BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from April 1, 2020 - April 30, 2020

FERC

The XBRL taxonomy for the Federal Energy Regulatory Commission (FERC) can be found here. There are about 650 companies that file reports to FERC using XBRL. There are about 11 different types of forms that could be filed.

You can look at the FERC taxonomies here.

FERC is not using extensions. Taxonomies essentially follow the structure of each form. Currently they have about 10 forms. Each form has schedules. Every schedule has a hypercube (they use the term Table). Each reported fact is associated to at least one hypercube.

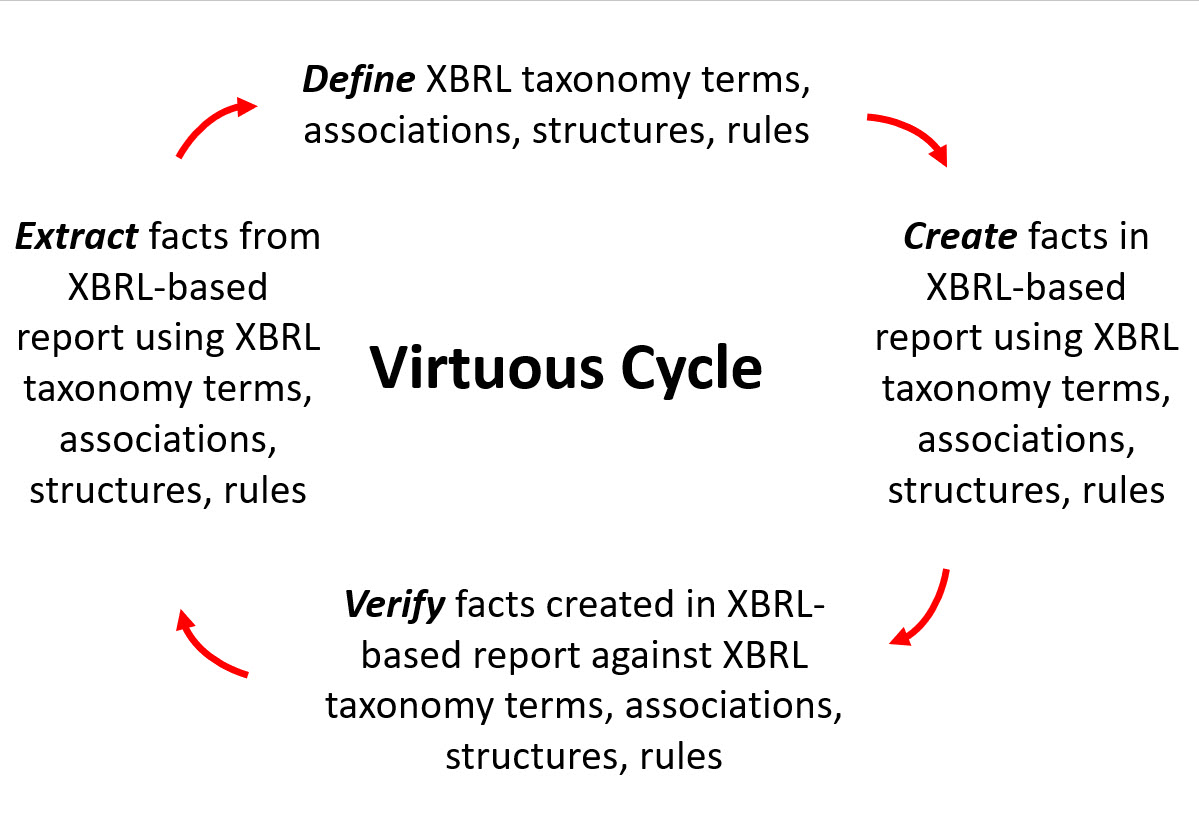

Virtuous Cycle

When a system is working right, it creates a virtuous cycle.

The terms virtuous cycle and vicious cycle refer to complex chains of events that reinforce themselves through a feedback loop.

- A virtuous cycle has favorable results.

- A vicious cycle has detrimental results.

The Financial Accounting Foundation (FAF) uses the notion of a virtuous cycle and feedback loop to show the value of quality accounting standards and financial information that is clear, concise, comparable, relevant and representationally faithful:

The Financial Accounting Standards Board (FASB) uses the notion of a virtuous cycle to point out the value of technology to investors:

Here is another virtuous cycle to consider: a proper functioning financial report logical system. Here is what I mean.

I created a prototype XBRL taxonomy for financial reporting by a not-for-profit organization. My intension was to create everything that is necessary to help me make sure I created the report correctly. Rather than using a "pick list" type of approach that the US GAAP and IFRS XBRL taxonomies use; I used a model based approach. I considered all the dynamics that impact a financial report logical system.

What I found is that the system created in that manner provides a virtuous cycle, a feedback loop, that helps make defining XBRL taxonomies, creating reports, verifying reports, and extracting information from reports all work more effectively.

Rather than viewing these tasks as individual silos; if viewed as a system all this becomes quite obvious.

As authors Gerald C. Kane, Anh Nguyen Phillips, Jonathan R. Copulsky, and Garth R. Andrus point out in their book The Technology Fallacy, it is a myth that technology is behind digital transformation. People are behind such transformations. The authors define digital maturity as follows:

Digital maturity is primarily about people and the realization that effective digital transformation involves changes to organizational dynamics and how work gets done.

The technology and know-how exists to make XBRL-based digital financial reporting work effectively. The question is does the will exist. It really would not take much to turn the existing vicious cycle of quality problems related to XBRL-based financial reports submitted to the SEC into a virtuous cycle.

The question is not "if" this virtuous cycle will ever be created, it is more a matter of "when" and "who" will be the first.

This YouTube video, Virtuous Cycle, provides a bit more detail should you be interested.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Alternative Approach to "Pick list" type XBRL Taxonomies

Today, many important XBRL-based taxonomies are being created as what amounts to human-readable "pick lists". In fact, that term "pick list" was used by people at the FASB to describe the US GAAP XBRL Taxonomy. Here are three examples of XBRL taxonomies that are essentially "pick lists":

PICK LIST BASED APPROACH:

So, what is the alternative to these "pick lists"? Why is the alternative better?

The alternative is to use a model-based approach to representing the XBRL taxonomy so that the information in the XBRL taxonomy is machine-readable but also readable by humans. The benefit of using a model-based approach is that you can control reports created using the XBRL taxonomy ensuring that they actually work effectively. Here are examples of XBRL taxonomies using a model-based approach.

MODEL BASED APPROACH: (model driven architecture)

- Not-for-profit (US GAAP) XBRL Taxonomy (working prototype) (Also see this for full machine-readable and human-readable documentation)

- Other model based approach examples

So, what is the actual difference between the "pick list" as contrast to the "model-based" approaches? Here you go:

- Consistency: The model-based approach is extremely consistent whereas the pick list based approach is far less consistent. For example, the model-based approach uses XBRL International's best-practice guidance related to the use of XBRL Dimensions. Every disclosure is consistently represented using a uniquely identifiable hypercube.

- Smaller, identifiable pieces: The model-based approach results in many more smaller easily identifiable pieces as contrast to the pick list approach which tends to create fewer pieces and crams "stuff" together in a far less organized manner.

- Guarantied quality: The model-based approach provides far, far more machine-readable rules that have four roles. First, the rules are used to verify that the XBRL taxonomy has been created correctly. Second, those same rules provide explicit guidance as to how to construct disclosures using the XBRL taxonomy by those creating reports. Third, those same rules are used by automated processes to verify that the report has been created consistent with expectations. Fourth, those same rules are used to effectively extract information from the XBRL-based reports. It is the rules that both provide and enforce the guarantee!

- Easier to use: The model-based approach is easier to use because complexity is moved from those creating reports to those creating the XBRL taxonomy. Further, that complexity is hidden from the user by software applications that leverage the well created XBRL taxonomy and all of the rules. Essentially, business professionals need only concern themselves with one thing: business logic of the information being represented. That, they understand.

- Easier taxonomy maintenance: With the model-based approach taxonomy maintenance is easier. Why? First, the pieces are smaller and significantly easier to manage. Second, all those rules make it virtually impossible to inadvertently break the taxonomy. Essentially, taxonomies that use a model-based approach have a built in test harness.

- Significantly improved taxonomy functionality: Model-based XBRL taxonomies are a web of information. Just look at all the relations for a disclosure.

Pick list-based and model-based XBRL taxonomies are not mutually exclusive. Contrast these two example disclosures for the components of inventories for my Not for Profit prototype and US GAAP. You can turn a pick list XBRL taxonomy into a model; or you can turn a model-based taxonomy into a pick list if you so choose.

There is no impact on the actual terms. The impact relates to structures, associations, and rules. Models have identifiable structures, clear associations, and complete set of rules. Pick lists don't. Pick list based taxonomies leave a lot of information out; that is what causes the quality problems experienced by such XBRL taxonomies.

Here is an example of what you can achieve using a model-based approach. Consider this:

- Have a look at this report. Human-readable | Machine-readable

- Note that the report is comprised of 77 individually identifiable set of information. For example, "Document information" is one set, the "Statement of financial position" is two sets (i.e. Assets roll up, Liabilities and Net Assets Roll Up); count them all you will find a total of 77.

- This validation report shows that all 77 of those individually identifiable sets of information is consistent with expectation. (Note that the list has 58 items, but the Level 3 and Level 4 disclosures are listed together on one line in that validation report, but individually count as different information sets)

- This validation report and this validation report show that the mathematical relations are consistent. Here is another version of the same information.

- This validation summary provides a pretty good dashboard that helps you understand that the report is properly functioning.

And so, while software is not where it needs to be; a person that understands WHAT to look for and WHERE to look can confirm that a model-based report is properly functioning. You fundamentally cannot do this with a pick list based report; the information is simply not there. So what do you do? Add the information you need. Then, you will have a model based XBRL taxonomy for your report. But that does not make the underlying base taxonomy model-based; only the report.

Here, I created the rules that cover 95% of the 194 individual sets of information in the Microsoft 2017 10-K. Why only 95%? Because the other 5% I could not effectively represent because of extension concepts. (see the complete analysis here)

- SEC Filing Page

- XBRL Instance

- Human readable validation report

- Disclosure Mechanics validation (partial validation tool you can use, before I added the additional rules)

This video provides additional information.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Accounting Systems Need to Come Out of the 19th Century

In a Financial Review article, Accounting systems need to come out of the 19th century, Petter Wells points out that accounting systems are stuck in the 19th century. He points out how XBRL can be leveraged to improve audits:

100 per cent check

Professor Wells said adopting software such as XBRL would enable a computer-generated check of 100 per cent of audits, so the regulator could then look into just those flagged as problematic and not rely on its own classification of risk.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

AI as a Commodity Service

In my view, Evan Sparks is right in his Forbes article What Andreessen Horowitz Got Wrong about AI; artificial intelligence will be a low priced commodity.

Indeed, better software infrastructure for AI and Deep Learning development, coupled with commodity pricing on basic GPU and AI cloud services will do for the AI industry what Java, AWS, Intel, Hadoop, and hundreds of other companies and technologies did for SaaS.

Standards, standards, standards.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print