BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from October 1, 2018 - October 31, 2018

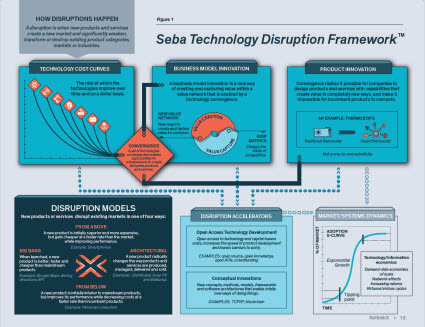

Seba Technology Disruption Framework

A BBC News article, Why you have (probably) already bought your last car, reports that RethinkX reckons that within 10 years of self-driving cars getting regulatory approval 95% of passenger miles will be in self-driving electric robo-taxis. The article goes on to say that these regulatory approvals could be in place by 2021 in the United Kingdom. Some say this could happen by 2030.

How does disruption work? The Innovators Dilemma explains the difference between sustaining (or incremental innovation) and disruptive innovation. Sustaining innovation meets a customer's current needs. Disruptive innovation meets a customer's future needs.

The Seba Technology Disruption Framework, which was created by Tony Seba, explains how disruption works:

(Click image to go to presentation which explains Seba Technology Disruption Framework)

(Click image to go to presentation which explains Seba Technology Disruption Framework)

Here is the definition of disruption Tony Seba uses:

A disruption is when new products and services create a new market and significantly weaken, transform or destroy existing product categories, markets or industries.

This 50 minute video explainshow AT&T missed the mobile phone market because of a 10x error in estimating the market provided by "an expert". Here is a list of the seven worst technology predictions of all times.

What does this mean for the modern finance platform? What does this mean when accounting, reporting, auditing, and analysis moves to a truly digital environment? Let me know what you think.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

1 Reference

|

1 Reference

|  Email

|

Email

|  Print

Print

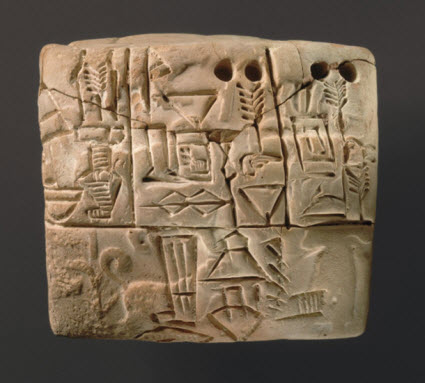

Understanding the Importance of Triple-Entry Accounting

Between 5,000 and 10,000 years ago farmers in Mesopotamia, where agriculture was born, used physical object to count crops and animals . The distinction between types of crops or animals was made by using different types and shapes of objects.

Then, in about 3200 BC, around 5,000 years ago, the first spreadsheet was invented. These farmers began documenting information using clay tablets in the earliest form of human writing ever discovered called Cuneiform. They partitioned their clay tablet into rows, columns, and cells. These farmers used single-entry accounting.

Source: Metropolitan Museum

Source: Metropolitan Museum

In 1211 AD a bank in Florence, Italy was the first documented use of double-entry accounting. Between 1299 AD and 1300 AD double-entry accounting came of age. In 1494 AD during the Renaissance, Venetian mathematician and Franciscan friar Luca Pacioli published a book, Summa de arithmetica, geometria. Proportioni et proportionalita (Sum of Arithmetic, Geometry, Proportion and Proportionality). That book documented the double-entry approach bookkeeping and recommended that others use this approach. The double-entry approach allowed for better error detection and the ability to differentiate unintended errors from fraud. Accountants adopted that new approach.

Most recently there are discussions about immutable mutual digital distributed ledgers using cryptographic technologies. One technology that can be used to implement a digital distributed ledger is blockchain. People are calling this "triple-entry accounting". Some say that triple-entry is the most important invention in 500 years. Basically what triple-entry does is create a link between the two double-entry systems documenting that the transactions in the two systems go together.

There is a little bit of a dispute around the true meaning of "triple-entry". Yuji Ijiri was first credited with using the term but the blockchain folks seem to have perhaps redefined the terma bit. I am using the term "triple-entry" as the blockchain people and Ian Grigg tend to use the term.

Here is the bottom line:

- A single-entry is not much more than a glorified list.

- Double-entry is in essence posting a transaction to two different single-entry ledgers with different parties responsible for each ledger. When you use a double-entry ledger what the transaction represents has to be explained by reasoning, the two transactions logically go together. Removing or changing part of the transaction will make the transaction illogical. Double-entry allows for the detection of errors and the differentiation of an unintentional error from fraud.

- Triple-entry further builds on double-entry in that triple-entry links a transaction in two double-entry ledgers and the link is publicly available for all to see the transaction. You are still able to explain the reasoning behind the entry but additionally the transaction is visable for all to see which makes it very tough to lie since others are watching. It would be illogical for the transaction to not be reflected the same in both ledgers.

With the volume of transactions growing and complexity increasing; triple-entry accounting intuitively seems like a potentially valuable tool. Perhaps those experimenting with triple-entry accounting might come up with something useful.

################################

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Introducing the Fact Ledger

Before writing was invented, between about 5,000 and 10,000 years ago farmers in Mesopotamia used physical object to count crops and animals. In about 3200 BC the first spreadsheet was invented when these farmers began documenting information using clay tablets in Cuneiform; partitioned their clay tablet into rows, columns, and cells. This was single-entry accounting.

In 1211 AD a bank in Florence, Italy was the first documented use of double-entry accounting. Between 1299 AD and 1300 AD double-entry accounting came of age and in 1494 AD during the Renaissance, Venetian mathematician and Franciscan friar Luca Pacioli published a book, Summa de arithmetica, geometria. Proportioni et proportionalita documenting this approach.

Accountants have a special name for the spreadsheets, or tables, that these farmers invented and Italian bankers perfected. Accountants call these ledgers.

A ledger is simply a place where you record information such as transactions.

A fact ledger is a new type of ledger that offers utility and leverage when accounting, reporting, auditing, and analysis is done in a digital environment. Another accountant and I came up with this idea when trying to figure out how to actually implement accounting process automation. The document Introducing the Fact Ledger summarizes our ideas related to this tool.

Fact ledgers can work with single-entry accounting, double-entry accounting, or even triple-entry accounting.

Do you have any ideas that might improve on our vision of the fact ledger? If so, give us a shout.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Reengineering Accounting

There are a lot of blockchain-related companies and other underlying infrastructure providers that are trying to reengineer accounting. Here is a partial list:

- Alastria

- Auditchain

- Axoni

- Balance3

- BBiller

- Blockstack

- ChainThis

- Global Legal Entity Identifier (infrastructure)

- GovernanceChain

- Hyperledger (blockchain infrastructure) (this is a business oriented approach; scalable, secure, industrial strength blockchain technologies for business)

- Ledgerium

- OpenFiling

- Pacio

- PayPie

- Request Network

It will be interesting to see if any succeed. Here are some good videos that explain Bitcoin, Blockchain, and Triple-Entry accounting: Bitcoin is more than money. Blockchain is a new way to record and store transactions of all sorts. This video explains the basics of how bitcoin works. This video explains how triple-entry accounting works. This is a pretty decent video that explains the implications of triple-entry accounting. This is an OK explanation of triple-entry accounting.

This paper created by the UK government is one of the most comprehensive yet approachable resources for understanding distributed ledgers.

Integrating semantics and blockchain.

AICPA: Evolution of Auditing: From the Traditional Approach to the Future Audit

Conclusion

Auditing has made great strides in the past decade, but it has not seemingly kept pace with the real-time economy. Some auditing approaches and techniques that were valuable in the past now appear outdated. Also, the auditing evolution has reached a critical juncture whereby auditors may either lead in promoting and adopting the future audit or continue to adhere to the more traditional paradigm in some manner. Future audit approaches would likely require auditors, regulators, and standards setters to make significant adjustments. Such adjustments might include (1) changes in the timing and frequency of the audit, (2) increased education in technology and analytic methods, (3) adoption of full population examination instead of sampling, (4) re-examination of concepts such as materiality and independence, and (5) mandating the provisioning of the audit data standard. Auditors would need to possess substantial technical and analytical skills that are currently not components of most traditional four year university accounting programs.

SOX introduced the first major change in the mandate of the public company audit. This new prescription focuses on auditor assessment of internal controls, a very important step in the assurance of future systems that will be modular, computerized, and often outsourced. The accounting profession now faces an opportunity to further elevate the audit to a higher level of automation. It is imperative that accountants ultimately lead the way in adoption and implementation of the future audit such that they continue to be the professionals of choice relative to audit engagements of the future.

Feasibility, Desirability, Viability

- Desirability is explored through Customer Segments, Customer Relationships, Channels and Value Proposition.

- Feasibility is explored through Key Resources, Key Activities and Key Partners.

- Viability is explored through Cost Structure and Revenue Streams.

Generally speaking, every major brand collapse you can think of started with the abandonment of their competitive advantage.

- Kodak invented digital cameras, then neglected the technology.

- Department stores thrived on convenience, but their disdain for internet shopping made their services harder to engage with.

- Nokia and Motorola had the phone market sewn up, then sat on their hands while two others took their Innovative title away from them.

Charlie

in Distributed Ledgers

|

Post a Comment

| Email

| Print

This Canadian Genius Created Modern AI

The YouTube.com video This Canadian Genius Created Modern AI tells the story of Geoff Hinton, the Canadian that created moden artificial intelligence. Almost everyone thought he was crazy...right up until the moment he revolutionized the field of AI.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print