BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from July 19, 2020 - July 25, 2020

GUI Examples

This is a summary of GUI examples:

GUI prototyping tools:

XBRL Taxonomy Development Handbook

XBRL US pulished the XBRL Taxonomy Development Handbook today. Pretty extensive. This is worth having a look at.

The handbook makes this statement with which I agree 100%: (Page 2, section 1.1.4 The End Result)

No matter the industry, specific requirements, or reporting needs, the ultimate goal at the end of the taxonomy development process is to create data that is meaningful to consumers. This is true regardless of what that data is and whether it is consumed in real time or collected in offline analyses. The accuracy, usability, and predictability for the consumer is vitally important, and the end product of development should be robust enough to deliver consistent results on all of these fronts.

The essence of an XBRL taxonomy is to enable a meaningful exchange of information. I tried to describe how to achieve that objective in this document.

While the details of this handbook are good, the handbook neglects to wrap those details into an overarching framework, theory, and principles. But, the details are good and I will incorporate all the useful aspects of this handbook into my Mastering XBRL-based Digital Financial Reporting resource.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

SEC Data Set on Google

The SEC Public Dataset is now avaiable via Google BigQuery.

But, there is a problem. How do you think Google is going to magically be able to overcome issues related to different companies using different reporting styles, companies use different concepts to report the same information, errors in the reporting information that I point out via my quality checks. XBRLogic points out similar errors.

Garbage in, garbage out.

Here is a basic query. Here is an introduction to BigQuery. Here is a video introduction.

Here is other information about Google BigQuery:

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

XASB XBRL-based Report Analysis

This blog post builds on the Microsoft XBRL-based Report Analysis. The Microsoft is a real report from a real company. What I was able to do was verify virtually 100% of that Microsoft report using a method that I created. The problem is that word "vitrually". To prove 100% I need to be sure that I can verify 100%. Because Microsoft had some extensions, I was only able to verify 94.8% of all disclosure mechanics rules.

But for this XASB reference implementation I can verify 100%. Here is that verification:

- Video walking you through the analysis (coming soon)

- XBRL instance

- XBRL taxonomy

- XBRL Cloud Evidence Package

- Pesseract Verification Results

- Fundamental Accounting Concept Relations (included with other mathematical relations)

- Disclosure Mechanics Validation Results, Pesseract

- Reporting Checklist Validation Results, Pesseract

- Disclosure Mechanics Rules (Human readable | Machine readable)

- Reporting Checklist Rules (Human readable | Machine readable)

- Model Structure Rules (Human readable | Machine readable)

- Type-subtype Rules (Human readable | Machine readable)

- Blocks

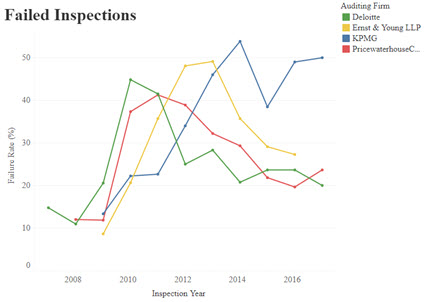

Fortune: Auditing is Broken

In a Fortune article, Wirecard shows auditing is broken. Here’s why—and how to fix it, JEREMY KAHN holds that auditing is broken. He points out that a POGO study found that when the PCAOB inspected Big 4 audits it found:

- Deloitte botched 20%

- PWC botched 23.6%

- EY botched 27.3%

- KPMG botched 50%

Unbelievable.

The article proposes a fix. I would add to that proposal using more automation. Understanding Digital shows how aspects of accounting, reporting, auditing, and analysis can be automated. I know that this works. As this article points out, a philosopher said, “The difference between arrogance and confidence is performance.” I am not being arrogant...I am confident I can deliver. Just need to figure out a way to get people to admit that there is a problem.

#############################

The Boogeyman Behind the Failure to Detect Fraud

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print