Public Company Quality Continues to Improve, 9 Quality Leaders

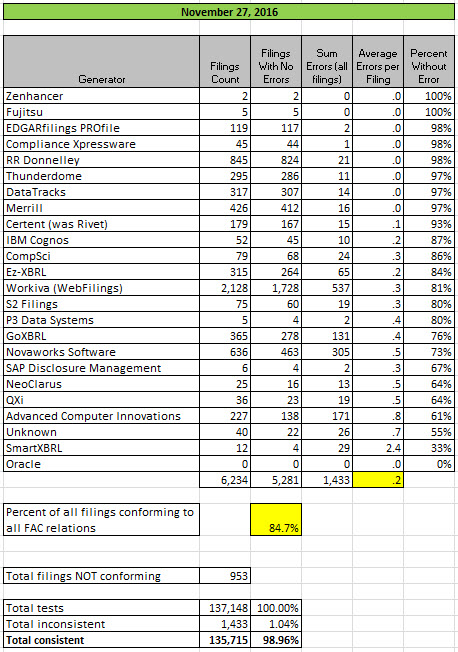

Nine quality leaders have laid the foundation for semantic interoperability and established a clear path to zero defect XBRL-based financial reports. A significant milestone was reached this month. The total number of filings that had inconsistencies dropped below 1000, currently only 953 have errors while 5,281 public companies are consistent with the fundamental accounting concept relations.

The document, Summary of Issues of Quality Leaders, inventories the complete list of fundamental accounting concept relations inconsistencies of every quality leader. In so doing, the document lays a path from the current high quality levels to zero defect levels. Remember, there are exactly three reasons for inconsistencies to be reported:

- The creator of the XBRL-based financial report made a mistake. To correct this mistake, the report must be fixed.

- The creator/maintainer of the US GAAP XBRL taxonomy made a mistake. To correct this mistake, the US GAAP XBRL Taxonomy must be fixed.

- The creator/maintainer of the fundamental accounting concept relations business rules made a mistake. To correct this mistake, the business rules must be fixed.

It really is that simple. The document mentioned above shows every inconsistency. Most of those 80 inconsistencies in the 69 reports are not disputed, filing agents/software vendors agree that they have made a mistake and they will fix the public company XBRL-based financial report. But they don't agree with all of the inconsistencies. What then? Who serves as the referee to establish what must be fixed: the filing, the taxonomy, or the business rule? This remains a bit vague.

But as the number of errors is reduced, the areas of disagreement begin to reveal themselves in the XBRL-based financial reports. The vast majority of inconsistencies are not disputed. While the quality leaders have fixed their mistakes, the quality laggards have not.

This ZIP archive contains an Excel spreadsheet that contains a listing of all 1,433 inconsistencies which exist in the 953 public company XBRL-based financial reports. If each of the inconsistencies were corrected by fixing the filing, the US GAAP XBRL Taxonomy, or the business rules; then the XBRL-based financial information would have zero defects as articulated by the business rules. While the rules I have provided are necessary (i.e. they are fundamental relationships) those rules are not sufficient. I have already pointed out that the disclosure mechanics rules also need to be passed.

The point is this: there is a self-evident connection between "quality" and "business rules". All you need to do is read the document which summarizes the remaining issues of the quality leaders and you cannot help to see this important connection.

How hard is it to fix mistakes? If you go back and look at prior testing results you would see that EDGARfilings PROfile went from 76% consistency in March 31, 2016 to 98% consistency in November 27, 2016. This graphic shows their improvement in quality. Merrill went from 55% consistency in March 31, 2015 to 97% consistency in March 31, 2016. Here is Merrill's graphic. Fixing mistakes just takes effort. Good tools can help too.

Here is the summary of consistency with the fundamental accounting concept relations business rules as of November 27, 2016:

(Click image for larger view)

(Click image for larger view)

Nice work to the quality leaders who have worked so hard to dial in their XBRL-based digital financial reports! Collectively, the 9 quality leaders have reached Sigma Level 4 and I expect them to reach Sigma Level 5 within the next three months. You quality laggards need to get to work fixing your mistakes.

* * * PRIOR RESULTS * * *

Previous fundamental accounting concept relations consistency results reported: August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

Charlie

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments