BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Microservices

The first time I heard the term microservice was from Andrew Noble the creator of Accziom where he offers microservices.

As pointed out by Dave McComb in Software Wasteland, there is a problem that causes software to be 10 times or even 100 times more complicated than it needs to be. Not having data centric applications (i.e. application centric or document centric) makes it harder to build software. I would take this even one step further and thinking information centric software.

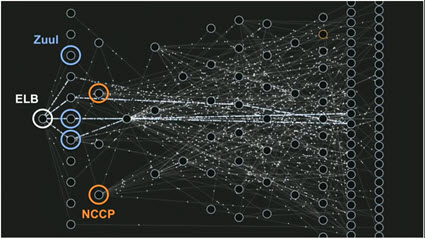

Here is an excellent video, A Netfiix Guide to Microservices. The video has a nice graphic that I find useful in visualizing microservices.

Now, that video above talks about very low-level processes and tasks. Now, the notion of microservices can also be used to describe the tasks and processes involved in the full record to report process.

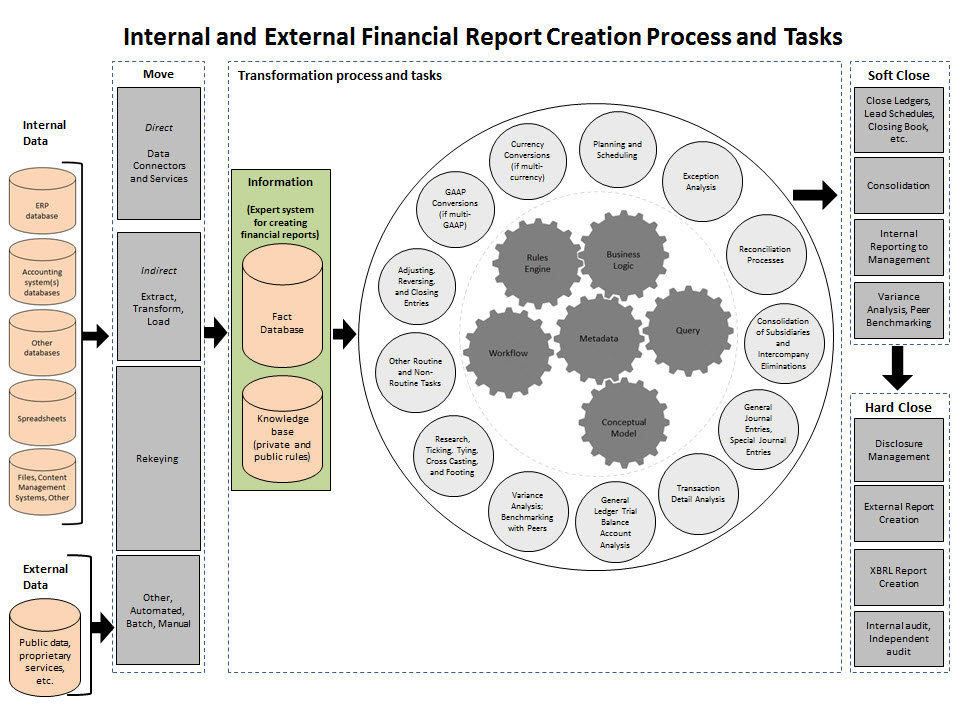

This graphic below shows many of those tasks and processes:

(Click image for larger view)

(Click image for larger view)

So imagine a "general ledger" microservice that can talk to a "transaction entry" microservice or a "close the books" microservice and so forth. Imagine that these microservices are intelligent software agents that exchanged standards-based inputs and outputs. Imagine that they worked at the "information block" level, effectively changing hypercubes of information held together by machine-readable accounting logic, the rules of math, and machine-readable accounting standards.

Today, there are plenty of these sorts of microservices that are carried out by an accountant, a report, green eye shades, and an Excel spreadsheet. Then tens if not hundreds of Excel spreadsheets are emailed around. Software silos are "integrated" using Excel spreadsheets, copying and pasting, RPA (robotic process automation), and other band aids and bailing wire to hook the kludge that people call their accounting information system together.

Break down silos rather than create them.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Overcoming Silo Mentality, Composite View of System

Deming points out that the typical way of solving problems is to break a system into pieces or subsystems and get each subsystem to run optimally. But that is not systems thinking. Systems thinking is about working together as opposed to working apart separately.

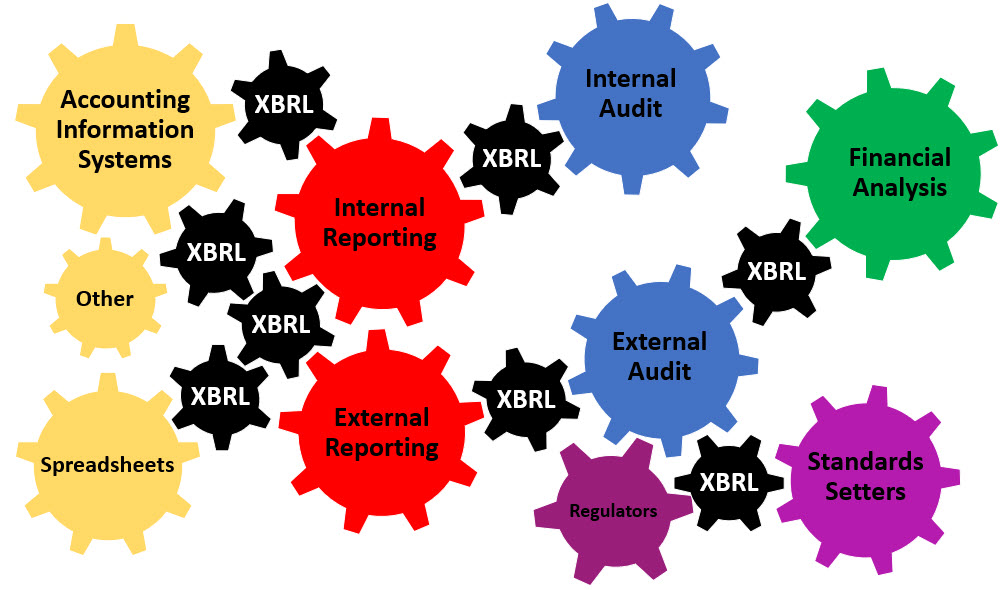

Here is an abstract view of the system I am concerned with: accounting, reporting, auditing, analysis.

(Click image for larger view and more details)(This image is a more tangible view of the reporting part of that system.)

(Click image for larger view and more details)(This image is a more tangible view of the reporting part of that system.)

So I would like to provide as good as a composite view of the entire system from pulling together pieces of this system that exist. This view also helps you see gaps within the individual silos. I have shown that the entire record to report process can be automated. Have a look, you might find this useful:

- Accounting: PWC provides an AI assisted bookkeeping system which they call InsightsOfficer. This seems promising, and I don't know for sure, but I would speculate that their bookkeeping system is not aware of XBRL and machine-readable stuff offered by XBRL. For example, it would make a lot of sense to be able to map the bookkeeping system chart of accounts to XBRL taxonomy concepts within the system. For example, here is how I did exactly what I am describing for the Not for Profit Financial Reporting Scheme prototype I created. Here are microservices that tie processing tasks and steps together. A little additional information needs to be added to the accounting system.

- Reporting: PWC does not seem to offer a reporting product per se. There might be a report writer within the bookkeeping product they offer. But, I speculate that bookkeeping product does not leverage XBRL or support outputting XBRL-based financial reports. But what if it did? For example, here is an autogenerated Inline XBRL financial report prototype. An example of a report creation tool is cloud-based Luca.

- Auditing: PWC does offer financial statement audit. However, does the PWC financial statement audit process leverage anything related to XBRL? Doubtful. I hope I am wrong. Does the PWC financial audit process include logic engine capabilities such as what Pacioli offers? Doubt it. Mindbridge says they have artificial intelligence assisted audit capabilities. But, does Mindbridge leverage XBRL-based machine readable information? Nope; I have talked to Mindbridge, they agree that it is a good idea, but they are not there yet.

- Analysis: Auditors, such as PWC do analytical review procedures as part of their audits. They compare a current report with prior year reports, look for variances, and then analyze those variances. Does PWC leverage XBRL-based reports for this variance analysis? Doubt it, particularly if they don't output reports into XBRL. Auditors and companies also benchmark their financial information with their peers. Investors, regulators, and creditors analyze financial report information. So here is an interface to the EDGAR repository of public company financial reports provided by XBRL Cloud. Does XBRL Cloud leverage the financial reporting scheme machine-readable information for effectively extracting information from reports? Some, but not enough. Does XBRL Cloud put all the reporting information into a database to make analysis faster? Nope. Here is a database provided by Reportix that would work nicely. Pesseract is a decent report analysis tool, but it has a lot of missing pieces.

All of the pieces are there, but the pieces have not been put together effectively yet. Note the word "yet". Auditchain holds itself out as the worlds first continuous accounting, reporting, auditing, and analysis platform. They don't have all the pieces in place yet. But, they have at least articulated the possibility of putting all those pieces together.

Yes, there are gaps in functionality. The gaps will be filled. Yes, companies will build proprietary pieces to the full system. But others will build standard pieces that fit together like modules or Legos. So WHEN will these gaps be filled? I don't think all the gaps will be filled by the end of 2022. But it will not take longer than 2025. My prediction would be sometime in 2023, 2024, or 2025.

There is already more software and pieces in place then you might think. I have been working on figuring all this out for about 20 years. This is science and math. This is not even rocket science; all you need to understand is undergratuate algebra to see THAT this can work. You do need a lot of accounting knowledge and the ability to communicate with good technical professionals.

Folks, this is inevitable. Not only is it inevitable, it is imminent. This is not a question of "if", it is a question of "when". Then you will see why I believe that this will be the biggest change in the institution of accountancy in 500 years.

Anyone care to bet against this? Let me know and tell my why and/or where I am seeing this incorrectly.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Auditors Need High Digital IQ

"Tomorow's audit, today. The new equation of people + technology." That is a statement made on this PWC web page. Scroll down a bit and you see this graphic of "One auditor. Three mindsets." Audit IQ, Digital IQ, Experience IQ.

So what exactly is a "digital IQ" and how do you get a digital IQ or improve the one you have?

So what exactly is a "digital IQ" and how do you get a digital IQ or improve the one you have?

What PWC is probably refering to is all the stuff I have become to recognize that is critically important to understand the next phase in the evolution of financial accounting, reporting, auditing, and analysis.

We are transitioning from the industrial age to the inforrmation age. Accountants, as well as others, are going to need to adapt.

A paradigm shift is occurring, a transformation. Gartner defines transformational as something that "enables new ways of doing business across industries that will result in major shifts in industry dynamics." Major shifts means lots of change and some winners and some losers.

The territory of accounting, reporting, auditing, and analysis are changing. Old maps will not work to understand this change. You need a new map. Mental maps that have worked for the past 40 years will not work for the next 40 years. Since the territory has changed, old maps simply will not work for you.

But how do you get this new map?

To get a new map, I would suggest reading the following documents:

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

PWC Offers Bookkeeping Services

PriceWaterhouseCoopers (PWC) with it's new product InsitesOfficer provides bookkeeping services.

My question is: why not connect automated financial reporting to the bookkeeping? Then you would have continuous accounting and reporting. Then, why not also connect audit to the bookkeeping and reporting?

PWC seems to be building out a new digital audit platform. However, they don't mention anything such as rules engines or rules creation software. True Comply seems to be doing some rules based stuff. Here is a full list of products PWC offers.

Ah, here is information about what PWC is calling Aura which is for financial statement audit.

What if PWC connected more of these things together into one workflow.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

University of Michigan and City of Flint Partner for XBRL-based Reporting Project

The University of Michigan and the City of Flint, Michigan are partnering to undertake an XBRL-based financial reporting project. Read more here.

Also note this paper, An Open Data Standard for Local Government Financial Reporting: How it Could Work in Michigan.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print