BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from November 3, 2019 - November 9, 2019

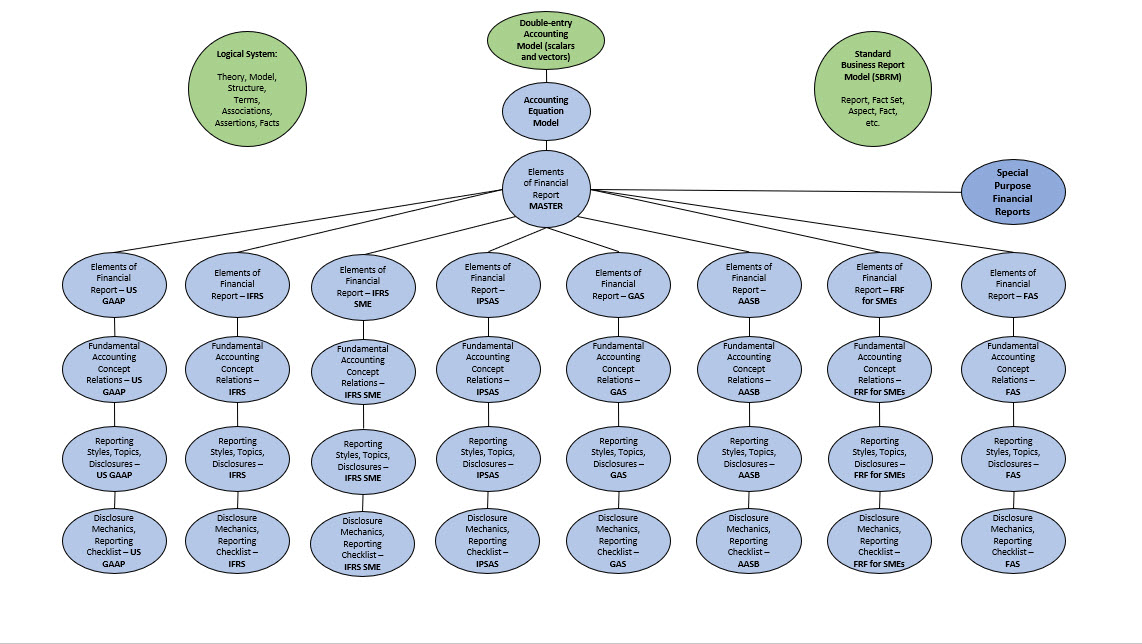

Financial Report Genome Project

I have undertaken something that, for lack of a better term, I am calling the Financial Report Genome Project. This graphic helps you see what that project achieves:

Basically, this is pure college freshman level math. All financial reporting schemes "fit" into the accounting equation. Each financial reporting scheme conceptual model definition of the elements of financial statements fits into the same model. Yes, it is true that different elements are used by different reporting schemes. Yes, it is true that variability exists. But all these financial reporting schemes fit into the exact same model. I know this becuase (a) two software vendors already support this and (b) I can provide the mathematical and logical proof.

What this project does is leverage an easy to grasp explanation of a logical system, a framework for representing a financial report using that logical system, the accounting equation, and the fact that financial reporting schemes elements of a finacial report can be mapped to the accounting equation; to implement XBRL-based digital financial reporting elegantly.

The unjustifiable and usually unconscious differences between implementations of XBRL-based reporting by regulators has profound implications for accountants. These differences tend to make using XBRL harder than it needs to be, tend to make software cost more to buy, tend to reduce functionality offered by the software to the users of the software, and tend to be completely unnecessary.

If you have read Artificial Intelligence and Knowledge Engineering in a Nutshell; on page 6 I highlight the Major obstacles to harnessing the power of computers. The key word: idiosyncrasies.

Folks, don't let the tendency for regulators to do things in their own little silos screw up financial reporting for the next 100 years! Accounting, reporting, auditing, and analysis in our now digital environment can be elegant and easy to use if people (a) understand how all this works and (b) consciously think about what they are doing.

Me, I don't like toiling in the inefficient salt mines using barbaric, outdated approaches.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

The Mathematics of Double Entry Bookkeeping

Mathematics Magazine published an article written by David Ellerman, The Mathematics of Double Entry Bookkeeping, where Ellerman points out that double entry accounting is based on well-known mathematics construction from undergraduate algebra. But Ellerman laments, "Mathematics and accounting truly seem to live in disjoint universes with no trespassing between them."

Well, I speculate that XBRL-based accounting, reporting, auditing, and analysis will join the universes of accounting and at least computer science if not mathematics. Digital distributed ledgers will likely have an impact also. Some people seem to think double entry accounting is obsolete. They probably don't understand the purpose of double entry accounting.

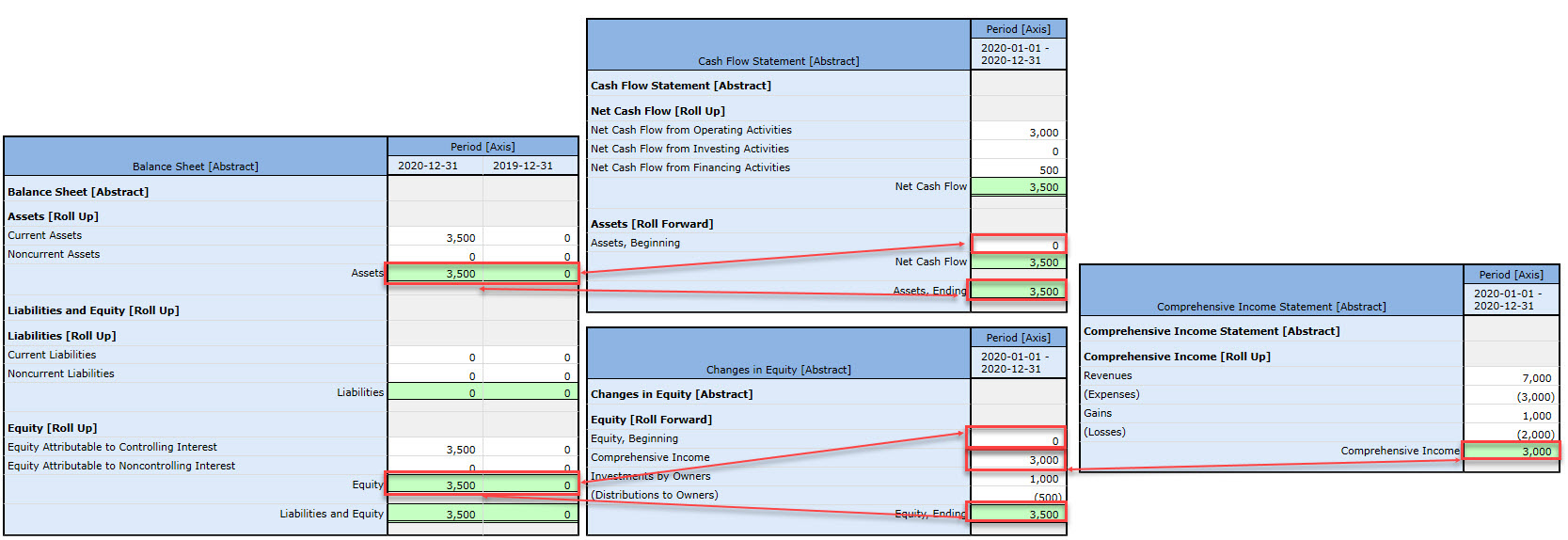

When you understand the scalers and vectors and know every financial reporting scheme uses the notion of articulation to intensionally and explicitly create the interrelationships between the four primary financial statements; you will recognize the leverage this offers.

When you understand that every real account on the trial balance has a roll forward, you see even more leverage.

When software engineers construct the right software, they can help accountants do accounting, reporting, auditing, and analysis in new and exciting ways. No more toiling in the salt mines!

##########################

Triple entry accounting (video)

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print