BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from February 1, 2020 - February 29, 2020

Mastering XBRL-based Digital Financial Reporting

Vince Lombardi pointed out, “Practice does not make perfect. Only perfect practice makes perfect.”

Digital financial reporting will undoubtedly play some sort of role in financial reporting. No one knows the exact role, but it will play a role. Recognize that mandated regulatory reporting using XBRL is NOT the only use of XBRL. Regulators like the SEC and ESMA are making too many mistakes.

If you want to master XBRL-based digital financial reporting here is how you do it.

(NOTE! I have summarized all of these resources into one document, Mastering XBRL-based Digital Financial Reporting. I am also putting a lot of this information into a video playlist Mastering XBRL-based Digital Financial Reporting.)

First, have a look a the following logical systems each of which has been properly represented in XBRL. The goal here is not to get into the details of XBRL at this point, rather the focus is to get the big picture and proper perspective as to what is going on. These will provide you with the proper fundamental grounding:

- Accounting Equation: Document | Files | Video | Video2 | Slides

- FASB's SFAC 6 Elements of Financial Statements: Document | Files | Video | Slides

- SFAC 6 Plus: Document | Files

- Common Elements of Financial Statement: Document | Files | Video | Slides

- Trial Balance: Document | Files | Video | Slides

- Journal: Document | Files | Video | Slides

- Proof Representation: Document | Files | Video | Slides

- Proof Representation 2: Files

- MINI Financial Reporting Scheme: Document | Files | Video | Slides

- XASB Financial Reporting Scheme: Document | Files | Video

- US GAAP Financial Reporting Scheme: Document | Files | Video (Working prototype)

- Not-for-profit (US GAAP) Financial Reporting Scheme: Document | Files | Video (Working prototype)

- IFRS Financial Reporting Scheme: Document | Files | Video (Working prototype)

- IPSAS Financial Reporting Scheme: Document | Files | Video (Working prototype)

- FRF for SMEs Financial Reporting Scheme: Document | Files | Video (Working prototype)

- Auditing XBRL-based Financial Reports: Document

NOTE: This is the most current MASTER version of the XBRL representations listed above.

Second, watch this 90 minute video play list: Understanding the Financial Report Logical System. This will help solidify your understanding of the financial report logical system and how it works.

Third, read the document Special Theory of Machine-based Automated Communication of Semantic Information of Financial Statements. That will fill in any missing details from the first and second steps.

Fourth, read the document Proving Financial Reports are Properly Functioning. That document helps you make the connection between the simple accounting equation and SFAC 6 logical systems and something like the Microsoft 10-K or any other financial report.

Five, read the document Artificial Intelligence and Knowledge Engineering in a Nutshell. That document provides critically important background information that helps you truly understand the first four documents.

Six, work through Intelligent XBRL-based Digital Financial Reporting. Explore these example XBRL-based reports. Download the Pesseract working proof of concept software application. Alternatively or in addition, watch the Pesseract video play lists. Here are more examples that might be useful to you.

Once you have a solid foundation: practice, practice, practice.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

1 Reference

|

1 Reference

|  Email

|

Email

|  Print

Print

XBRL Market Segmentation

Market segmentation is the process of dividing a larger market that appears homogeneous into groups with distinct but similar needs or wants. You then design products, pricing, and perception that match the preferences of each unique group.

Products that are used to create XBRL-based financial reports that are ultimately submitted to regulators such as the SEC or ESMA can allow errors because those regulators don't seem to care much about report quality.

However, when XBRL-based digital financial reporting is implemented within the enterprise, quality matters a lot. No organization in their right mind, large or small, would ever implement digital financial reporting internally if the new digital approach is not somehow better, cheaper, or faster than the current approaches that they use.

Will accounting, reporting, auditing, and analysis go digital?

Well, that is up to software vendors. Can software vendors create software that is better, cheaper, and/or faster than current accounting, reporting, auditing, and analysis approaches.

Public/listed companies that reoprt to the SEC and ESMA are mandated to do so. They have no choice; and so they are required to purchase something even if it does not work correctly.

Private companies do have a choice.

OK, so how do you create software that improves current accounting, reporting, auditing, and analysis approaches? You do that by being clever, creative, and innovative.

My document Special Theory of Machine-based Automated Communication of Semantic Information of Financial Statements documents proof that XBRL-based digital reporting can work and how to do make it work.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Digital Financial Reporting: The Big Picture in Pictures

Digital financial reporting can be explained by the following graphics. Note that you can click on any of the images to get a larger image. Also note, that this video also covers this information.

First, note that I am seeing the following trends in financial reporting that are evolving in their individual "silos" but will eventually integrate with one another:

- Machine-based digital reporting

- Human-machine collaboration

- Integrated reporting

- Push reporting

- Continuous reporting

- Continuous auditing

- Triple-entry accounting

- Algorithmic analysis/regulation

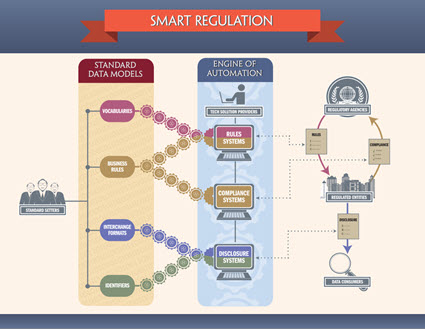

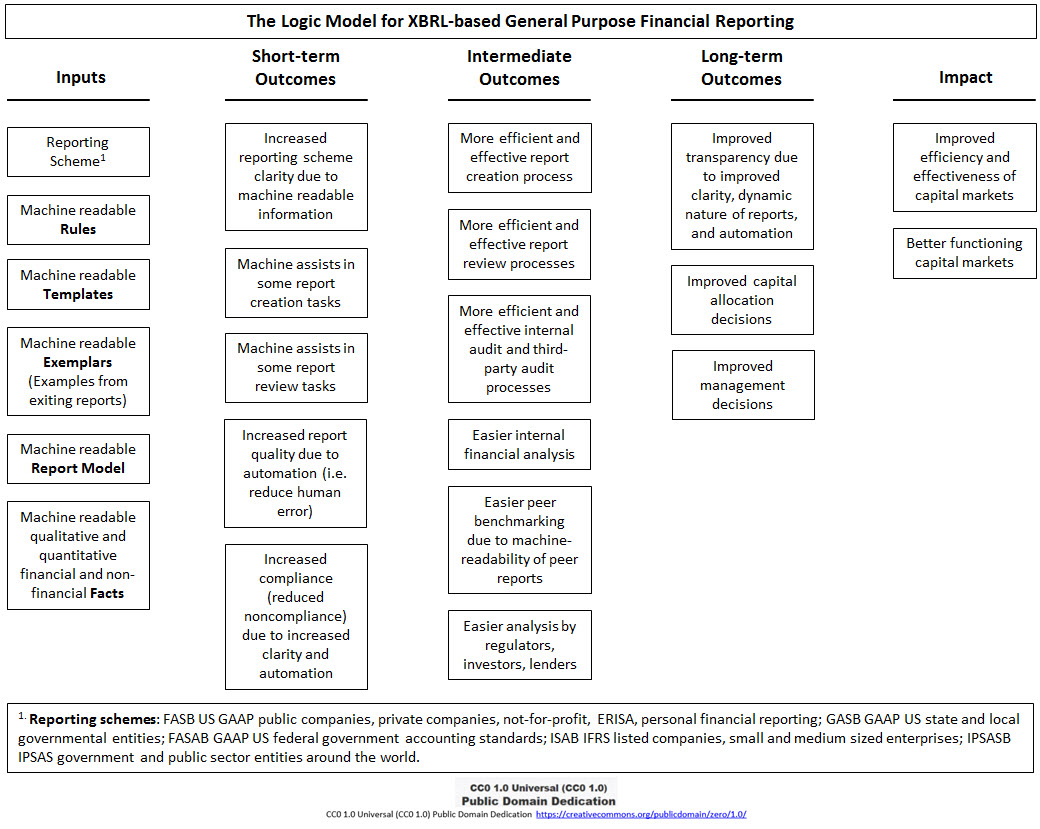

This graphic provided by the Data Coalition shows what they refer to as "Smart Regulation". In the graphic you see that they refer to "standard data models" (i.e. machine-readable rules) and the "engines of automation" (i.e. rules engines and artificial intelligence):

It is not going to be the case that enterprises keep their same old systems and "bolt on" new stuff, doing more work, just so that they can make regulation more efficient (but remain inefficient internally). And it will not be the case that each enterprise creates it's own model. Think of the notion of a global standard common enterprise model for any organization to improve their internal processes and tasks.

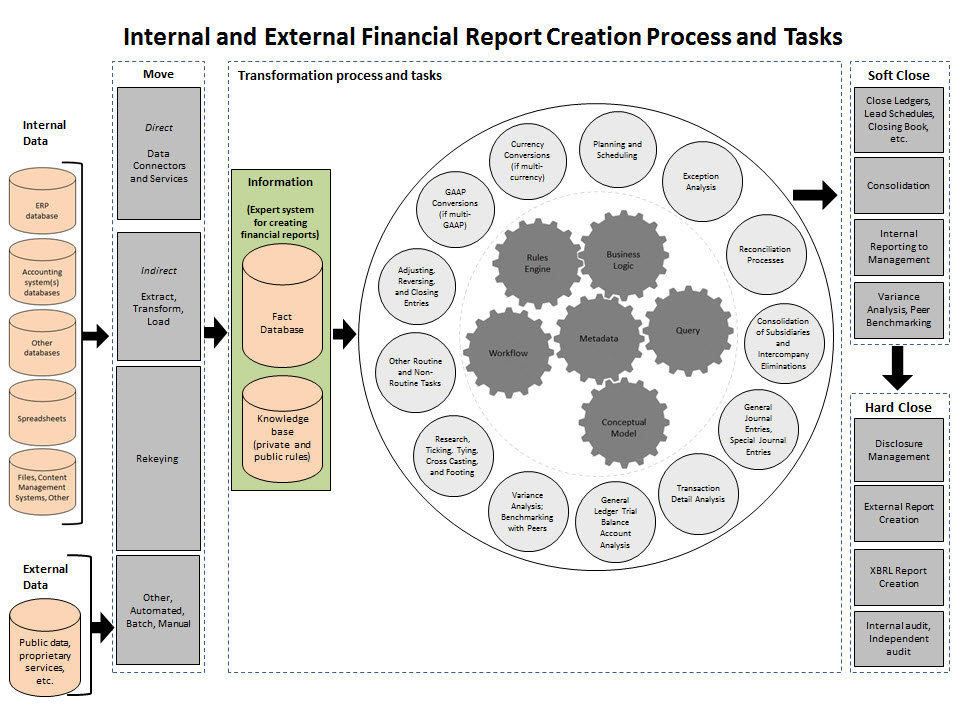

The inner workings or processes and tasks of a financial reporting system of a typical enterprise is explained by this graphic inspired a Blackline graphic related to continuous accounting which I built on:

Those processes and tasks are the candidates for automation. Will everything be completely automated? That is very doubtful. Will nothing be automated? That is likely doubtful also. The answer will be somewhere in between today's grueling, barbaric manual processes and the notion of "lights out finance" where the entire process is totally automated.

So, how will that automation be achieved?

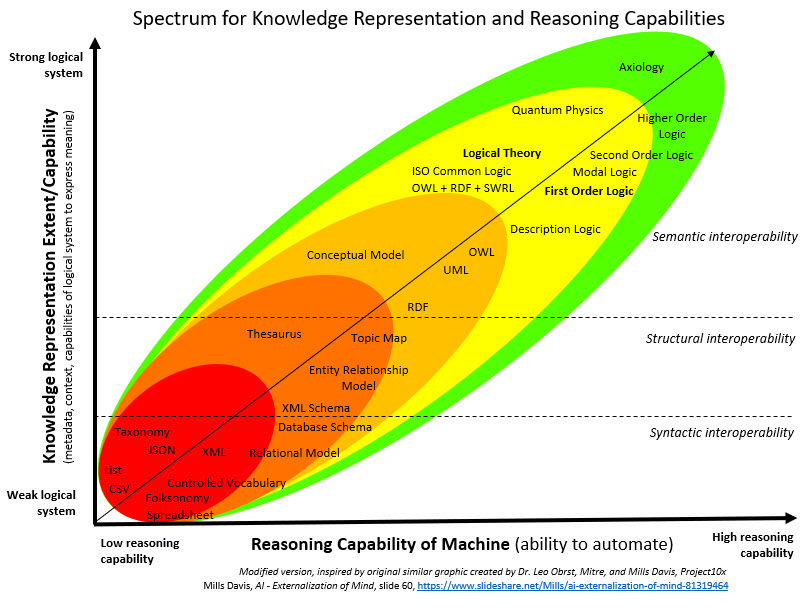

This graphic, inspired by a similar graphic created by Dr. Leo Obrst and Mills Davis on slide 60 of this SlideShare presentation, shows the relationship between knowledge representation capability of different technical approaches and of reasoning capacity that can be achieved within a software application:

Note that there are many alternative approaches, each has its set of capabilities, many different ways will work, and a logical theory is one of the better approaches because it is highly expressive.

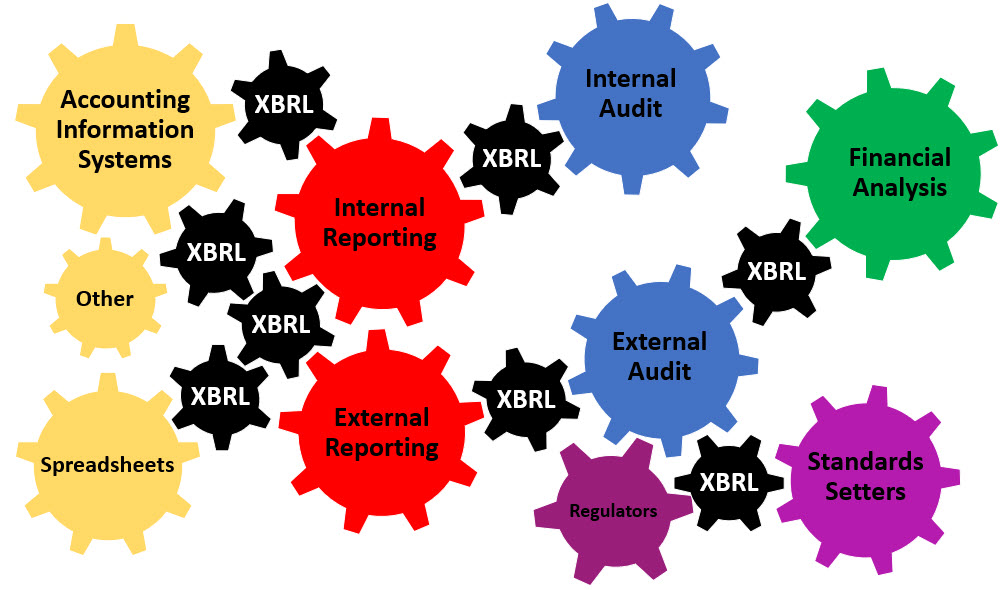

This graphic shows how global standard XBRL can be used to link different aspects of accounting, reporting, auditing, and analysis together so that information can be exchanged between tasks and processes:

So that is the big picture in pictures. This example small system helps you understand the details of how all this actually works.

I provide a more complete explain of the moving parts in the document Special Theory of Machine-based Automated Communication of Semantic Information of Financial Statements. This video play list, Understanding the Financial Report Logical System, provides an overview of that document.

To understand that document, it is best if you read Artificial Intelligence and Knowledge Engineering in a Nutshell go get important background information.

Why do any of this?

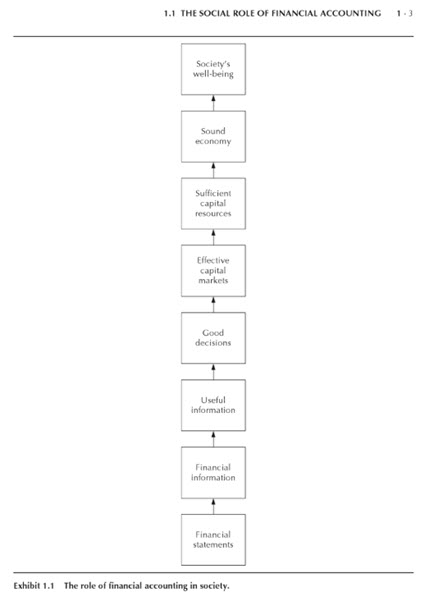

As pointed out in the Accountant's Handbook on page 3 (D. R. Carmichael, O. Ray Whittington, Lynford Graham); financial reporting benefits society and improving financial reporting increases that benefit:

And so, the business case for XBRL-based digital financial reporting is better functioning capital markets and an improvement in the well being of society:

What do you think?

Here is a visualization of the logical conceptualization of a financial report. The Financial Report Semantics and Dynamics Theory has the same logical conceptualization in narrative form. The OMG Standard Business Report Model (SBRM) standardizes and formalizes that model. XBRL is a global standard technical syntax for implementing that formal logical conceptualization.

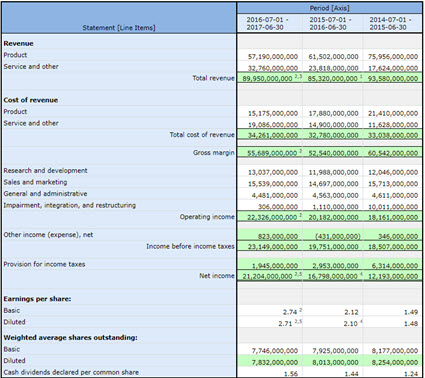

And so, what will this look like for accounting professionals, financial analysts, and other business professionals? Well, here is one version of what it will look like:

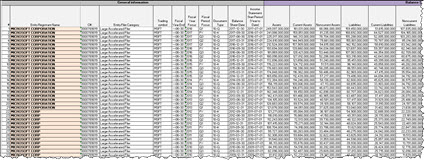

But it could look like many different things because software can reconfigure the pieces to suit your needs. For example, it might look like this Excel-based automated comparison of 33 Microsoft financial statements (click the image to run the Microsoft comparison or any comparison of 22 other public companies; alternatively, try one of these Excel extraction tools that compare information for thousands of public companies):

The possibilities are endless, digital financial reporting is just getting started! If you want more details, Intelligent XBRL-based Digital Financial Reporting likely has what you are looking for.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Trends in Financial Reporting

Financial reporting will be different in the fourth industrial revolution. There seems to be a number of trends that are interacting with one another in the realm of financial reporting. This is a summary of what I see:

- Machine-based digital reporting: Machine-based digital reporting will likely prevail over the historically prevalent exchange of paper or e-paper by humans. (See this)

- Human-machine collaboration: Machines working along side humans to perform work much like a calculator helps humans do math, as contrast to the current overly manual processes. (Think good-old fashioned rules-based expert systems like TurboTax.)

- Integrated reporting: Sometimes called "triple-bottom line" or "sustainability reporting" or "ESG" as contrast to simply financial reporting. (Check out Larry Fink's letter to CEOs related to climate change.)

- Push-reporting: Push-based reporting as contrast to pull-based reporting. (Example)

- Continuous reporting: Continuous reporting as contrast to the historical "batch" oriented mode of reporting. (See the Finance Factory)

- Continuous auditing: Continuous auditing and AI assisted auditing using things like the dynamic audit solution as contrast to older audit approaches. (See Imagineering Audit 4.0)

- Triple-entry accounting: Triple-entry accounting leveraging digital distributed ledgers as contrast to double-entry accounting which is internally focused.

- Algorithmic analysis/regulation: Algorithmic regulation or "smart regulation" as contrast to older approaches which tended to be more manual.

Center to all of this is the financial report logical model, enabling a new modern approach to financial reporting. Software interacts with that model to put things into a report, make sure the report is right, extract information from the report for analysis, etc. Machine-readable metadata glues everything together logically, enabling very significant automation.

Imagine a financial report (or business report for that matter) that combined all of these three characteristics/capabilities:

- Nice formatting providing "eye candy" to humans.

- Inline XBRL providing human-readable details within that nicely formated document, plus fundamental machine-readability.

- Human readable details; current Inline XBRL viewers are OK, but there is a lot of room for improvement. For example, seeing that all the mathematical computarions ticked and tied. A standard view of reported facts.

This video that explains how to turn gaseous "facts" into liquid "fact tables" and ultimately into human-readable renderings.

How is your digital maturity? Do you understand that this is more about people and organizational dynamics as contrast to simply technology? How well do you understand artificial intelligence? By one account, 81% of business leaders don't understand AI. Do you have the "technology skills" people like the AICPA say you need? Personally, I don't believe that you need technology skills; what you need is Computer Empathy.

Did I miss something? Let me know. Get the big picture here.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Digital Reporting Convention

Apparently there is a Digital Reporting Convention in Vienna, Austria! Seems to be put on by Nexxar. Seems they have a technique called push reporting. They are talking about the changing role of the corporate report:

Changed role of corporate reports

The role of the corporate report as an information medium has changed fundamentally in the last two decades. For a long time, the corporate report was not only regarded as the central source of information, but also as the only source of information regarding the economic development of a company. In the digital age, the report has lost this monopoly position. On the Internet, it competes with numerous other – often algorithm-based – information providers. Already on the day of publication, central contents such as the Balance Sheet or Statement of Income of a listed company are available on numerous large and small online portalson the web (e.g. Google Finance).

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print