BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from March 29, 2020 - April 4, 2020

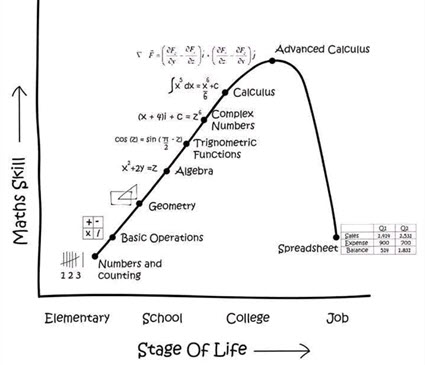

Understanding Why Many Business Professionals Don't Understand AI

Pascal Bornet posted an insightful graphic that explains why most business professionals don't understand the changes that will be caused by artificial intelligence:

I taught an accounting information systems class at the University of Washington and there was not one student in the class that knew how to program, even Excel VBA. It amazes me how many accounting students and business professionals that think they understand Excel but cannot even write simple VBA code. Also, while Excel is an excellent tool, Microsoft Access is an even better tool for many tasks than Excel. What really blows my mind is that you can have an entire team of accountants and not one person on that team can write VBA code! If you know VBA and SQL you have an an excellent skill set. Throw onto that XPath and XML and you can do even more. Master XBRL to that and you can do even more.

Personally, I think my personal skill set is about three quarters of the way up that right side line toward the top. I wish I could get my head around graphs better. I don't think I can get my head around stuff good enough to be able to program complex stuff myself. But, I understand enough to be able to talk to software engineers effectively.

I would really encourage business professionals to read and understand the information in Artificial Intelligence and Knowledge Engineering in a Nutshell. AI is real. Get ready. Heck, even better...help create the future of accounting, reporting, auditing, and analysis. Why? As is said, "The best way to predict the future is to create it."

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Try Pesseract, Get a Glimpse of the Future of Financial Reporting

Pesseract is a working proof of concept that was created by Hamed Mousavi, a software engineer, and myself. Hamed and some of his colleagues won the prize of 9th XBRL Global Academic Competition 2008-09, which was held in Bryant University, USA.

Pesseract is not a commercial product yet, but it is very robust software application that works incredibly well for a proof of concept. It can help you understand what you should be asking other software companies for in terms of features and functionality. Here are several ways to understand Pesseract:

- Screen shots: About 30 screen shots that help you see the features.

- Videos: Several video play lists.

- Download: Download the application and try it out for yourself.

- Pesseract Testing: Download these files and try Pesseract locally. (Use this documentation to understand the steps you should perform. Helps you understand the method below.)

- Demonstration scripts: About 20 demonstration scripts that you can read, or walk through yourself (if you download the software.

- Method: Good practices/best practices based method for creating a process control mechanism that consistently yields high-quality XBRL-based financial reports where the model can be “reshaped” or “altered” by report creators explained as briefly as is possible. (Supported by Pesseract).

- Mastering XBRL-based Digital Financial Reporting: Try any of the 12 test cases that I have created to exercise XBRL-based digital financial reporting. Pesseract was used to test and develop a lot of these ideas.

If you download the software and want a license, email me and I will get you a license and send you instructions how to install the license.

Set the bar high! Don't settle for substandard software. Push software vendors in the right direction by being an informed buyer.

Want to try creating XBRL-based financial reports? Try Luca.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

EngineB

EngineB says that they are about bringing the "digital revolution to professional services". EngineB calls for a common data model. There are three videos on their home page that explain what they are up to. You can follow them on LinkedIn here.

This 30 minute video helps you better understand what EngineB is up to. Seems like Microsoft is behind what EngineB is doing. In the video, the CEO of EngineB says that "every accounting firm that you have ever heard of is involved". He says that 69% of an audit can be automated and that we can move to "continuous audit".

EngineB is not trying to change what companies do internally. Their focus is when you have to interact with an external party you can use a common format making information exchange more effective and efficient.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Software Companies Prototype

This blog post provides information related to a prototype used to understand reporting styles and disclosure mechanics rules.

Reporting Styles (US GAAP)

The following software/technology related companies were selected. For each, an Excel spreadsheet is provides which can be used to reliably Extract information for each of their XBRL-based reports submitted to the SEC. Embeded within the spreads are the rules for the reporting style. The Reporting Style link provides that same information represented using XBRL. Those XBRL-based rules have been used by three different software vendors to extract information from XBRL-based reports submitted to the SEC. This ZIP archive contains an Excel spreadsheet with all the XBRL reports submitted to the SEC and each of the three Extract files.

- Microsoft: Extract | Reporting style | COMID-BSC-CF1-ISM-IEMIB-OILY-SPEC6

- Apple: Extract | Reporting style | COMID-BSC-CF1-ISM-IEMIB-OILY-SPEC6

- Amazon: Extract | Reporting style | COMID-BSC-CF1-ISS-IEMIT-OILY-SPEC2

- Facebook: Extract | Reporting style | COMID-BSC-CF1-ISS-IEMIB-OILY-SPEC2

- Alphabet/Google: Extract | Reporting style | COMID-BSC-CF1-ISS-IEMIB-OILY-SPEC2

- SalesForce: Extract | Reporting style | COMID-BSC-CF1-ISM-IEMIB-OILY-SPEC6

The six examples use three reporting styles. Here is a list of all the US GAAP reporting styles. Note the machine-readable RSS file with a link to each of the schemas for individual reporting styles.

The VBA code in the Excel spreadsheet can be used to reverse-engineer the process of extracting information. The XBRL based rules are better because they are not hard coded into the application like I did with the Excel (which is because I have limited programming skills).

This is an OLDER VERSION OF THE REPORTING STYLES!!! But, it can help you understand the notion of reporting styles.

An obvious question is, "How do I know the reporting style code to use for a specific company?" There are two ways. (1) You can use this web service which is pretty reliable; (2) You can probe the report and figure out the reporting style based on the terms/associations of the balance sheet, income statement, cash flow statement. Longer term, approach (2) is best. To get started, approach (1) is easy.

Disclosure Mechanics Rules (US GAAP)

Each disclosure that might appear in a financial report has a "digital signature". That digital signature can be used to identify each individual disclosure and extract information for that disclosure from an XBRL-based report. Here is a list of all the disclosure mechanics rules in a natural language syntax. Here is the same information in machine-readable XBRL.

To properly extract information you first need to identify each "fact set" or "block" of an XBRL-based report. This document helps you understand the notion of a fact set (a.k.a. block). Networks are too large and too arbitrary. Individual facts are too small a set. The fact set or block is just right!

Here is an example of blocks:

US GAAP, Microsoft 2017 10-K: SEC Filing Page | XBRL instance | Evidence Package | Disclosure Mechanics | Blocks | Pacioli

Here is information about each of the other five companies 10-K report for 2018:

US GAAP, Apple 2018 10-K: SEC Filing Page | XBRL Instance | Evidence Package | Disclosure Mechanics | Pacioli

US GAAP, Alphabet 2018 10-K: SEC Filing Page | XBRL Instance | Evidence Package | Disclosure Mechanics | Pacioli

US GAAP, Facebook 2018 10-K: SEC Filing Page | XBRL Instance | Evidence Package | Disclosure Mechanics | Pacioli

US GAAP, Salesforce 2018 10-K: SEC Filing Page | XBRL Instance | Evidence Package | Disclosure Mechanics | Pacioli

US GAAP, Amazon 2018 10-K: SEC Filing Page | XBRL Instance | Evidence Package | Disclosure Mechanics | Pacioli

Example comparison: Earnings per Share disclosure: Microsoft, Apple, Alphabet, Facebook, Salesforce, Amazon.

If XBRL-based reporting is practiced correctly, you can do stuff like this and like this. You can also avoid errors like this.

To learn more, I would encourage you to watch these two video playlist: Understanding the Financial Report Logical System and Mastering XBRL-based Digital Financial Reporting.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Record to Report Plus!

It seems that Luca Pacioli either neglected to include something in the double-entry accounting model or he included it but it did not get used in practice for one reason or another.

Why do I say that? Because when I add just this one piece to a general ledger, it enables a complete and verifiably correct set of primary financial statements to be generated: balance sheet, income statement, changes in equity, and a fully baked, proper cash flow statement.

You can also get a roll forward of each real account (i.e. balance sheet line items). To see what I mean, watch this video which does this using existing software you can get your hands on today:

There were multiple key ideas that contributed to achieving this result. Several years ago, someone summarized this notion that an XBRL-based report could be an algorithm or mathematical model. Someone else had this notion of a financial report is a “tree” (actually a graph) and that the “branches” (subtotals) and “leaves” (line items) where different parts of a report and the branches and leaves naturally “rolled up”. Someone else gave a class in FRx about 25 years ago that I attended and many of the things in the FRx “report writer” are applicable to this process. FRx also had a lesser known product called FRL (I think it was) which was essentially a stand alone general ledger (i.e. not an accounting system) into which GL transactions can be “posted”. Someone else, probably 20 years ago, provided an Excel spreadsheet that demonstrated how to extract information from an XBRL-based document. Everything that I learned about working with XML had it’s roots in that Excel VBA code. Someone else who was a Price Waterhouse (pre Coopers and Lybrand) audit senior taught me a slick way to model a financial report that he used in Lotus 1-2-3.

What does all this mean? It means that Deloitte is right with their vision of the Finance Factory. What I was able to do was cobble together the sort of “machinery” that will be running the finance department of the future. That video and these files explains HOW to implement that “Finance Factory” vision, turning it into reality.

"Bolt on" approaches to implementing XBRL-based reporting are doomed. Record to report will undergo significant automation over the next 10 to 20 years. What I am showing is only the tip of the iceberg. You should have a look at EngineB if you don't believe me.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print