BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from February 1, 2017 - February 28, 2017

Properly Differentiating Data, Information, and Knowledge

The terms data, information, and knowledgeare easily confused. You can understand how to properly differentiate these terms by watching this 4 minute video by Nick Milton.

Knowledge is the piece of information that you need right now that allows you to take effective action. Actionable information.

Knowledge based systems provide capability and know how. Knowledge management is about creating a managed system that routinely and systematically institutionalizes knowledge and ensures that people have the knowledge they need to make correct decisions, take effective action, take the correct action.

The result of poor knowledge management are:

- Mistakes repeated

- Successful practices not replicated

- Slow rate of learning

- Knowledge lost when staff retires or gets a new job

We live in the information age, not the "data age". How do you turn data into information? How do you store information? How many mistakes does your organization repeat over and over? How are your processes for capturing good ideas and repeating them? How fast does your organization learn? How much knowledge will be lost when staff leave your organization?

Charlie

in General Information

|

Charlie

in General Information

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Understanding XBRL's Role in the Fourth Industrial Revolution

We are in the midst of the fourth industrial revolution. Are you ready? Do you even know what Industry 4.0 is or what it means for you?

Here is a list of the four industrial revolutions:

- Mechanization, water power, steam power.

- Mass production, assembly line, electricity.

- Computer and automation.

- Cyber physical systems.

In their paper Imagineering Audit 4.0, Jun Dai and Miklos Vasarhelyi of Rutgers University provide a comprehensive and complete description of how industry will work in the future and therefore why a knowledge media such as XBRL is a critical required part of the information infrastructure for turning their vision into a reality.

Dai and Vasarhelyi describe Industry 4.0 as follows:

Originating in Europe and spreading to the US, Industry 4.0 emphasizes six major principles in its design and implementation: interoperability, virtualization, decentralization, real-time capability, service orientation, and modularity. The objective of Industry 4.0 is to increase the flexibility of existing value chains by maximizing the transparency of inbound and outbound logistics, manufacturing, marketing, and all other business functions such as accounting, legislation, human resource, etc.

Basically, what Industry 4.0 means is that technologies will be used to dramatically improve the efficiency and effectiveness of businesses and other organizations. What does this mean? Some say that it means 47% of jobs in the United States are at risk from automation.

No one knows exactly what this fourth industrial revolution will mean, but based on the other three I think the fourth will turn out just fine if you make sure your skill set is up-to-date. Information barbarians will likely not fare well. It is far better to understand digital.

But let's get back to XBRL's role in Industry 4.0. On page 16 of the paper, in the section titles "Standardization of information and data", Dai and Vasarhelyi point out the important role standards play in this new world:

To facilitate information exchange and analysis in Audit 4.0, regulators and standardization agencies should create suitable standards that define the formats and naming rules of commonly used data.

On page 14, the role of pre-determined business rules is pointed out:

In addition, business processes will be monitored against pre-determined rules to detect violations of key controls, and cross-verified via certain continuity equations.

As I have said before, business rules prevent anarchy. For increased efficiency and effectiveness in business processes to be realized, business information exchange will need to work correctly. For meaningful machine-based information exchange to work, you need pre-determined rules relating to technical syntax, domain semantics, and workflow. It really is that straight forward. This set of principles helps you understand the details.

Further, while it might not seem to be the case because of quality issues; XBRL-based reporting by public companies to the SEC helps accountants and others figure out how to use these sorts of technologies. It is actually rather amazing that about 7,000 different companies can represent rather complex financial information and communicate that information to the SEC and get 98.96% of that information right. On average, 84.7% of companies get all of the measured information right, and a set of 8 software vendors manage to get 97% of more of their reports correct as measured by the checks that I perform.

But 98.96% is not good enough. What is good enough? Six sigma is one target manufacturing has used, that is 99.99966% of everything being correct. Is that good enough for information-based processes? Well, it is a good minimum target to shoot for currently.

Conceived of in 1998 and turned into a global standard by the American Institute of Certified Public Accountants (AICPA) in 1999; XBRL is being perfected as a critical knowlege media ready for Industry 4.0.

If you are an accountant or other business professional and you want to understand digital better, I would suggest Part 1 - Foundation for Understanding: Background, Framework, Theory, Principles.

#################

PWC: Are you ready for tomorrow no matter what tomorrow brings? (4IR)

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Changing Old School Financial Report Creation Processes

No one really disputes the fact that old school processes, practices, and procedures for creating external financial reports contain inefficiencies. For example, consider these four sources:

- CFA Institute: calls for "...greater efficiencies within the current inefficient system" [of creating financial reports].

- Gartner: "...average Fortune 1000 company used more than 800 spreadsheets to prepare its financial statements"

- Ventana Research: "...for larger companies, assembling the periodic external reports typically is an inefficient and error-prone process."

- PriceWaterhouseCoopers: "...old school manual processes..." and "commonly cut and pasted, rekeyed, or manually transferred into word processing and spreadsheet applications used for report assembly and review process steps"

Have the stars aligned, creating an opportunity for reinventing these processes? I think so.

What has changed?

The answer is that one thing has changed which has enabled another thing. If you read the first PDF I referenced above, you will notice that each of those four organizations hails XBRL or "structured data" as the way to to make financial reporting processes more efficient.

That is not quite right. XBRL or structure data is not the change that will make processes more efficient; structured data enables the change to occur. This video, How XBRL Works (which now has over 46,000 views), helps you see what structured information is as contrast to unstructured information.

So, XBRL or structured data is the enabler of a change, it is not the change itself.

Again I ask, then what changed? Well, two things changed.

First, the structured information lets a computer effectively address the individual pieces of a financial report. Because of the structure, software applications can do things with the individual pieces of the report. Basically, you can take measurements of structured information; that was impossible when financial reports were unstructured information.

Second, because you can address or measure or otherwise work with the individual pieces that make up a financial report; more processes, procedures, and other tasks used in the report creation process can be automated.

Old school review processes are almost 100% manual. It does not have to be this way. On the other hand, there is ZERO probability that 100% of the financial report creation process will be automated. That is absurd.

What percentage CAN effectively be automated though? Some percentage. That percentage is greater than 1%. Is it 10%? Is it 20%? Is it 50%? More than that?

Further, there will no doubt be quality improvements also. There is NO WAY that a process that is nearly 100% manual can be of perfect quality. So, there is some level of quality problems that exist in the current old school processes. But, you cannot see those problems or measure the problems because, you guessed it, the current financial reports are unstructured and you cannot address the pieces of a report.

Just because you cannot measure quality problems does not mean that quality problems do not exist. They exist.

How exactly will financial report creation processes be made more efficient? The answer to that question is machine-readable business rules. Remember, business rules prevent anarchy.

More on that later...so stay tuned!

But have the stars aligned enough to allow for a real change to the old school manual processes of creating an external financial report to truly be replaced? That depends entirely on whether how clever software creators are in making all the pieces of knowledge based systems usable by business professionals.

It really is that simple. The law of conservation of complexity states very clearly, you leave one required piece out, your system will simply not work.

There is zero probability that professional accountants will want to go to the IT department as part of getting the external financial reports out. That will NEVER happen. They would rather struggle with the currently manual processes than lose any control over the process. Proof of that: current processes.

Some software creators have provided small incremental improvements to processes. If knowledge based systems can effectively be utilized in financial report creation processes, that will be a disruptive innovation, not just another incremental improvement.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

European Listed Company Financial Reporting to Use XBRL

In December 2016, the European Securities and Markets Authority (ESMA), the European Union agency responsible for the regulations that govern securities and the conduct of public markets within the EU, announced that starting January 1, 2020, public companies that prepare consolidated IFRS financial statements will provide them in the structured format XBRL.

ESMA is in the process of developing the detailed technical rules, will field test their system, and will submit the details of their proposed solution to the European Commission for endorsement by the end of 2017.

What does that mean? Well, it seems to mean that another 10,000 or so listed companies will be reporting using XBRL-based structured information. ESMA will be using Inline XBRLwhich basically XBRL embedded within XHTML. The SEC will likely move to Inline XBRL also.

Hopefully the ESMA will learn from the SEC experiences with XBRL and avoid the quality issues encountered in the XBRL-based public company financial reports. Time will reveal the answer. One advantage of Inline XBRL is that it helps separate the presentation of information (in the XHTML) and the representation of information (in the XBRL).

What will software vendors do? Will they build more bolt-on solutions to the current barbaric processes and procedures for creating financial reports or will they innovate and create intelligent XBRL-based digital financial reports using improved processes that truly leverage the technology? Will the quality pivot and the cost pivot occur?

Has the maturity levelof XBRL taxonomies, creation software, business rules available, and the knowledge of business professionals reached a point where the pieces can be put together appropriately?

Will Europe lead? Great opportunity to re-think financial reporting processes, bringing them out of the dark ages. Time reveals all.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Intelligent XBRL-based Financial Reporting Maturity Levels

I have made the comparison of digital blueprints, CAD, and digital financial reports before. Ask yourself a question: How useful would a digital CAD blueprint be if that blueprint had errors? If a construction contractor put together a building with a blueprint that had errors, or if someone tried to assemble an iPhone with pieces designed with blueprints that had errors, or if information was supplied to a numerically controlled machine that creates engine parts; how would that work out?

Clearly errors in XBRL-based digital financial reports would cause similar problems when investors, analysts, regulators, and others used information from the report.

So, how exactly does a digital CAD drawing achieve high quality? Why can CAD work as a global standard for the design, engineering, and creation supply chain; but XBRL-based digital financial reports have to be so error prone? What causes the difference?

How can it be that draftsmen, architects, engineers, designers, and others can successfully create near error-free digital blueprints but accounting professionals cannot create near error-free digital financial reports? Why is that?

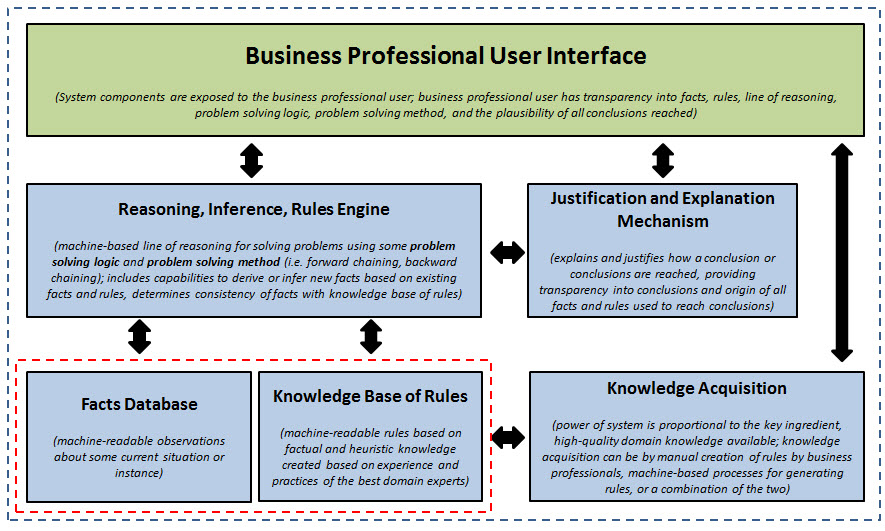

Like many things, intelligent XBRL-based digital financial reporting will evolve and go through different maturity levels. Just like CAD, an intelligent XBRL-based digital financial report is a knowlege based system. Such a system has specific parts. This diagram outlines those parts and shows the relations between each part of a knowledge based system:

(Click image for larger view)

(Click image for larger view)

Here is an overview of each part part of a knowledge based system such as an intelligent XBRL-based digital financial report:

- Database of facts: A database of facts is a set of observations about some current situation or instance. The database of facts is "flexible" in that they apply to the current situation. The database of facts is machine-readable. An XBRL instance is a database of facts.

- Knowledge base (rules): A knowledge base is a set of universally applicable rules created based on experience and knowledge of the practices of the best domain experts generally articulated in the form of IF…THEN statements or a form that can be converted to IF...THEN form. A knowledge base is "fixed" in that its rules are universally relevant to all situations covered by the knowledge base. Not all rules are relevant to every situation. But where a rule is applicable it is universally applicable. All knowledge base information is machine-readable. An XBRL taxonomy is a knowledge base. Business rules are declarative in order to maximize use of the rules and make it easy to maintain business rules. Knowledge that makes up the knowledge base is acquired using manual or automated knowledge acquisition processes.

- Reasoning engine: A reasoning engine provides a machine-based line of reasoning for solving problems. The reasoning engine processes facts in the fact database, rules in the knowledge base. A reasoning engine is also an inference engine and takes existing information in the knowledge base and the database of facts and uses that information to reach conclusions or take actions. The inference engine derives new facts from existing facts using the rules of logic. The reasoning engine is a machine that processes the information. An XBRL Formula processor, if built correctly, can be a reasoning engine and can perform logical inference.

- Justification and explanation mechanism: When an answer to a problem is questionable, we tend to want to know the rationale behind the answer. If the rationale seems plausible, we tend to believe the answer. The justification and explanation mechanism explains and justifies how a conclusion or conclusions are reached. It walks you through which facts and which rules were used to reach a conclusion. The explanation mechanism is the results of processing the information using the rules processor/inference engine and justifies why the conclusion was reached. The explanation mechanism provides both provenance and transparency to the user of the expert system.

These four pieces are exposed to the users of the knowledge based system within software applications that is used by a business professional.

Software applications must provide all of these pieces. The law of irreducible complexitystates basically that "A single system which is composed of several interacting parts that contribute to the basic function, and where the removal of any one of the parts causes the system to effectively cease functioning." That means that each of the parts in the diagram need to exist for the system of an XBRL-based digital financial report to work correctly.

Further, the system must be usable by business professionals. The law of conservation of complexity essentially states, "Every software application has an inherent amount of irreducible complexity. That complexity cannot be removed from the software application. However, complexity can be moved. The question is: Who will have to deal with the complexity? Will it be the application user, the application developer, or the platform developer which the application leverages?"

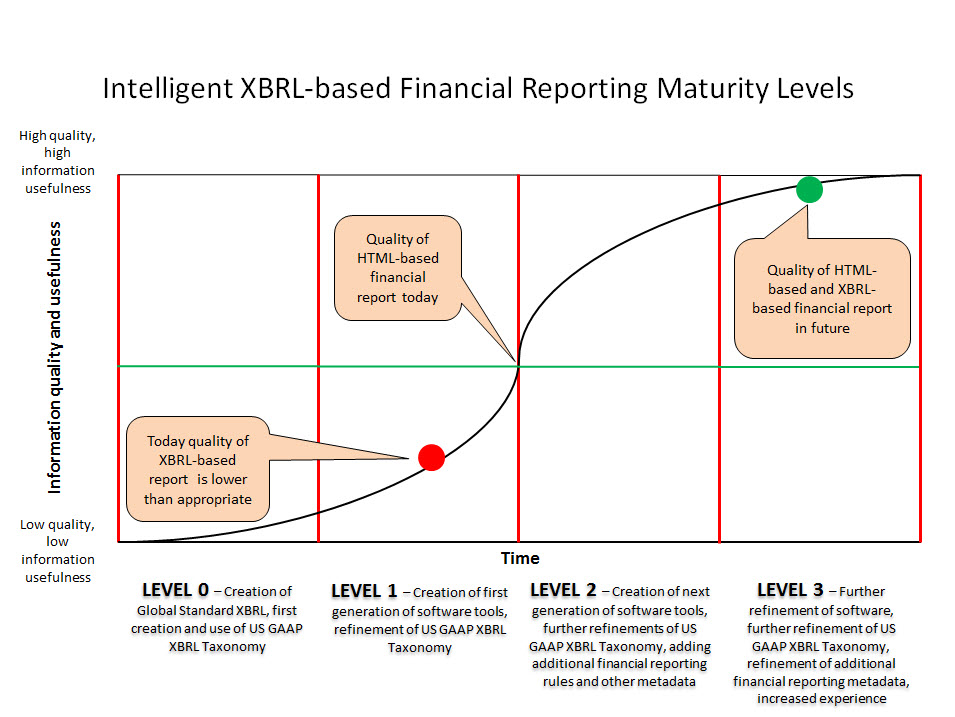

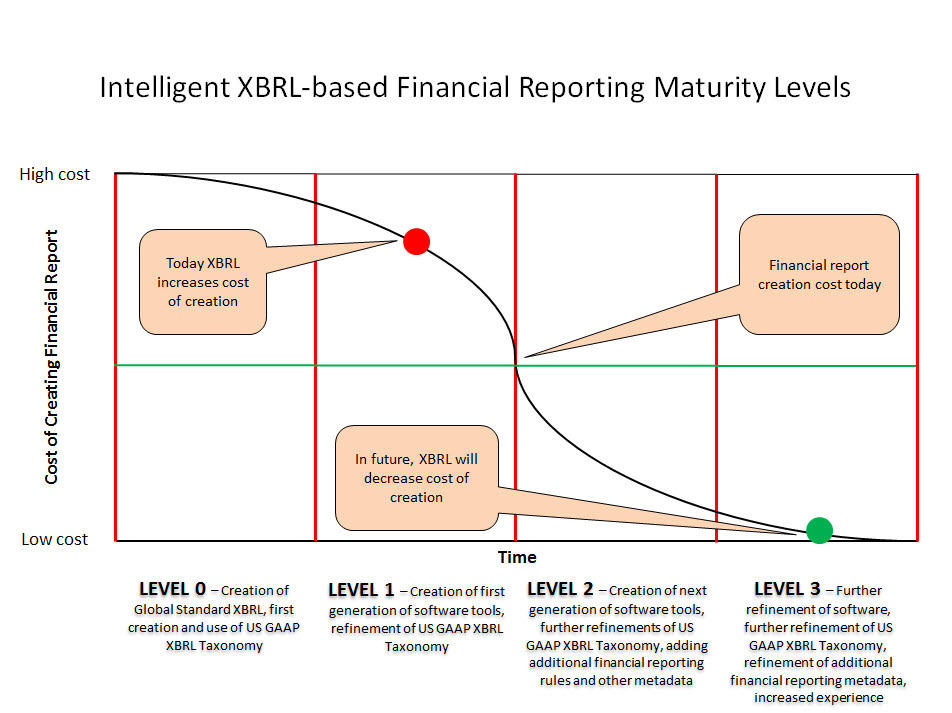

Today's software applications do not provide all of these parts completely or in a form that is usable by business professionals creating intelligent XBRL-based digital financial reports. But when software does provide all of these pieces, two pivots will occur. The two graphics below show that the benefits of XBRL-based digital financial reporting will flip the dynamics of the financial reporting process. A disruptive innovation will occur. The barbaric processes used to create financial reports today will evolve and be replaced by new, better, faster, and cheaper processes.

These three things need to occur:

- More business domain knowledge in machine-readable form put into the knowledge base (rules).

- Better software applications which more precisely provide all the components of a knowledge based system in a form useable by business professionals.

- Business professionals need to learn a handful of things about knowledge engineering so that they don't need to rely of knowledge engineers or information technology professionals to create financial reports.

Quality pivot:

(Click image for larger view)

(Click image for larger view)

Cost pivot:

(Click image for larger view)

(Click image for larger view)

Blueprints made the flip to digital in the 1980s and 1990s. Do you believe these changes are possible for financial reporting?

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print