BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries in Modeling Business Information Using XBRL (213)

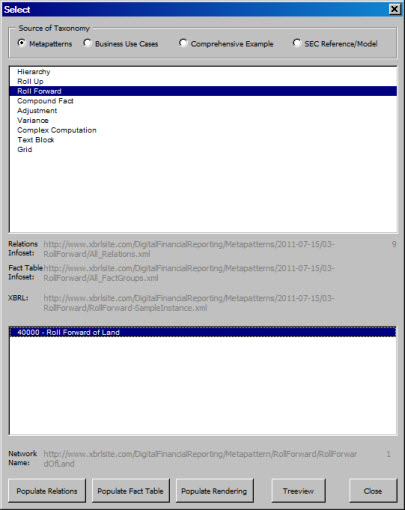

Relations, Fact Table, Rendering Viewer

I created a prototype application using Microsoft Excel which allows you to see even better how using infosets, rather than working with XBRL directly, can make your life easier. The Excel prototype is a great learning tool also. It lets you better see what the information articulate by XBRL communicates.

The prototype hooks directly to the metapatterns, business use cases, comprehensive example, and SEC reference/model samples/examples which I have created. It lets you have a closer look at the meaning of information articulated within an XBRL taxonomy and XBRL instance. All the business use cases which I have run across are covered.

The rendering does not work as well as I want at this point because it does not leverge the information models (the metapatterns) yet and it does not support more than one [Axis] on columns or rows.

All the infosets have been pre-processed for these samples/examples in advance for these examples (complements of XBRL Cloud) which contributed two style sheets which transforms their infosets to the format which I use. That means that this application does not even need to use an XBRL processor. The infoset format is my strawman implementation of the Business Reporting Logical Model (BRLM) created by the XBRL International Taxonomy Architecture Working Group. I have since abandoned that implementation format in favor of the US GAAP Taxonomy Architecture model which is used by SEC XBRL financial filings. That model is documented here. The two models are, however, interchangeable.

Charlie

in Demonstrations of Using XBRL, Modeling Business Information Using XBRL

|

Charlie

in Demonstrations of Using XBRL, Modeling Business Information Using XBRL

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Understanding the Role of an [Axis] in an SEC XBRL Filing

If you look within SEC XBRL filings you can see that their creators still have confusion about what exactly an [Axis] does.

As explained in on the SEC XBRL Financial Filing Glossary and Logical Model, an axis is:

A means of providing information about the characteristics of a fact reported within a business report.

Nothing scary or technical about that explanation and that is all an axis really is. Now, some people refer to an axis or [Axis] as seen in XBRL taxonomies using other terms which can make them seem confusing. Some common terms are: dimension as used in the XBRL Dimensions specification, aspect as used in the XBRL Formulas specification, measure as used in the multidimensional model and in the Business Reporting Logical Model, to name most. I will use [Axis] as used in the US GAAP Taxonomy and in SEC XBRL financial filings.

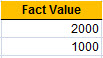

But what exactly does an [Axis] do? Walking through this will make exactly what an [Axis]. Consider the following two facts:

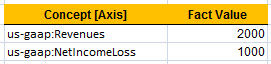

The two facts have values. What do those values mean? Well, you don't really know, you need more information. So, you add an [Axis] to provide additional characteristics. Now, consider this next screen shot:

So above, I added the Concept [Axis] and provided values for each fact to both explain and differentiate the two fact values. The value of an [Axis] is called a [Member]. We still don't have quite all of the information we need yet, this next screen show will make that clear:

So now we are getting closer and closer to something which is becoming useful. Knowing the period and the entity reporting the fact, in the case of SEC XBRL financial filings the CIK number, is commonly desired. In fact, it is so common that XBRL requires these three [Axis] on every single fact: the concept, the period, and the reporting entity.

But, do we have enough information? Well, that depends. Take a look at the next screen shot and we will bring up a few more things about an [Axis].

XBRL provides the ability to add even more, in fact any number of, [Axis]. Here we added the business segment [Axis] and indicated that our fact values both relate to the the consolidated entity.

When do you know if you have enough [Axis]? Well, that is dependent on whether you have communicated all the business information you are required to communicate. A fact is comprised of a value and all the characteristics which describe that value. There is nothing technical about what an [Axis] does so don't let a poor software implementation or some consultant who speaks using $150 an hour jargon tell you any differently. Yes, it really is that simple and straight forward.

Rather than complicating this explanation with more details, I will call this good. You can find more definitions of the report elementswhich make up an SEC XBRL financial filing in that same glossary.

I will go into some of the more common mistakes I am seeing in SEC XBRL financial filings later.

Charlie

in Modeling Business Information Using XBRL

|

Post a Comment

| Email

| Print

Video Overview of XBRL Abstract Model Created by XBRL International

XBRL International held a webinar which explained the UML model they are creating for XBRL, referred to as the XBRL Abstract Model. You can watch this 1 hour 34 minute video on YouTube here.

For those serious about understanding XBRL, this video is worth investing in. As stated in the webinar, XBRL International is trying to create two models:

- Primary model: Models semantics.

- Secondary model: Maps modeled semantics to the XBRL technical syntax.

One of the most useful aspects of this video are the very, very good questions which were asked. The webinar stated that a public working draft of this model would perhaps be available in October.

The semantic model which I have created can be found here. My model, which would fit into the model I saw in the webinar, is more focused on financial reporting and tends to be at a higher level than the model created by XBRL International.

Charlie

in Modeling Business Information Using XBRL

|

Post a Comment

| Email

| Print

Updated list of Exemplars

I am updating my lists of exemplars, cycling back and making everything consistent. If you don't know what I am talking about when I say exemplar, search this blog site and/or read Modeling Business Information Using XBRL.

More to come.

Charlie

in Modeling Business Information Using XBRL

|

Post a Comment

| Email

| Print

Unofficially Declare that Using SEC XBRL Income Statement Information Maddening

I unofficially declare that using the information from the income statement of SEC XBRL financial filings maddening.

While it is true that I am not a professional programmer, in fact I am not very good and have been referred to as a "dinker"; I do understand some of the things which are helpful in using information and things which get in the way of using information.

Now, the balance sheet and cash flow statement are a cake walk. The reason is that there are totals and subtotals which you can use to check to be sure you are grabbing the right information on both the balance sheet and cash flow statement. The structure of balance sheets and cash flow statements between filings is very consistent. You can calculate or impute information and there is generally something to check what you impute against to be sure you are getting things right.

There is little of these types of things when it comes to the income statement. What is more there are other things which just get in the way. For example, I thought I was getting Net Income (Loss) correct because I was at least finding the numbers in the filing. But what I realized is that there is duplication of concepts in the SEC XBRL financial filings. Duplicate values for Net Income (Loss) exist if the filer has a noncontorlling interest. Seeing as 21% of all filers have a noncontrolling interest, I cannot be sure I am grabbing the correct Net Income (Loss) concept. There is a big difference between getting some number and getting the right number.

It seems as though the details are there. If the roll up of the income statement is correct and if the detail is there (it matches the HTML so it likely is), then you can get to the pieces you want. But as far as I can see, this could be a task which needs to be done for each and every SEC filing to make comparisons work well and to be able to provide, say, an aggregate value for revenues, net income (loss) or other such reported facts across all SEC XBRL financial filings or some subset of filings.

The good news is that it does look like it is quite possible to use this information.

Charlie

in Modeling Business Information Using XBRL

|

Post a Comment

| Email

| Print