BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from July 1, 2018 - July 31, 2018

Leveraging Poka-yoke to Build Better Software

Poka-yoke (not to be confused with the Hawaiian raw fish salad, poke) is a technique used to prevent mistakes through smarter design. Poka-yoke is a Japanese term that means "mistake-proofing". A poka-yoke is any mechanism consciously added to a process that helps an equipment operator avoid mistakes. Its purpose is to eliminate defects by preventing, correcting, or drawing attention to human errors as the errors occur.

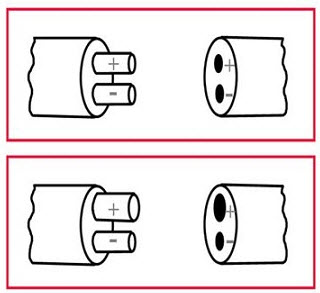

For example, consider the graphic below. You want someone to plug the plug into the receptacle such that positive and negative of the plug and receptacle match up. Inadvertently reversing this would have catastrophic consequences. In the top part of the graphic notice that it is possible to make a mistake but in the bottom part of the graphic a mistake would be impossible because of the size differences in the positive and negative receptacle and plug.

(Image from Process Exam, Six Sigma Tools - Poka-yoke)

(Image from Process Exam, Six Sigma Tools - Poka-yoke)

Poka-yoke is a Lean Six Sigma technique. You can use techniques such as this to build better software. My MBA is in these sorts of quality control techniques. At the time these were called "World Class Manufacturing Techniques". Today people call these techniques "Lean" or "Six Sigma" or "Lean Six Sigma". While Lean Six Sigma was developed by the manufacturing sector, these techniques are applicable to literally any system.

In the document Putting the Expertise into XBRL-based Knowledge Based Systems for Creating Financial Reports, Hamed Mousavi and I explain how we are leveraging things like poka-yoke, patterns, compound objects, and other techniques to create an expert system for creating financial reports. That software we are creating is part of the modern finance platform which, we believe, will replace the old school approaches for creating financial reports.

If you read the document Computer Empathy you will recognize how dumb computers are but also what it takes to get computers to reliably perform work for you.

An expert system for creating financial reports is a pretty novel idea, I believe. Time will tell if we can make this work. There is a tremendous amount of complexity that is required to be coordinated to pull this off appropriately. We believe that the modern finance platform will not only disrupt, but will significantly transform accounting, reporting, auditing, and analysis. Time will tell whether we are right or whether we are wrong.

Some people (ok...well, at least one person) call accounting "history's sexiest subject". I don't really know if it is sexy, but it is certainly interesting. Digital distributed ledgers, triple-entry accounting, artificial intelligence, digital financial reports; what a great time to be an accountant if you understand what is going on.

Don't quite understand? Well, start by reading Computer Empathy. Don't be sold a bill of goods by the snake oil salesmen!

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

2 References

|

2 References

|  Email

|

Email

|  Print

Print

The Modern Finance Platform

I mentioned that old school financial report creation processes can be inefficient and error prone and that these processes should be change. But how should these processes be changed?

BlackLine has one of the best explanations of what the modern finance platform will look like. BlackLine uses the term "smart close". Their smart close appears to be SAP specific. Here is BlackLine's description:

The Modern Finance Platform

BlackLine builds solutions that modernize the finance and accounting function to empower greater productivity and detect accounting errors before they become problems. BlackLine products work in unison to eliminate manual spreadsheet-dependent processes prone to human error. BlackLine Account Reconciliations automates and standardizes the reconciliation process, and natively integrates with other BlackLine products to help manage every element of reconciliations and the financial close. Streamlining account reconciliations helps ensure accurate and efficient accounting activities, free from manual, error-prone practices. BlackLine is the only provider that offers a unified cloud platform supporting the entire close-to-disclose process and the leader in Enhanced Finance Controls and Automation software. BlackLine enables clients to move away from out-of-date practices and help finance and accounting professionals work smarter, more efficiently, and accurately. Clients around the world use BlackLine. BlackLine’s cloud platform unifies the experience of more than 196,000+ people around the world as they accurately, securely, and efficiently execute critical accounting tasks from reconciliations and journals to intercompany settlement and the financial close.

As I menstioned in the document Computer Empathy, more tasks of both the internal and external financial report creation processes will be automated. Rather than humans doing all the work, teams of humans assisted by machines (i.e. software) will collaborate to create financial reports. Humans will focus on the sorts of things they do best; machines will focus on the sorts of things they do best.

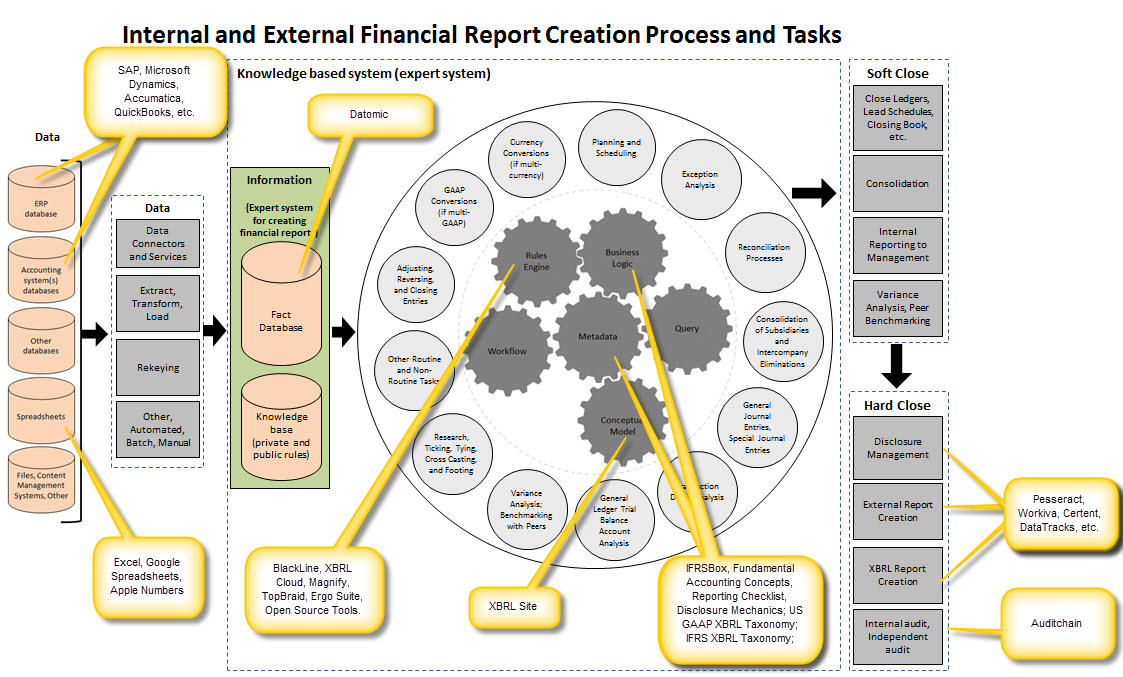

So, what is the process? What are the tasks that need to be performed? What software is available? I have been nuturing this graphic along for about six months which tries to explain the tasks within the process of creating a financial report. Here is that graphic (click image for a larger view):

(Click image for larger view)

(Click image for larger view)

If you think about how you might implement accounting process automation one of the first things you will realize is that you have to use some sort of technical syntax in these processes. XBRL is an excellent choice. I show you how you can do this in my Guide to Implementing Robotic Finance. Now, XBRL is not the only choice. The semantic web stack is a viable alternative. You do need some sort of a logic framework.

To be honest, I do not clearly understand the pros and cons of the semantic web stack as contrast to the XBRL stack. Frankly, I really don't think it matters which technical stack you choose. The power of the logic framework does matter. The more powerful the logic, the more work that can be automated.

Don't understand all of this? You are not alone. Many business professionals need to enhance their digital skills. What the heck is a digital mirror world? And what is triple-entry accounting? Or, digital distributed ledgers? What are the risks of artificial intelligence? It does not seem that artificial intelligence is working for self-driving cars; why should we believe it will work for finanancial reporting?

These are all excellent questions. And all of these questions have answers.

Accounting, reporting, auditing, and analysis in a digital environment will be here sooner than you might think! Don't be an information barbarian. The quality standards of financial reporting are extremely high. Software vendors that cannot maintain quality will not succeed. Low quality is simply a non-starter.

How do you build a modern finance platform? This document General Ledger Trial Balance to External Financial Report helps you understand the pieces of that puzzle.

Stay tuned for more information.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

1 Reference

| Email

| Print

Updated List of IFRS Filings

I have updated my set of IFRS-based financial reports that have been submitted to the SEC. I am using these filings to create IFRS metadata including the reporting styles. Here is a list of what I have:

- Human readable list of the now 406 IFRS filings.

- Machine readable RSS feed of those same 406 IFRS filings.

- IFRS Reporting Styles Analysis.

- ZIP archive containing Excel spreadsheets that prove the reporting styles.

- List of the current reporting styles. (Details)

- IFRS Reporting Styles Summary. (Overview)

- List of manually organized and classified statements and disclosures.

- ZIP archive with XBRL taxonomy model structure and roll up relations.

- ZIP archive of XBRL instances.

- Roll up query tool. (New, work in progress)

- Roll up query tool linked to reporting style mappings. (New, work in progress)

- Analysis of errors in one reporting style

Basically, I added about 90 form 40-F filings that use IFRS of Canadian companies. Stay tuned! More to come.

Here are some updates to the reporting styles:

- This summary and detailed information is the most current.

- Those reporting style rules (#1) are 100% synchronized between XBRL Cloud, Pesseract, and the Excel versions and tested to be sure they are consistent.

- This set of Excel spreadsheets in the ZIP file have the rules for the classified balance sheet (BSC), typical cash flow statement (CF1), and the most common income statement (SPEC6).

- I made most of the adjustments requested by others:

- Commitments and contingencies was REMOVED from all balance sheets.

- Temporary equity was REMOVED from all balance sheets.

- Many of the codes such as BSC, BSU, SPEC6, CF1 are now included in the XBRL taxonomy and related documentation.

- I removed the network and rules related to Preferred Stock Dividends and Other Adjustments, and Net Income (Loss) available to Common that are not applicable to IFRS.

- I removed other stuff associated with US GAAP that is not applicable to IFRS

- I fixed the issue related to the Revenues concepts being in the wrong order.

- I fixed the issue related to "ifrs-full:OperatingExpense".

- I added the 2018 IFRS taxonomy.

- I had two separate creation tools for the "controlled natural language" format and the "XBRL Formula" XPath 2.0 rules format. Now this is ONE tool. (i.e. doing things now takes half the time).

- Here are all the rules I currently have in both XBRL Formula (XPath 2.0) format and the Controlled Natural Language (i.e. Excel-ish type) format: (note the LINKS to the actual XBRL Formulas)

- Here are all the networks.

- Here are all the fundamental accounting concepts.

- Here are the mappings.

- Here are the fundamental accounting concept relations in presentation form.

- And here is the PROOF that all this works (I will update this empirical evidence of actual filings as I add new reporting styles)

Like I said, stay tuned. If you don't understand why I am doing all this, you may want to consider reading this document.

Charlie

in Becoming an XBRL Master Craftsman, Creating Investor Friendly SEC XBRL Filings, Digital Financial Reporting

|

Post a Comment

| Email

| Print

Enhancing your Digital Skills

Professional accountants and other business leaders will need to enhance their "digital skills" in order to be efficient at accounting, reporting, auditing, and analysis in a digital environment.

Allan Grody, in his article, Banking could use more leaders with STEM skills, points out the importance for those in leadership positions to become conversant in the important details about the technologies they will inevitably employ:

"It's important that those at the front end of this information - legislators, regulators and financial executives - become conversant in these skills, lest the back-end stumbles over meaning and intent and, in some cases, declares it impossible to be implemented."

While those in leadership positions don't need to have a deep understanding of math or computer programming; they do need to have the capacity to ask good probing questions and be able to have a meaningful conversation about the digital construction materials those that they lead are working with. Leaders should be able to question and challenge how their direct reports are overseeing the implementation digital tools that will be used to perform work using algorithms, metadata, conceptual models, and other tools, techniques, and processes.

Don't be an information barbarian. Leaders have a responsibility to acquire these "digital skills" that allow them to understand how accounting, reporting, auditing, and analysis work in the digital age; ultimately your industry or your customers hold leaders to a higher standard.

But what skills do you need?

STEM (science, technology, engineering, and math) is a very general description. "Learn to code" is a hysteria, which likewise is a very general description and it is simply misguided to think that everyone should be a programmer. Simply understanding "technology" is too broad and general to be helpful.

Understanding the specifics of how computers work will help you understand how to employ these very useful tools for your work. The document Computer Empathy strives to provide you with very specific details of what you need to learn with enough information to help you understand why you should learn it. That document should provide you with a good theory, framework , and principles to help you not only survive, but to thrive in a digital environment.

ESMA Field Test Information, Great Information for Testing

I mentioned in another postthe field test of the ESEF (European Single Electronic Format). Here is some additional information.

This is the set of 22 companies that participated in the ESEF field test. I created an RSS feed for these 22 companies. Not sure why the ESMA did not do that, it is kind of standard practice to provide a machine-readable version of the set of filings.

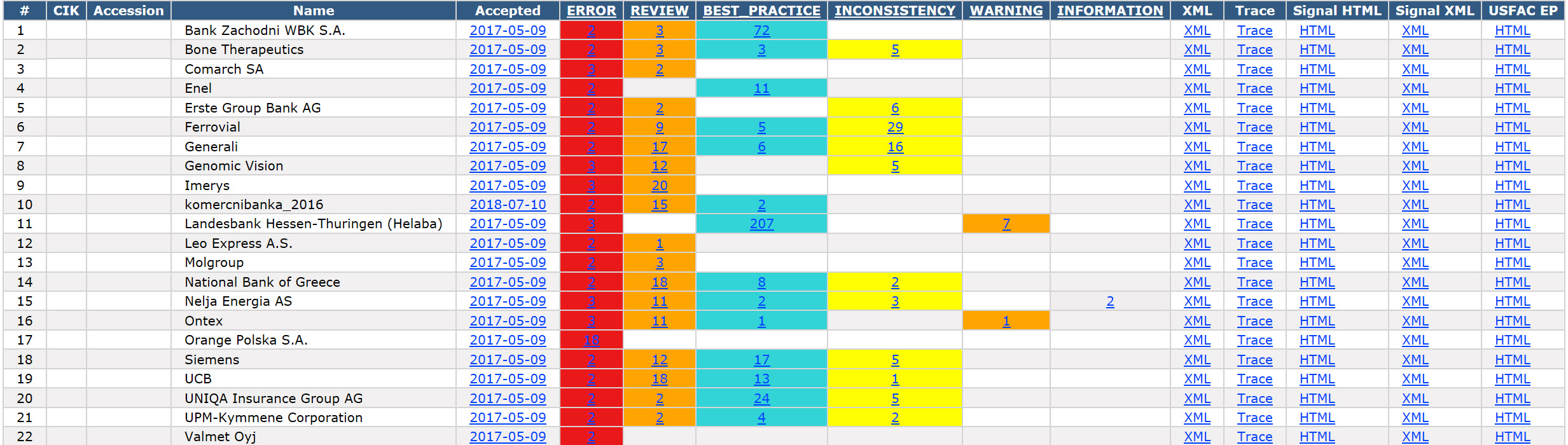

I ran all 22 of these filings through validation using XBRL Cloud and the following are the validation results:

By ESMA filer:

(Click image for larger view)

(Click image for larger view)

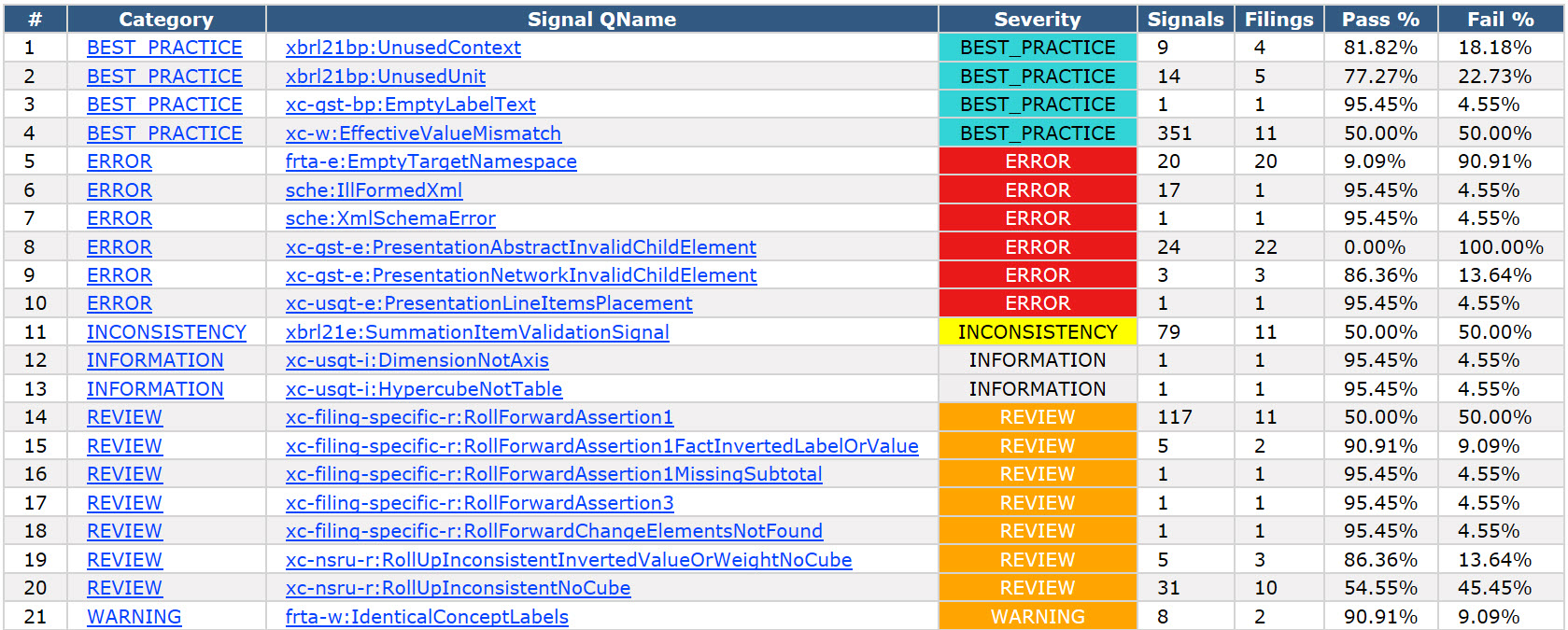

By Error/Inconsistency message:

(Click image for larger view)

(Click image for larger view)

There are a lot of errors, but the vast majority of errors fall into one category which is called "InvalidXhtmlBodyContent". Basically, the filer is not representing their [Text Block]s correctly, violating the Inline XBRL specification. One of the filings would not even load, I am pretty sure that filing was violating the Taxonomy Package Specification which dictates how the ZIP archive is formatted. Could be wrong about that, still trying to figure that out but that is what I speculate is going on.

So, these 22 filings add to my set of IFRS filings that I am testing. I am creating the fundamental accounting concept relations continuity cross check validation for IFRS with the help of a handful of other accountants. I am also working on validating the disclosures. I have the framework all up and running, I just need to create more metadata to match what I have for US GAAP.

If you are still trying to understand why I am going through all this effort, read this document.

Just for the heck of it I tried to create an XBRL instance using the Taxonomy Package ZIP format. Here it is. It worked!

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print