BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from October 1, 2018 - October 31, 2018

NASBP: Surety Data Standards: Is Manual Data Entry Dead?

In an article, Surety Data Standards: Is Manual Data Entry Dead?, NASBP says "We’re hammering the final nail in the coffin of manual data entry... more to come."

NASBP says, "The gruesome (and grueling) days of painful re-keying of data may be coming to an end. Could data standards be the magic bullet?"

The article says:

"In 2017, The Hartford successfully brought standardized WIP reports into their internal financial management system, reducing WIP report processing from 20 minutes to 3 seconds. And earlier this year, two more software providers enabled their applications to prepare XBRL-formatted WIPs. Crowe LLP introduced a unique application to automatically build XBRL-formatted WIP reports along with other financials."

XBRLogic says it can automatically generate a normalized financial report in 2 minutes.

Are you toiling in the salt mines of data entry? Not me. I am brainstorming how to build the modern finance platform. There are already commercially available tools for accounting process automation, continuous accounting, smart close, and finance transformation. Managing the workflow of those tasks can also be managed with things like close process management. Personally, I have better things to do with my time that toil in salt mines.

####################

Here is an example surety report.

Here is a press release.

Charlie

in General Information

|

Charlie

in General Information

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Brainstorming How to Build the Modern Finance Platform

Every now and then I get to a point where I become so overwhelmed with information that I know is important but I have not been able to organize, summarize, and otherwise synthesize it enough to make it as coherent as I want it to be. I am at that point.

The last time I was at that point was before I created the document Computer Empathy. That document is by no means the perfect organization of information but it is a very good inventory of the moving pieces of a puzzle that I was trying to put together. Besides, it lead me to the exact same conclusion that others independently came up with when the created the idea of "computational thinking" that basically everyone needs to understand. That bottom line has two points: (1) if you want to get a computer to perform useful work for you reliably you need to understand how computers function; (2) computers work using the rules of logic.

This time I am not sure what the point is yet. I have confidence that it will appear, but I have not arrived at that destination yet. But, here are the current puzzle pieces that are scattered around that I am trying to arrange: (currently in no particular order)

- Distributed Ledgers+Smart Contracts+XBRL: There is a connection between distributed ledgers, smart contracts, the capabilities of XBRL, triple-entry accounting, and the modern finance platform.

- Fact ledgers: Accountants understand HOW to do double-entry accounting; but what I am seeing is that many accountants, including myself, don't understand WHY they use double-entry accounting. Maybe it was never explained to them. Maybe they forgot. For me, I don't know if it slipped my mind. The fact ledger leverages the ideas of the ledger and the journal to create machine-readable versions of those to important tools of accounting.

- Leveraging the Theoretical and Mathematical Underpinnings of a Financial Report: This document explains the theoretical and mathematical underpinnings of double-entry accounting and financial reports. A financial report is a graph of facts. That graph of facts includes transactions, events, circumstances, and other phenomenon of an economic entity that fits into two categories: things that went through the general ledger (double-entry) and things that did NOT go through the general ledger (single-entry).

- Leveraging XBRL's Extensibility Effectively: XBRL builds on top of XML. Native XML is not extensible; XBRL can be safely extensible. If you choose to leverage XBRL's extensibility you have to manage that extensibility appropriately. A complete set of clear rules is mandatory for information conveyed within an XBRL instance to be understood as intended if extensibility is used.

- Understanding and Appreciating the Capability to Recognize and Identify Blocks: This document explains a technique that I came up with, the Block, that allows software to interact with XBRL-based information effectively.

- Chain of Capabilities Necessary to Automate Accounting Processes: As the notion of irreducible complexity points out, there is a chain of capabilities that must be mastered in order to effectively and reliably automate accounting processes. I provide a precise list of the capabilities that are necessary to master, but I am not 100% certain that the list is sufficient. The first software vendor that masters this chain of capabilities, understands the Law of Conservation of Complexity, and creates functional software that is truly usable by professional accountants will win big.

- General Ledger Trial Balance to External Financial Report: This document summarizes a basic example of putting all the pieces together to go from a general ledger to an external financial report for all the transactions that flow through the general journal to the general ledger. All those pieces fit together. What this example does not show is the transactions, events, circumstances, and other phenomenon that does not flow through the general journal and general ledger.

The vision of the modern finance platform is articulated well. Blackline articulates their vision "...to modernize the finance and accounting function to empower greater productivity and detect accounting errors...". Jun Dai and Miklos Vasarhelyi of Rutgers University provide a vision of what auditing will be like in their papers Imagineering Audit 4.0 and Toward Blockchain-Based Accounting and Assurance. Auditchain has a vision and is building what they call a continuous audit and reporting protocol ecosystem. Pacio is also building an ecosystem that includes what they call a standardized semantic information model (SSIM). GovernanceChain is building "the triple-entry accounting network".

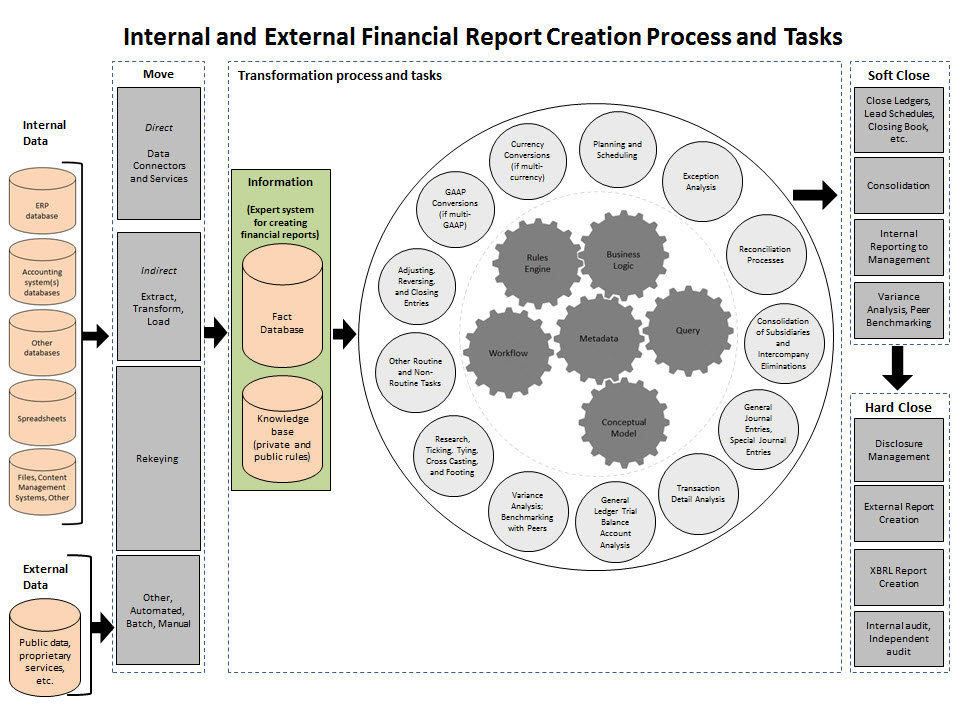

There are three graphics that I would like to combined into one composite graphic. I have broken down the processes and tasks involved in creating an internal and external financial report as such (my graphic was inspired by this graphic of Blackline):

(click image for larger view)

(click image for larger view)

Jun Dai and Miklos Vasarhelyi of Rutgers University have a graphic that describes their notion of a "mirror world" and how mirror worlds relate to the real world:

(Click image for larger view)

(Click image for larger view)

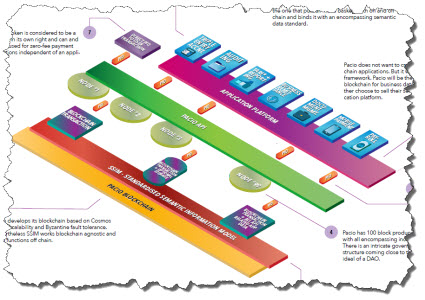

Paico has a pretty good infographic which describes their specific system:

(Click image for larger view)

(Click image for larger view)

I have some other graphics from an accounting information systems text book that I have which are pretty good. Plus, I have some other graphics. What I want to create is one graphic that pulls all of these ideas together.

All my ideas are instantiated within a solution which is contained in this ZIP file which you can download. There are two software applications which will execute all those rules which results in these two packages of information being generated:

- Evidence Package: Allows user to view the pieces of a report and validation information

- Reporting Checklist: Tests the pieces of the report to make sure they conform to rules.

What I would really like is for those two sets to be combined into ONE set of information. Secondly, one downside of the above information is that it is static rather than dynamic. The second software application provides a more dynamic interface, you can download and try that software here.

The documents show two other examples. The first example is simpler and easier to follow. The second example is an actual XBRL-based submission to the SEC which is extremely robust, but incomplete in some areas.

And so my task: How do I simplify all this and explain it?

Stay tuned, I am sure I will figure it out.

Charlie

in Digital Financial Reporting

|

Post a Comment

|

1 Reference

| Email

| Print

1 Reference

| Email

| Print

Incremental, Disruptive, and Foundational Technologies

The Innovators Dilemma points out the difference between an sustaining or incremental innovation and a disruptive innovation.

- Sustaining technologies which foster improved product performance. (improves a current business model)

- Disruptive technologies which result in worse product performance in the short term, but then over the long term they bring to a market a very different value proposition than had been available previously. (attacks current business models with lower cost business models)

This article references a Harvard Business Review article which points out the difference between a disruptive technology and a foundational technology.

- Foundational technologies create new foundations for economic and social purposes.

Foundational technologies have two dimensions that need to be considered: novelty and complexity.

The more novel the technology is, the more effort needed to ensure users understand the problems the new technology solves. The higher the number of parties and the diversity of parties that have to work together to work together to produce a new solution, the more complexity is involved in making that product available.

The Harvard Business Review article points out how foundational technologies take hold; see the section How Foundational Technologies Take Hold in the article. They point out a matrix that compares the dimensions of novelty and complexty, the four intersections in the matrix are:

- Low Novelty, Low Complexity: Single Use

- High Novelty, Low Complexity: Localization

- Low Novelty, High Complexity: Substitution

- High Novelty, High Complexity: Transformation

Charlie

in General Information

|

Post a Comment

| Email

| Print

Distributed Ledgers + Smart Contracts + XBRL

I put together a document which I called Distributed Ledgers + Smart Contracts + XBRL that summarizes information I collected related to using XBRL within distributed ledgers.

Basically, XBRL offers an entire global standard ecosystem for working within a digital distributed ledger to represent information and smart contracts to execute processes and workflow. Within XBRL one can represent complex information such as an entire financial report. Perhaps not every implementation of a smart contract in a distributed ledger needs all of this robust functionality; but if you do need it, the global standard XBRL can provide it.

########################################

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Understanding Digital Financial Reporting using Pesseract

Pesseract (free download) is a software application created by a software engineer and myself. These screenshots help you see what Pesseract can do. We don't consider it a commercial product yet because it does not have the compete set of features completed. However, Pesseract does have plenty of features and can be effectively used to explore XBRL-based reports and understand where XBRL-based digital financial reporting is headed.

Try Pesseract using these XBRL instances and XBRL taxonomies. Why? Because they are good examples of XBRL-based financial reports. You can also try any US GAAP or IFRS XBRL-based report submitted to the SEC. But I suggest you use the better reports. Microsoft, Apple, Google. Here are US GAAP reports and IFRS Reports.

We are not "paving the goat path" like other software developers; our goal is to increase our know-how. We figured out a different path.

Pesseract is a working proof of concept where we are figuring out how to create an expert system for creating high-quality financial reports. We believe that we can make Pesseract create higher quality reports than the financial reports that are being created today. Pesseract will be a disruptive innovation that changes how financial reports will be created in the future. We buy into the notion of the modern finance platform. We buy into the notion of mirror worlds. We buy into the notion of triple-entry accounting and distributed ledgers. We believe artificial intelligence can be leveraged to automate many accounting tasks. We buy into the notion that Lean Six Sigma can be leveraged to improve process quality.

Accounting, reporting, auditing, and analysis in a digital environment is not about making incremental changes to outdated 20th Century paper and document oriented workflow and processes of creating financial reports.

We are making Pesseractavailable for professional accountants to experiment with. To download Pesseract, go to the Download/Get Started tab here and follow the instructions. We are not making the creation features available at this point, we are tuning those features. But, there are many, many other things you can do with Pesseract. Below is a set of documents that help you learn about Pesseract and XBRL-based digital financial reporting:

- Getting Started with Pesseract: helps you learn some of the basics.

- Validating an IFRS based Report: helps you understand that Pesseract works with IFRS reports as well as US GAAP based reports.

- Report Model Structure and Fundamental Accounting Concept Relations Validation: walks you through the process of validating a reports model structure and fundamental accounting concept relations.

- Multiple Languages: walks you through the use of labels in multiple languages.

- Appending Instances: shows you basic example of how to append information from one XBRL instance to another XBRL instance.

- Dynamic Rules: shows you have business rules can be dynamically used with an XBRL instance. (Here is the example with all the rules available locally, this is really interesting.)

- Normalized Comparison: walks you through the process of comparing information across period for an entity or across entities for a period.

- Appending Linkbases: shows you basic example of how to append information to an existing report using XBRL linkbases.

- Drill Down: shows you how you can leverage the structured nature of XBRL to drill down from higher granularity information to lower levels of granularity; or move from lower granularity to higher granularity.

- Filtering and Searching: shows you how you can leverage the structured nature of XBRL to filter and search information within a financial report.

- Exploring model structure and fact tables: helps you better understand structured reports by explaining basics of the model structure and fact tables.

- Networks, Components, and Blocks: helps you understand the differences between networks, components, and blocks.

- Blocks (Advanced): helps you understand the connection between blocks and reporting checklist and disclosure mechanics validation.

- Hundreds of Example Reports: helps you understand where to find hundreds of XBRL-based reports which you can help you consolidate your knowledge.

- API, Batch Processing, Plugins: helps you recognize that Pesseract is not just a software application; it has an API, you can create batch processes at the command line, and you can create plugins.

- Profiles: helps you understand what a profile is, how profiles are helpful.

- US GAAP Reports: This is 5,734 XBRL-based reports created using US GAAP that you can fiddle with.

- IFRS Reports: This is 406 XBRL-based reports created using IFRS that you can fiddle with.

- Financial Report Creation Wizard: Wizard which walks you through the process of creating a financial report. (Not in the current release)

The following are demonstrations of Pesseract:

Stay tuned as additional examples will be provided as they are created and we will provide newer versions of the Pesseract application as as appropriate. An investment of your time today could make you a digital financial reporting master craftsmen of tomorrow!

#########################

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

1 Reference

| Email

| Print