XBRL-Based Financial Report Ontology Prototype

I was trying to articulate a financial report ontology using OWL. I did not really like what I created because I did not understand it and very few, if any, other business users understood it. How can you tell if the ontology is correct if business users don't understand what they are looking at?

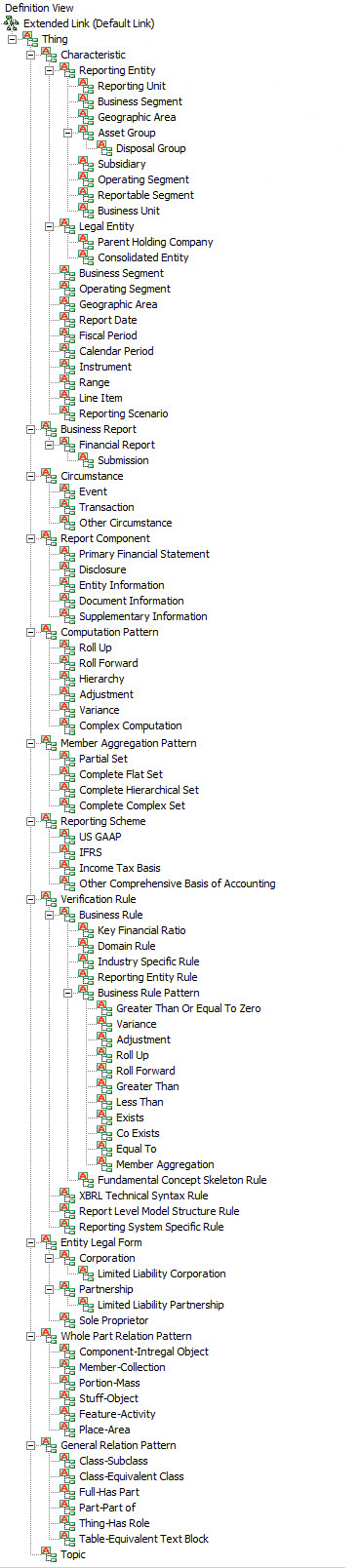

And so I did the same thing using XBRL (prototype). See the graphic below. This is not perfect, but it is WAY, WAY closer to being understandable. Plus it meets the needs of business users because computations can be easily articulated using XBRL Formula and XBRL calculation relations.

While I am not totally convinced that I can really call this an ontology, it certainly has a significantly higher level of semantics than most XBRL taxonomies that are being created.

Here is the XBRL taxonomy schemas for the pieces of this:

- Financial report ontology (fro): http://www.xbrlsite.com/2014/Protototype/fro/fro.xsd | HTML | XML

- Topics: http://www.xbrlsite.com/2014/Protototype/fro/topics.xsd

- Disclosures: http://www.xbrlsite.com/2014/Protototype/fro/disclosures.xsd

- Key ratios: http://www.xbrlsite.com/2014/Protototype/fro/keyRatios.xsd

- Fundamental accounting concepts (fac): http://www.xbrlsite.com/2014/Protototype/fro/fac.xsd

- Fundamental accounting concept rules (XBRL Calculations): http://www.xbrlsite.com/2014/Protototype/fro/fac-rules.xsd

- Fundamental accounting concept rules (XBRL Formula): http://www.xbrlsite.com/2014/Protototype/fro/fac-formulas.xml

- Map US GAAP XBRL Taxonomy to fundamental accounting concepts: http://www.xbrlsite.com/2014/Protototype/fro/fac-MAP-to-USGAAP-definition.xml

- Arcroles (which provide semantics): http://www.xbrlsite.com/2014/Protototype/fro/fro-arcroles.xsd

The primary thing that I was trying to do in OWL is to get one graph of all the "things" which play a role in a financial report. Well, I now have that.

I am not saying that all of this is correct. Got something better? Let me know. Have ideas for improvements? Send me an email.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments