BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Proof + Common + Rendering Example Representation

The Proof+Common+Rendering example representation is a new addition to my set of examples which can be used to master XBRL-based financial reporting. What this example does is show you the essence of an XBRL-based digital financial report and then reconcile that essence to a 10-K.

Key information for this example representation includes:

- Files: Every file is available for your further analysis.

- Documentation: This walks you through the example and helps you see what I am trying to get across.

- Database: You can download the Microsoft Access database that I used to create the example. The only thing not included is the code that generates the disclosure mechanics and reporting checklist rules.

- Pixel Perfect Rendering (Inline XBRL): This is an Inline XBRL instance document that was generated from the database above. This version references a web-based taxonomy that supports the XBRL instance.

- Pixel Perfect Rendering (PDF): This is a PDF generated from the information in the XBRL instance using XSL-FO and a FOP to generate the PDF.

There is a wealth of knowledge in this information. This builds on the accounting process automation or record to report example. In essence, if you read through all the examples you can see that you can put transactions into a general journal and if that is done correctly you can generate a pixel perfect XBRL-based financial report and/or a human-readable PDF, HTML, Word, or other such representation.

Essentially, this points out that there is a completely new workflow possibility that can be employed for creating financial reports. Whether one of the outputs is XBRL or not makes no difference. In fact, this is bigger than just reporting; it impacts accounting, reporting, auditing, and analysis.

We live in a world where the questions remain the same; but the answers have changed. This TED Talk video, Why the majority is always wrong, explains. While 97% continue to do more or less of the same things over, and over, and over; 3% try new things.

Consider thinking outside the box. Why settle for normal when you can be exceptional! The digital transformation is about talent, not technology. Learn to leverage your tools effectively.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Ray Dalio: Systemized and Computerized Decision Making

This excerpt from Ray Dalio's book Principles is one of the best discussions about artificial intelligence that I have run across: SYSTEMIZED AND COMPUTERIZED DECISION MAKING.

This YouTube.com video, AI and Algorithmic Decision Making, provides an excellent overview that is very approachable to business professionals.

There is one notion that I disagree with that comes across in this article. The article gives the impression that you literally "program" rules (i.e. put rules in code). For a number of reasons, that is not a good idea. If logic and rules is expressed in "code"; then only programmers can add new logic/rules, maintain the logic/rules, and business professionals have to educate the coders on the business logic that they are trying to get programmed.

There is a better way. If the "computer code" and the "business logic/rules" are separated, then programmers can write code and business professionals can work with and maintain the rules/logic. Using this approach, the rules/logic are represented in declarative form in some machine-readable format. A rules engine or logic engine then uses those rules/logic.

So, rather than writing your "principles" code, you write them as declarative rules. Closed systems are necessary, you cannot just add "stuff" haphazardly. Open ended systems might not work reliably, there is a chance of error. If the "future can be different than the past", you have to be very careful. Open versus closed systems seems to be described by control theory.

Plenty of rules engines or logic engines already exist. The missing piece is the computer readable business rules. Rules for creating a financial report look like this. (Here are many more examples.)

And so, while I would not dispute that understanding how to code is helpful. But, you really don't need to "learn to code". If you want to understand the details better, I would invite you to read Artificial Intelligence and Knowledge Engineering Basics in a Nutshell.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Database that Generates Pixel Perfect Rendering

I updated an example that now does something really interesting. If you go to this PROOF+COMMON+RENDERING example you will find this Inline XBRL Instance. That was generated using the Microsoft Access database in this ZIP archive. Now, keep in mind that I am not really a very good programmer, but it will give you an idea of how to generate renderings. I don't have an interface for editing the "cells" that drive the rendering, I just edit the database table.

That might not look like much, but you could create a complete XBRL-based 10-K for Microsoft, Apple, Google, Amazon, or anyone else using that Microsoft Access database. Clearly you would want an XBRL processor and XBRL Formula processor to verify that everything is working correctly (that is what I do).

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

HBR: Digital Transformation Is About Talent, Not Technology

A Harvard Business Review article by Becky Frankiewicz and Tomas Chamorro-Premuzic, Digital Transformation Is About Talent, Not Technology, points out:

“...the best way to make your organization more data-centric and digital is to selectively invest in those who are most adaptable, curious, and flexible in the first place.”

“Technical competence is temporary, but intellectual curiosity must be permanent.”

“A much bigger competitive advantage is to harness valuable data, having the necessary skills to translate that data into meaningful insights, and above all being able to act on those insights.”

Excellent read. It seems as thought the risk of not adapting is increasing significantly.

This article points out that digital transformation is a leadership problem.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

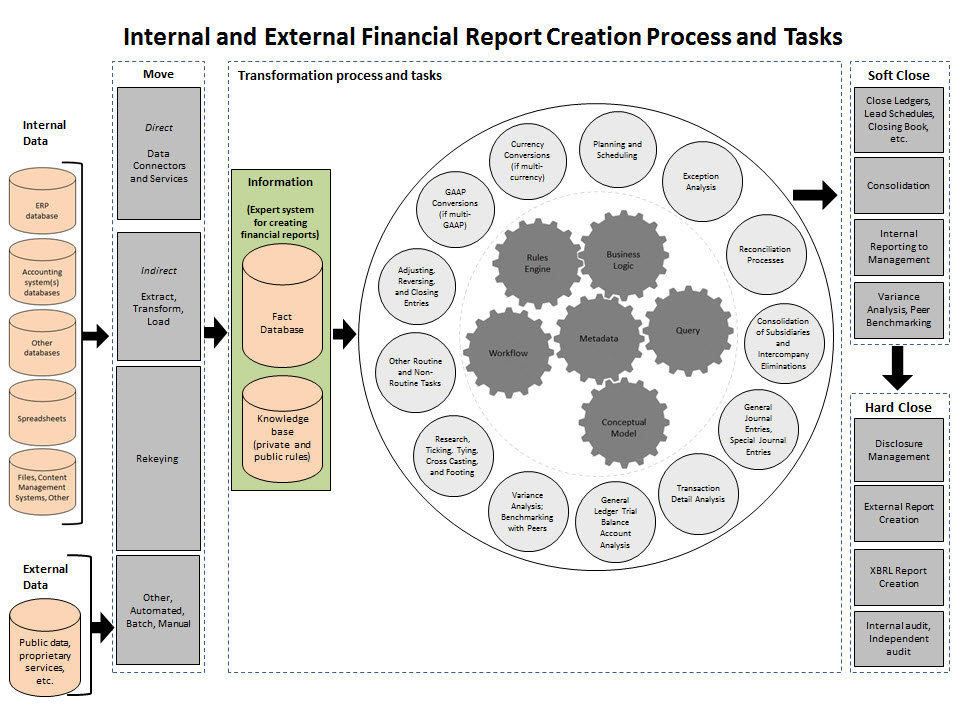

Essence of Accounting

By understanding the Essence of Accounting it is possible to understand likely futures of accounting, reporting, auditing, and analysis.

Given that the CEO of IBM believes that every company will ultimately become "an AI company", that each of the Big 4 are telling their clients that the fourth industrial revolution is a thing and to pay attention to AI, and at least one of the Big 4 has provided a pretty good vision of what finance will look like in the future; significant change is pretty much a forgone conclusion.

But change to what? Think human-machine collaboration. How exactly will all this artificial intelligence stuff work? Well, no one really knows with certainty but there has been some significant experimentation; but I have placed my bet.

Fundamentally, accounting works like this: INPUT (journals) >> PROCESSING >> OUTPUT (report)

The basics of accounting can be explained using basic math and/or graph theory. Complexity exists but that complexity comes in the form of explainable patterns. With the complexities of the real world, it can look more like this:

If you understand the essence of accounting and you understand the essence of how computers work then all this stuff is actually pretty straight forward and easy to grasp.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print