BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from January 1, 2017 - January 31, 2017

Understanding that XBRL is a Knowledge Media

Most people think about XBRL in terms of what it is. Using that definition, XBRL is a global technical syntax for exchanging information. Another way of looking at XBRL is in terms of the value it provides. Using that definition, XBRL imparts knowledge. XBRL is a new medium. XBRL is a high-fidelity knowledge media.

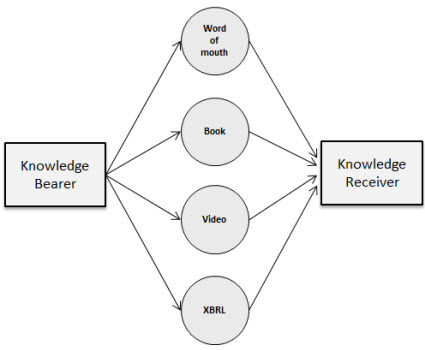

In his book, Systematic Introduction to Expert Systems, Frank Puppe discusses the notion of knowledge media. This figure, a modified version inspired by Frank Puppe's Figure 3.2, shows some knowledge media in order to contrast some specific advantages and disadvantages of the different media. This will help you see the value of the XBRL knowledge media:

Inspired by Frank Puppe's Figure 3.2, page 21.

Inspired by Frank Puppe's Figure 3.2, page 21.

The graphic shows a knowledge bearer on the left which imparts some knowledge to a knowledge receiver on the right via some knowledge media. Just a few knowledge media are shown. Here is a summary of some of the advantages and disadvantages of the list of knowledge media which are shown in the graphic above:

- Direct contact between knowledge bearer and knowledge receiver: With some media you need direct contact between the bearer and receiver of knowledge. For example, with Word of mouth you generally need direct contact. With a Book, a Video, or XBRL you don't need direct contact.

- User control over information access: Word of mouth, Book, and Video all tend to be sequential access to the information. You tend to receive information in a specific order. With XBRL, it is easy to reorder or reconfigure information. The user can easily control of the order of information access.

- Verifiability of information: Verifying the information you receive is possible using any media. However, because XBRL is machine-readable; automated testing can be used to verify information and experimentation is easy. For example, I can test the complete set of XBRL-based public company financial filings using software in a matter of a few hours. Word of mouth, Book, and Video media is not machine-readable.

- Testing information ambiguity: Because XBRL is machine-readable in terms of meaning but Word of mouth is not machine-readable and Book and Video are not machine-readable in terms of meaning; XBRL can be used to measure the ambiguity of information conveyed. The effects of vagueness and poorly articulated information can be made very clear using testing, and so such ambiguity can be minimized between the knowledge receiver and knowledge bearer.

- Information fidelity: Fidelity is the degree of exactness with which something is copied or reproduced. With Word of mouth the fidelity tends to be maximized because the bearer and receiver are communicating directly. If there are issues in understanding, questions can be asked. With a Book or Video, there tends to be a bit less fidelity perhaps. With XBRL, because information is converted from what is more an analog (paper) to a digital representation, their might be a loss of fidelity if the digitization is not done well. It is sort of like the difference between a record which is analog, a CD which is digital format, and a MP3 which is compressed digital format. The price you pay for the smaller MP3 files is lost fidelity, but what is lost is the frequencies far beyond a human's ability to hear. Everything is a tradeoff.

- Reach versus richness: In their book Blown to Bits, Philip Evans and Thomas S. Wurster point out the new economics of information. In the past, you could have reach or richness, but typically not both at the same time. The internet completely changed this economic equation. Reach is access to information. Richness to quantity, timeliness, accuracy and variety of information. Word of mouth tends to be the richest information, but the reach can be lower. Books have excellent reach, but less richness. With XBRL you can have excellent reach and richness.

However, in order to make use of a knowledge media effectively, the following three conditions must be satisfied:

- Easy for knowledge bearer to represent information: The effort and difficulty required for the knowledge bearer to successfully formulate the knowledge in the medium must be as low as possible.

- Clear, consistent meaning: The meaning conveyed by the knowledge bearer to the knowledge receiver must be clear and easily followed by human beings and be consistent between different software applications. The result cannot be a "black box" or a guessing game and users of the information should not be able to derive different knowledge simply by using a different software application.

- High-quality information representation: The form in which the knowledge is represented to the receiver must be as good as possible. The quality must be high whether the knowledge receiver is a human-being or an automated machine-based process. Sigma level 6 is a good benchmark, 99.99966% accuracy.

The knowledge conveyed by a zero defect intelligent XBRL-based digital financial report as to the financial condition and financial position of an economic entity is just an example of the capabilities of the XBRL knowledge media. Digital business reports of other sorts are possible also. Think semantic spreadsheets. See here and here.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Clear Vision of Intelligent XBRL-based Digital Financial Reporting Tool

If I had a tool for creating zero defect (sigma level 6 quality) US GAAP and/or IFRS general purpose financial reports leveraging intelligent XBRL-based structured information and I could create those reports faster than you can create financial reports today, incurring less costs than you incur today, and with a higher quality level than the financial reports that you create today; then would you buy that tool?

What if the tool had all the necessary pieces, it was complete. What if the tool was easy to use. What if the tool was inexpensive.

Do you know how to build such a tool? Do you know the proper technologies to employ to create the tool? If you are a business professional, do you understand how to specify such a tool?

Leap frog the competition: Intelligent XBRL-based Digital Financial Reporting

No magic. Skillful execution. Attention to detail. Quality of a master craftsmen. Engineering excellence. Steve Jobs would be happy.

Purpose-build for disclosure management and financial report creation, intelligent XBRL-based digital financial reporting products collect information about financial report creation projects and allow this information to be coordinated across all other representations of the project, so that every statement, policy, and disclosure is based on internally consistent and complete information from the same underling financial information database. Risk of noncompliance is minimized. Cost of compliance is minimized. Effort to comply is minimized.

All the information provided by this resource is released into the public domain. Two key pieces of the resource are a summary of the background information necessary to understand the problem correctly and a conceptual model that pushes the technical aspects into the background, freeing professional accountants from technical details so they can focus on the accounting and reporting.

Next step? Turn the vision into a reality. Stay tuned.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

XBRL Open Information Model 1.0

XBRL International has published a candidate recommendation for the XBRL Open Information Model (OIM) 1.0. XBRL International defines OIM as follows:

The Open Information Model provides a syntax-independent model for XBRL data, allowing reliable transformation of XBRL data into other representations.

My personal view here is that this is a good step in the right direction, but there is not really anything that is "XBRL data". XBRL is a technical syntax. There is "financial data" and there is "nonfinancial data" and either of those types of data, or information really, can be represented using the XBRL technical syntax.

What is still missing is a global standard conceptual model for business information, including financial information. Until that global standard model exists, here is the conceptual model that I am using. I arrived at that by reverse-engineering XBRL-based public company financial reports which were submitted to the SEC.

My conceptual model has a significantly deeper level of meaning than is provided by the XBRL International OIM.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

An Open Letter to President-elect Donald J. Trump on Financial Reform

Financial InterGroup wrote an An Open Letter to President-elect Donald J. Trump on Financial Reform and a research paper Trumpeting in the New Era of a Lean Technology-Driven Financial System". Seems like the proposal is to create something similar to Dwight D. Eisenhower's Interstate Highway System for the U.S. and global finance system.

I agree with this vision and I believe that Near Zero Defect XBRL-based Financial Reports and Intelligent XBRL-based Digital Financial Reporting can play a major role in turning that vision into reality.

Here are a few excerpts from the open letter and the research paper:

"This is a call to President-elect Trump, an acknowledged master builder, as he ushers in the lean era of financial regulation. We encourage him to establish a new executive-level office to inform his administration on how to rebuild an essential infrastructure component of our economy - the financial system and its regulatory apparatus, on the road to lean, transparent technology driven regulation."

"It's incredulous to many inside the financial industry and truly amazing to those in other industries that after six decades of automation of financial transactions there are no global standards for the identity of financial market participants nor their financial products. Imagine if every supermarket had a different barcode for the same product on its shelves or a different code for the producer or supplier of the product. Walmart, FedEx and Amazon could not exist. Imagine a shopper buying groceries and being asked to return three days later to pick it up. This is the current state of finance, no standards and waiting days to own financial products bought days before."

"The Office of Financial and Regulatory Technology (the OFRT) is to be a new executive branch agency, a research and standards setting body. It would be the center of research and innovation to evaluate new technologies and build links between evolving technologies and new regulations. It would enable more effective and transparent oversight of financial institutions, amongst financial regulators, and between the two in a digitized financial and regulatory environment. It would also enable less regulators and less third-party data and infrastructure intermediaries."

"The OFRT would follow in the footsteps of the U.S. Department of Defense's Advanced Research Projects Agency, the 1960's era government agency responsible for creating a packet switching time-sharing network of computers known as ARPANET, the precursor to today's Internet and World Wide Web. A similar ground breaking technology, distributed ledger technology (DLT) has entered the world of finance. DLT is an outgrowth of the Blockchain. Both were developed to support the digital cryptocurrency Bitcoin. DLT works like a huge, decentralized ledger which records every transaction and stores this information on a global network to prevent tampering. It needs standards and a center of gravity, much like the ARPANET provided for the Internet."

This is a great opportunity for the United States! Here is how to make it work.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Intelligent XBRL-based Digital Financial Reports

Today's software for creating XBRL-based digital financial reports is off target. Software engineers/developers/vendors need to be nudged in the right direction by business professionals. But first, business professionals need to learn what to ask for.

CAD/CAM software which is used to create "digital blueprints" offers good lessons for professional accountants and other business professionals. Contrasting how digital blueprints are created to how digital financial reports can be created helps to communicate the vision of what an intelligent XBRL-based digital financial report is.

I found three videos related to CAD/CAM that run a total of about 25 minutes which helps communicate the vision. Any business professional can understand this information. In those 25 minutes, if you have only a little imagination you can grasp the parallels between what has happened to the blueprint and draftsmen, architects, and engineers; and what is happening to accountants, auditors, and analysts.

When you watch these three videos, think of the following: Near zero defect intelligent XBRL-based digital financial report:

Purpose-build for disclosure management and financial report creation, intelligent XBRL-based digital financial reporting products collect information about financial report creation projects and allow this information to be coordinated across all other representations of the project, so that every statement, policy, and disclosure is based on internally consistent and complete information from the same underling financial information database.

Here are the three videos:

- The Difference between traditional CAD and BIM: (11 minutes) The really good part starts at 3:52 where the narrator explains that you "draw with walls, doors, and windows" rather than with lines and circles like in AutoCAD.

- Revit 2017 - Tutorial for Beginners: (13 minutes) This video simply provides additional, but very good, details which expands the ideas shown in the first video. Shows how Revit lets you work with walls, doors, windows, roofs, ceilings, floors and so forth. Imagine an intelligent financial reporting tool that lets you work with statements, disclosures, policies, roll ups, roll forwards, etc. Think intelligent spreadsheets.

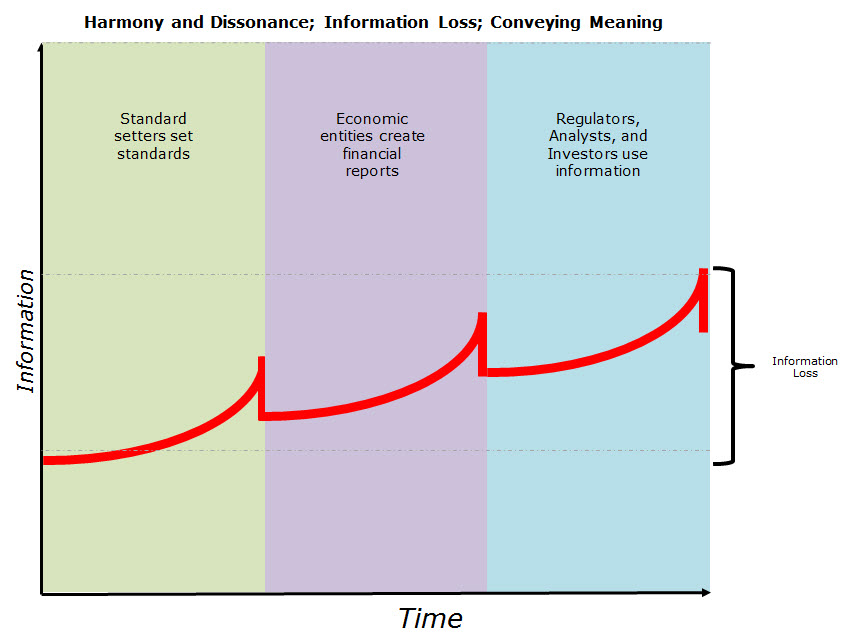

- The Evolution of Drafting: (9 minutes) While the entire video is good to watch, the three graphics which show relating to "no need for interpretation" and "information lost over time" make a major point: Information lost over time: Design phase, Construction phase, Facilities management phase; a similar situation exists with financial reporting

Using the "information loss over time" idea from the third video and combining that idea with the notion of "harmony" as contrast to dissonance from the SWIFT Institute paper, I created the following graphic which shows information loss between standards setters, economic entities which create financial reports using those standards, and then regulators, investors, and analysts who use that information. This is what I came up with:

(Click image for larger view)

(Click image for larger view)

I don't know that I have the graphic totally right, but I do believe it helps make the point about information loss and how intelligent XBRL-based digital financial reporting helps to minimize information loss by improving communications.

Do you have a better graphic to communicate this notion? Let me know.

What is necessary is a tool purpose-built for creating financial reports? The user is never exposed to the XBRL-technical syntax, or anything "technical" that relates to computers. The "technical" that they work with relate to accounting and financial reporting. How to you create such a tool? Read this. That information helps you hone your skills.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print