low quality? That would be absurd. As such, high-quality XBRL-based digital financial reports should be a commodity.

"Custom" is not scalable. While standard approaches do allow scaling.

Companies should not compete as to whether they can or cannot create high-quality XBRL-based reports. We need ALL such reports to be of high quailty. Companies should compete in terms of value added above and beyond fundamental quality, building on top of a rock-solid digital financial report foundation. Why? So we can reliably and predictably do this:

If XBRL-based reports fundamentally do not work reliably, then such reports are nothing more than an expensive garbage collection scheme. But what if they do work?

I have put together a series of documents that can jumpstart your understanding of XBRL-based digital financial reporting. Those documents add up to a total of 161 pages. If you want to make a small investment, you can learn about XBRL-based digital financial reporting and how those techniques also apply to accounting, auditing, and analysis. Here are the documents in the order that I would suggest that you read them:

- Understanding Proof: Proves that XBRL-based reports can work and shows you what such a working report looks like and is capable of. (30 pages)

- Understanding Method: Explains, at a high level, a proven, reliable, best practice method for implementing XBRL-based digital financial reporting following the forthcoming OMG Standard Business Report Model (SBRM). (35 pages)

- Understanding Digital: Helps professional accountants get their heads around important aspects of digital related to accounting, reporting, auditing, and analysis. (84 pages)

- Understanding Semantic Shreadsheets: Takes the ideas of XBRL-based financial reports and generalizes them to business reporting. (12 pages)

Not saying that the documents are perfect; they are the best that I can put together currently. Myself or others will improve this information even more over time.

Want to make a bigger investment? Watch this video playlist and/or read Mastering XBRL-based Digital Financial Reporting.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments