One Global Standard Model for All Stakeholders

Modano has a motto: "One Model for All Stakeholders". That is explained well in this YouTube video, One Model Technology. They talk about streamlining disjointed processes. If you go to their web site you can see beautifully laid out sample PDF documents and there is even a Sample Model you can explore. At the heart of Modano sees to be Microsoft Excel per this download page. All this is built on top of what they seem to refer to as their "One Model Technology".

But there is a problem. That model is not standard. Because the model is not standard, there are some issues you will run into.

But what if there was a "one model technology" that really was one model and STANDARD!

Enter the Logical Theory Describing Financial Report, the Standard Business Report Model (SBRM), the Pacioli rules/logic/reasoning engine, the Luca financial report creation tool, the XBRL global standard, and a method that ties all these things together to effectively streamline disjointed accounting, reporting, auditing, and analysis processes.

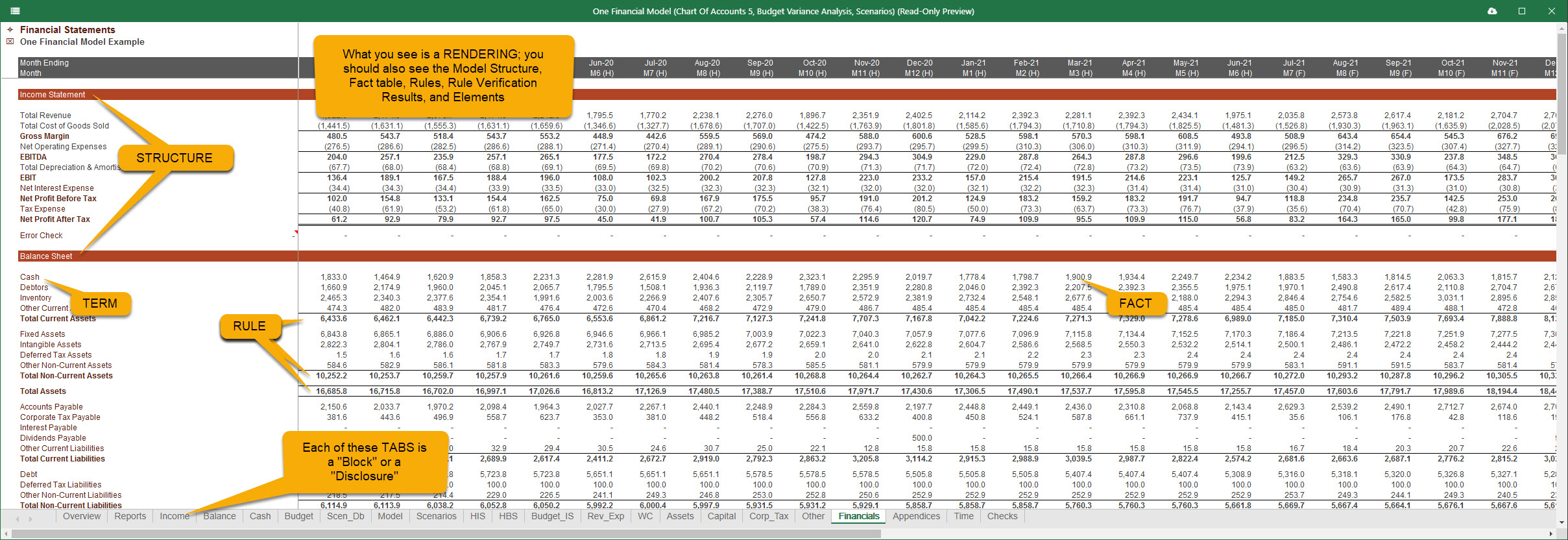

Imagine "One GLOBAL STANDARD MODEL for All Stakeholders”. Well, you don't really need to imagine it; all this exists today. (Click the image for a larger view.)

So how is what I pointing out different than the "One Model Technology" of Modano? Here are the benefits of those two words "global standard":

- You get ONE MODEL but that model is FLEXIBLE and ADJUSTABLE enough to support the unique reporting needs of literally ANY ECONOMIC ENTITY. This has been proven by the fact that over 6,000 economic entities that report to the SEC using US GAAP and about 400 reporting to the SEC using IFRS and about 10,000 reporting to the ESMA using IFRS all use one fundamental financial report model.

- You get machine-readable process control mechanisms that makes sure those adjustments to the global standard model stay within permissible boundaries and therefore don’t break the fundamental logical model.

- You get a global standard syntax, XBRL, that can be used to move information from one step to the next step in your processes. But it does not stop there. That same XBRL global standard syntax can be used to move information throughout the financial reporting supply chain. From accounting system to reporting; from reporting to your auditor; from your audited report to regulators, investors, and financial analysts.

- Digital distributed ledgers are used to make certain that the information has not been manipulated, improving trust and guaranteeing provenance of the information.

- A powerful ISO Modern PROLOG GLOBAL STANDARD rules/logic/reasoning engine can operate over all the financial information in that one flexible, adjustable model.

- RULES for controlling processes and model manipulations are represented in a standard global syntax, XBRL. So, all your models are transferable from system to system using that global standard XBRL technical syntax.

- Global standards based models can be transferred from an economic entity to their CPA and auditors. Models can be transferred to shareholders, analysts, investors, and regulators rather than being locked into a proprietary enterprises internal reporting system.

- Handles not only numerical financial information, but also non-financial information such as sustainability reporting, accounting policies, textual disclosures whether the information comes from your accounting systems or any other information source.

- Software vendor lockin is reduced, forcing software vendors to compete by adding value rather than making it hard for you to change software applications.

That, my friends, is the power of global standards and improving the semantic hygiene just a bit. When financial report models are properly implemented financial accounting, reporting, auditing, and analysis flows without the need for rekeying information or all the other grueling but unnecessary tasks caused by a lack of these standards or improperly implemented financial report knowledge graphs.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments