BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from October 1, 2015 - October 31, 2015

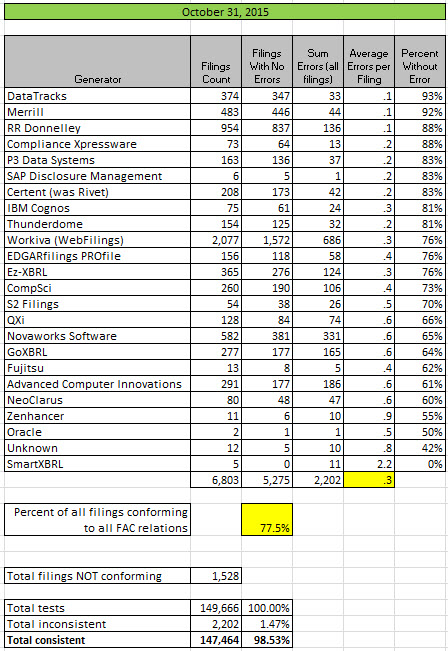

Public Company Quality Continues to Improve, Nine Generators above 80%

The quality of XBRL-based public company financial filings to the SEC again continues to improve. Now there are nine software vendors and filing agents which are 80% or more consistent with the approximately 22 fundamental accounting concept relations. Here is the information by software vendor/filing agent:

(Click image for larger view)

(Click image for larger view)

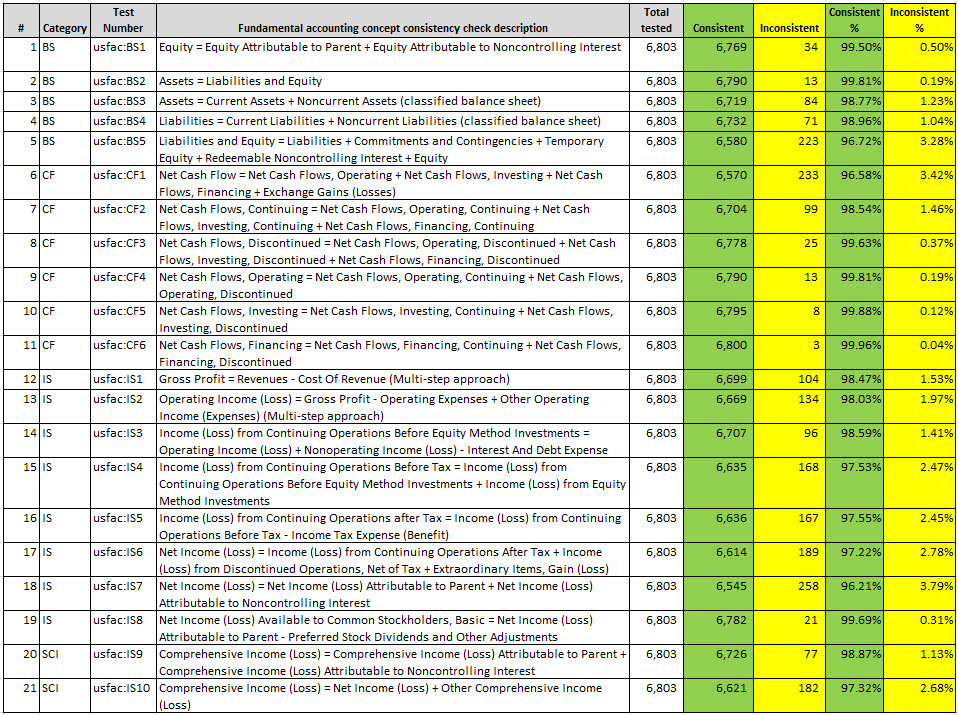

And here is the same information broken out by relationship:

(Click image for larger view)

(Click image for larger view)

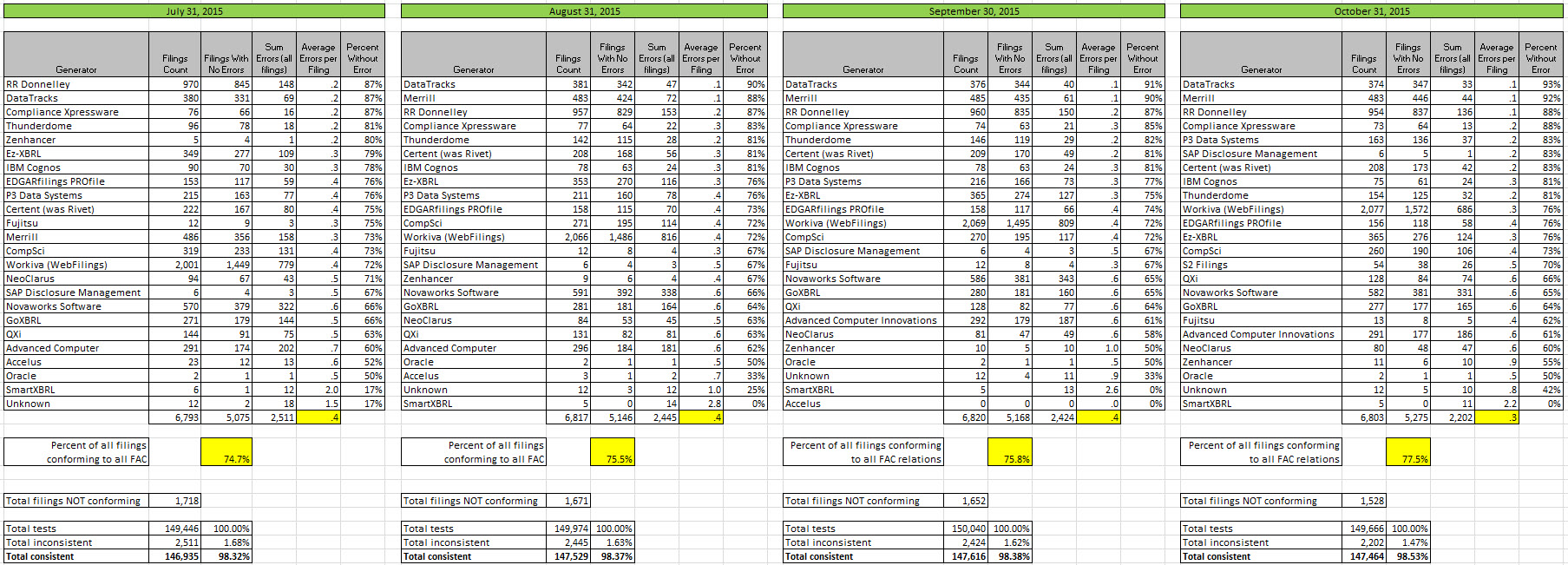

Here is comparison information for July, August, September, and October 2015:

(Click image for larger view)

(Click image for larger view)

Great work to the software vendors, filing agents, and public companies who are blazing the digital financial reporting trail!

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Moving Web Services to Azure

I am making the switch to Microsoft Azure. Here are some prototypes:

Charlie

in Demonstrations of Using XBRL

|

Post a Comment

| Email

| Print

Need for Digital Alternative to General Purpose Financial Statement

“The difficulty lies not so much in developing new ideas as in escaping from old ones.” (John Maynard Keynes)

The general purpose financial statement (or financial report) has existed for over two millennium. Formats for general purpose financial statements have included clay (see below), paper, word processor documents such as Microsoft Word, PDF, and HTML. The common thread that all these reports have is that a machine cannot read these reports because the reports are unstructured.

The institution of accountancy needs to create a digital, or structured, version of the general purpose financial statement which is machine-readable.

Annual balance sheet of a State-owned farm, drawned up by the scribe responsible for artisans: detailed account of materials and workdays for a basketry workshop. Clay, ca. 2040 BC.; Wikipedia, Retrieved October 28, 2015.

Annual balance sheet of a State-owned farm, drawned up by the scribe responsible for artisans: detailed account of materials and workdays for a basketry workshop. Clay, ca. 2040 BC.; Wikipedia, Retrieved October 28, 2015.

Financial Statement, Wikipedia, Retrieved October 28, 2015

Financial Statement, Wikipedia, Retrieved October 28, 2015

The digital general purpose financial report is an improvement that helps move the institution of accountancy forward, providing an improvement to that institution. Given today's increasing volume of financial information, complexity of financial information, and importance of financial information; it makes perfect sense to provide such a digital alternative or option.

Financial analysis has been digital for many years; first via the electronic spreadsheet and now with a multitude of options.

With digital books, maps, photos, films, music, blueprints, etc.; what about the digital financial statement does not make sense? Perhaps I am stating the obvious.

Reposted on LinkedIn (Please consider going to LinkedIn and Like this post)

This is my vision of how a digital financial report would work.

Imagine being being able to pivot a financial report:

https://upload.wikimedia.org/wikipedia/commons/d/d7/8-cell.gif

https://upload.wikimedia.org/wikipedia/commons/d/d7/8-cell.gif

Charlie

in Digital Financial Reporting

|

Post a Comment

|

1 Reference

| Email

| Print

1 Reference

| Email

| Print

Several Interesting Prototypes

I created several interesting prototypes. Check them out. If you have any feedback or ideas, please send me an email.

- Reporting styles for statement: Shows different reporting styles, lets you compare and contrast different reporting styles.

- Fundamental accounting concept relations 'graphs': (When I say graph, I don't mean like a 'chart'. What I mean how the term graph is used in mathematics.) This lets you see the graph of rules for each reporting style.

- Reporting styles for statements (alternative 2): This is similar to the first bullet above, but it is a different approach to showing the information.

- Each fundamental accounting concept relation: Lets you view each of the fundamental accounting concept relations. (I think I will redo this similar to the third bullet point, were you can select from a list.

- Improved disclosure viewer: Somewhat of a library of disclosures.

- Improved "report frame" or "reporting style" viewer: A "report frame" is a term I came up with to enable the differentiation in how economic entities report. You can think of a report fame as a "pallet" or "style" of reporting. Of the many things in a financial report, each can have alternative approaches to reporting those things.

- Improved fundamental accounting concept relations viewer: An improved approach to viewing the fundamental accounting concept relations.

Again, any feedback would be great. Always looking for ways to improve things.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

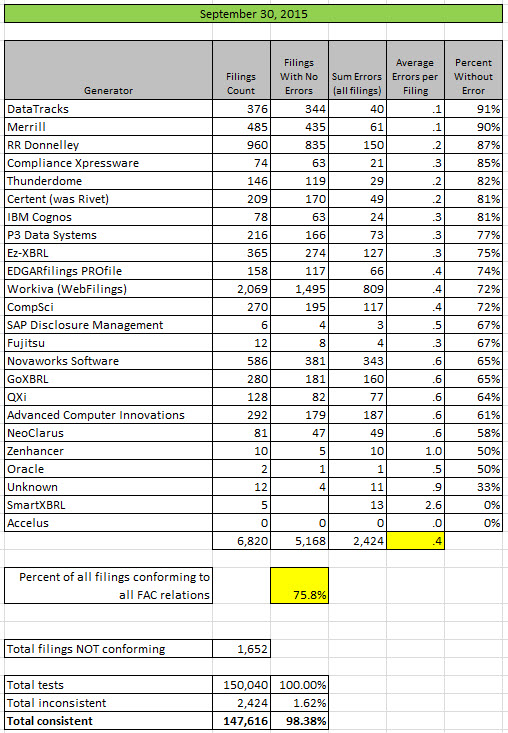

Public Company Quality Continues to Improve, Two Generators at 90%

The improvement is slow and steady which might not be sexy, but the quality of public company XBRL-based digital financial reports continues to improve.

A second software vendor/filing agent, Merrill, joins DataTracks with over 90% of all of the XBRL-based public company digital financial reports which they create being consistent with all 22 of the basic, common sense fundamental accounting concept relations rules.

(Click image for larger view)

(Click image for larger view)

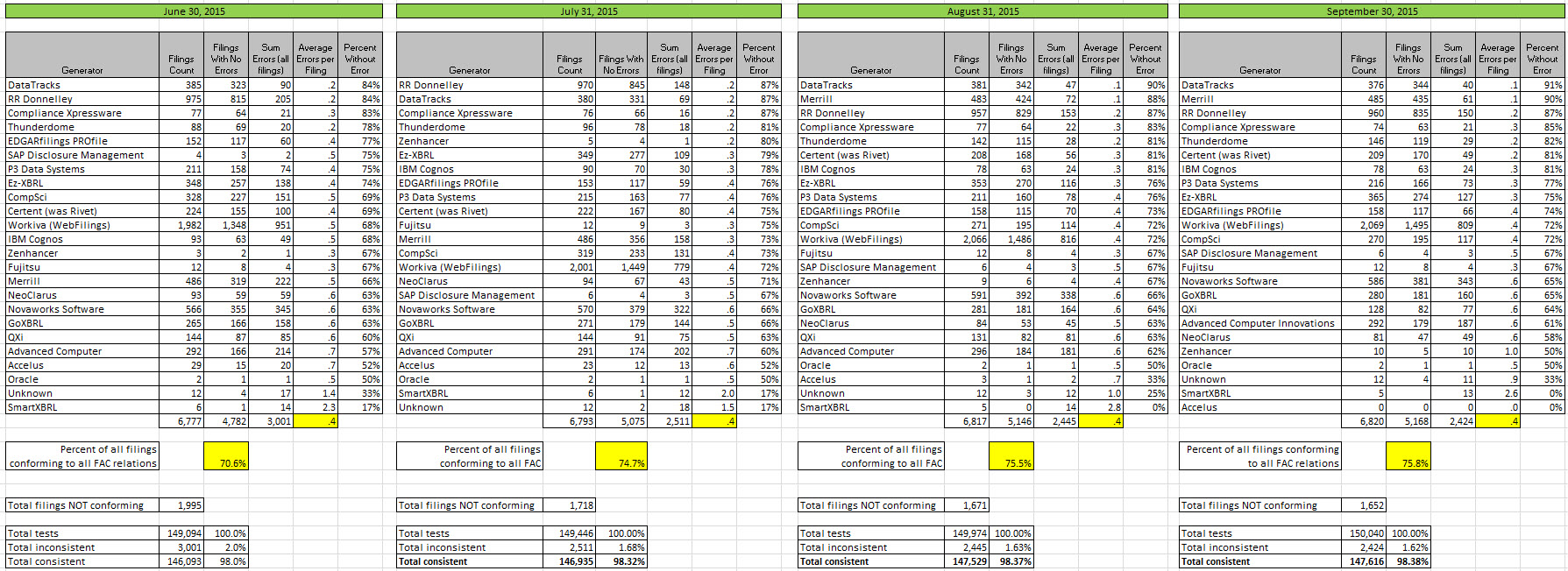

As can be seen in the four month comparison and comparison across individual consistency check:

- Between June 2015 and September 2015, the total number of public company XBRL-based digital financial reports consistent with all 22 of the basic, common sense fundamental accounting concept relations went from 70.6% to 75.8%.

- For the same period, the total number of inconsistencies with those rules dropped from 3,001 to 2,424.

- If you consider each individual consistency check of which there are 150,040; 98.38% of all fundamental accounting concept relations are shown to be consistent with expectation.

- The least consistent rule is 96.3% which means that at least that percentage of the total 6,820 are consistent with the rule. That means only 3.7% are inconsistent with that rule for some reason.

Comparison across four months:

(Click image for larger view"

(Click image for larger view"

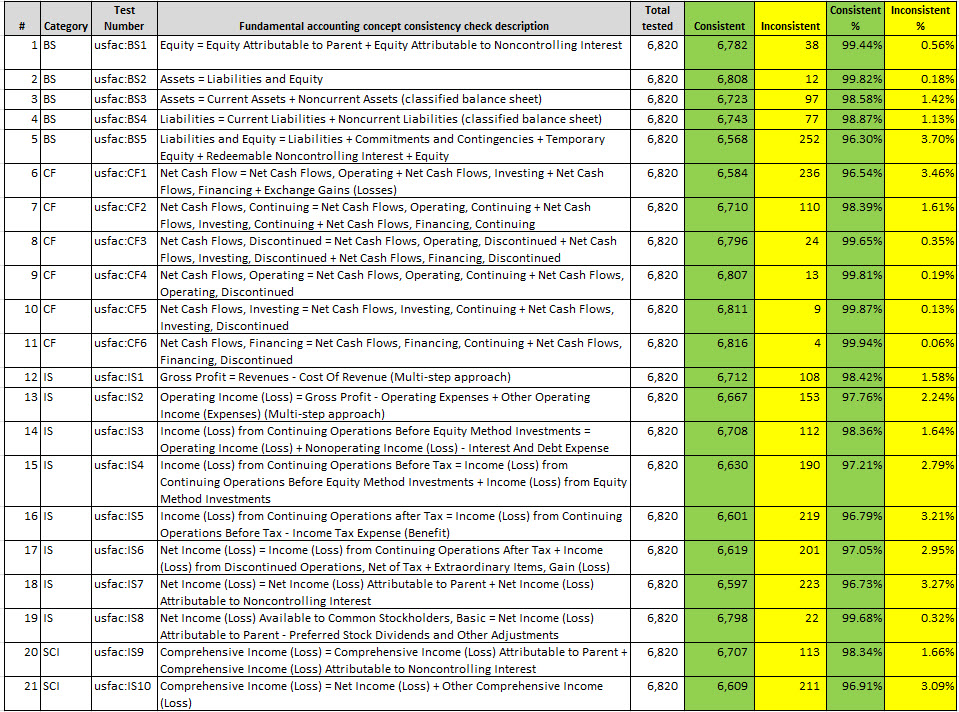

Information per fundamental accounting concept consistency check:

(Click image for larger view)

(Click image for larger view)

I don't know if the XBRL US Data Quality Committee is considering adding these basic, common sense fundamental accounting concept relations to their battery of consistency checks. I would encourage you to ask members of the committee why they would not add these basic common sense rules.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print