Public Company XBRL-based Digital Financial Report Quality Inches Forward

Not a lot of movement in the quality of public company XBRL-based financial reports, but quality did improve slightly. See the information below:

Because there is not a lot going on I want to introduce a handful of additional quality measures. In order to read any information from an XBRL-based digital financial report, you have to be able to locate the reporting economic entity of the report, the current balance sheet, and the current year-to-date income statement. Further, you want to know that the information is trustworthy and if you cannot be sure the balance sheet, income statement, and cash flow statement to not roll up correctly it raises a red flag in your mind as to the reliability of the information.

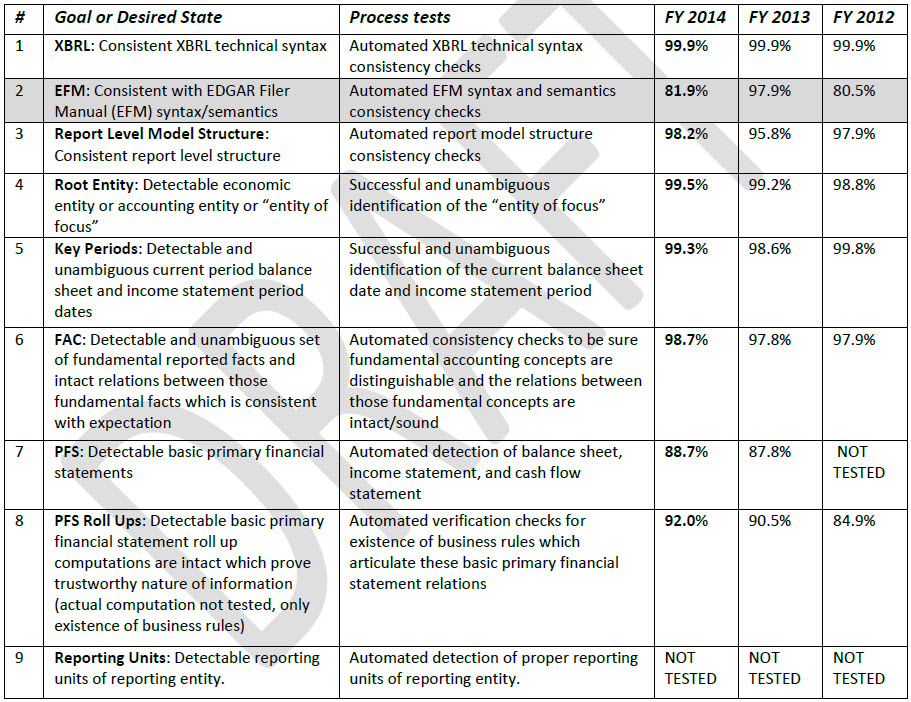

Here are six additional quality measure which are part of what I call the "minimum criteria" for making use of information reported in an XBRL-based digital financial report. You can see page 2 of this document for a three year comparison of this information. Here is where things stand now:

- Ambigous root economic entity: Only 14 out of 6,683 entities, or about .21%, get this wrong.

- Ambigous current balance sheet date: Only 29 out of 6,683 entities, or about .5%, get this wrong.

- Ambigous current income statement year-to-date period: Only 41 out of 6,683 entities, or about .7%, get this wrong.

- No balance sheet calculation relations provided: Only 44 out of 6,683 entities, or about .66%, don't provide these calculation relations.

- No income statement calculation relations provided: Only 176 out of 6,683 entities, or about 2.63%, don't provide these calculation relations.

- No cash flow statement calculation relations provided: Only 202 out of 6,683 entities, or about 3.02%, don't provide these calculation relations.

It appears that about 98% of public companies provide XBRL calculation relations for the primary financial statements. Note that for 2014, 2013, and 2012 the percentage of public companies that provided calculations relations for the primary financial statements was 92.0%, 90.5%, and 84.9%; respectively. So, that is improving. Below is a summary for all the minimum criteria for the past three years:

(Click image for larger view)

(Click image for larger view)

The SEC seems to be putting additional pressure on public companies to provide the required XBRL calculation relations. I look forward to the 2015 analysis of 10-Ks to see how much improvement occurred over the past year.

* * *

Previous fundamental accounting concept relations consistency results reported: December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments