BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from October 1, 2017 - October 31, 2017

WIRED: Data is the New Oil of the Digital Economy

In his WIRED article Data is the New Oil of the Digital Economy, Joris Toonders points out the value of data in today's digital age for those that learn to extract and harvest that data. But there is one thing that is even more valuable than data. Metadata.

Fortune has a similar article, Data is the New Oil, by Jonathan Vanian. The tag line of that article is, "Artificial intelligence is only as good as the data it crunches."

While it is true that data is important; metadata is even more important. The key ingredient in a knowledge based system is domain knowledge. Metadata organizes domain knowledge.

What is not in dispute is the need for a "thick metadata layer" and the benefits of that metadata in terms of getting a computer to be able to perform useful and meaningful work. This is simply science.

But what is sometimes disputed, it seems, is how to most effectively and efficiently aquire that thick metadata layer. There are two basic approaches to getting this metadata layer:

- Have the computer figure out what the metadata is: This approach uses artificial intelligence, machine learning, and other high-tech approaches to detecting patterns and figuring out the metadata.

- Tell the computer what the metadata is: This approach leverages business domain experts and knowledge engineers to piece together the metadata so that the metadata becomes available.

And this is not an "either/or" question. Both automated and manual knowledge acquisition methods can be used combined into a hybrid approach to aquiring knowledge. The question is how to best combined the two approaches to most effectively and efficiently get the important metadata you need.

Because knowledge acquisition can be slow and tedious, much of the future of artificial intelligence and expert systems depends on breaking the knowledge acquisition bottleneck and in codifying and representing a large knowledge infrastructure using automation. But, domain professionals are still going to need to participate. And to participate, they need to understand knowledge and knowledge science.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Hashgraph: An Alternative to Blockchain for Distributed Ledgers?

I thought that blockchain was the only way to build distributed ledgers. Seems like there is a new technology: hashgraph. This article, Blockchain Just Became Obsolete: the Future is Hashgraph, helps you understand the difference between blockchain and hashgraph. In particular, this 10 minute video is very helpful.

Remember that a distributed ledgar is an application or a use case. Blockchain and hashgraph are technologies that are used to implement distributed ledgers.

Charlie

in Distributed Ledgers

|

Post a Comment

| Email

| Print

Conceptual Legos and the Universe of Discourse

A significant problem that professional accountants have with XBRL is that they don't understand the moving pieces of the conceptual model, the "Conceptual Legos" that make up the pieces of an XBRL-based digital financial report.

If you don't understand the higher-level conceptual model then the model is defined in solely syntactic terms and as such do not have any meaning until they are given some interpretation. That interpretation is the semantics of the model.

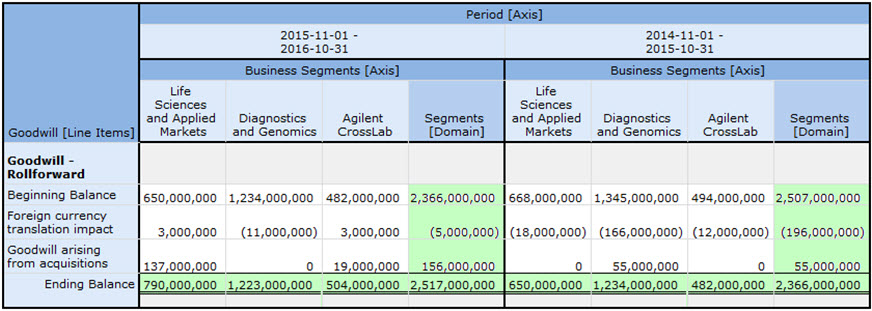

How hard is it for you to interpret the information in the graphic below? (Click the image, and a larger view will be provided.) It is probably pretty easy for either accountants or even non-accountants to interpret that information. That graphic is driven by 100% pure XBRL. Now, the application processing the information is driven by some additional information about business reports, the multidimensional model. That helps software render the information. The multidimensional model provides information that gets things into the right rows, columns, and cells.

(Click image for larger view)

(Click image for larger view)

Now, the report fragment above happens to be a disclosure of the goodwill roll forward, the changes in goodwill from each balance sheet beginning balance to each ending balance.

Not surprisingly, reports contain lots of report fragments. Those report fragments represent lots of different disclosures. Many of those disclosures are roll forwards. Others are roll ups. I gave the terms "roll forward" and "roll up" and similar patterns in the organization of reported disclosures a name; I call them concept arrangement patterns.

If you scan this document that contains descriptions of about 65 or so financial disclosures, you will see lots of different roll forwards, roll ups, and other concept arrangement patterns. If you look at each of those disclosures and the one shown above, you see cells colored GREEN which represents a mathematical computation. Every roll forward actually mathematically rolls forward. That is shown be the GREEN cells in the last row of that disclosure. This particular roll forward also cross-casts shown by the other GREEN cells. I gave this cross-cast a name also, I call it a member arrangement pattern.

I documented all these terms that I refer to in this Introduction to the Conceptual Model of a Digital Financial Report.

A Universe of Discourse is the set of all things under consideration during a discussion, examination, or study.

A universe of discourse is also the set of all objects or entities that is defined by a conceptual model. XBRL-based digital financial reporting is NOT "conceptually promiscuous"; you simply cannot just add new pieces to the conceptual model. Now, don't get confused here. The conceptual model is the shape of the information you put into the model. Remember, the same XBRL technical syntax can be used to define both US GAAP and IFRS financial reporting schemes. US GAAP and/or IFRS concepts (and other stuff) is what goes INTO the conceptual model. US GAAP and IFRS share the same business report and financial report conceptual model.

Now, you don't want all this to be a mess and you want a consistent interpretation of the conceptual model, so you define rules. Why? Because rules prevent anarchy. See XBRL-based digital financial reporting principle #3: "Anarchy is defined as 'a situation of confusion and wild behavior in which the people in a country, group, organization, etc., are not controlled by rules or laws.' Rules prevent anarchy."

Rules assert knowledge. For example, "Assets = Liabilities and Equity" (i.e. the accounting equation) is both a rule and knowledge. Constraints are restrictions on existing knowledge. Constraints can be used to detect incomplete information. Constraints can be used to check knowledge for inconsistencies and contradictions. Rules all follow the same rules of logic.

The rules of logic are a common denominator for a universe of discourse, or sometimes referred to as a domain. Business professionals interact with the conceptual model using the semantic level of these "Conceptual Legos" logical pieces software applications expose that are understandable by the user of the software system. Business professionals don't interact with the technical syntax.

The system is not a "black box", rather the system is transparent do that the business professional using the system and understands what the system is doing.

Digital financial reporting requires that every business user of the system share the same universe of discourse, the same fundamental conceptual model, and the same logical rules. The goal is that every interpretation of the conceptual model is consistent with the intended interpretation of the conceptual model. The conceptual model is formal, the conceptual model is definable, and the conceptual model has a finite set of shapes.

When a software developer puts all these pieces together correctly, what do you get? You get easy to use software and zero defect digital financial reports. Software is easy to use because it is simple. Not simplistic, simple. Simple means you work hard to keep complexity to a minimum. See the Law of Conservation of Complexity. Reports don't have defects because humans augmented by machines that leverage rules watch over the creation of the report.

Here is an example of such software. That is just a robust proof of concept to test all these ideas. More software is on the way!

Pretty good stuff, huh! Well, I cannot take any credit for it. These ideas come from Blockly which came from Scratch. I am simply applying those ideas to financial reports.

JOA: Accountants’ role in managing AI disruption

The Journal of Accountancy published an article, Accountants role in managing AI disruption, pointing out some short-term (20 to 30 years) and longer-term (50 to 70 years) impacts that artificial intelligence (AI) will have on society. You can read the article to understand those changes.

More importantly, Calum Chace, an AI expert, makes the following statement in the article, "Accountants can play a leading role in the dialogue about the future. He said accountants are trusted for their intelligence, level-headedness, and analytical abilities, and he expects that as AI's impact on the world emerges, accountants will continue to use their skills to serve the public interest."

I agree. But first, accountants need to understand AI and its probable impact.

Chace says that at a more immediate level, accountants need to know how to handle the disruption that AI is bringing to their profession in the very short term. (i.e. now) Three immediate steps include:

- Start slowly; this will be baby steps for most companies

- Make use of your data

- Find the necessary skills

Here is a baby step where you can use your data and determine if you have the skills you need or if it is necessary to bring in additional skills: XBRL-based digital financial reporting.

The document that I put together, Getting Ready for the Digital Age of Accounting, Reporting and Auditing: a Guide for Professional Accountants, is helpful to professional accountants trying to get their heads around things like AI. One of the first applications of AI in accounting and reporting will be XBRL-based digital financial reporting.

Rudimentary AI is already here. How do I know? Because I helped to create it. I would not go as far as saying that I wrote the book on the use of AI in financial reporting; but I will say two things:

- I put together about 750 pages worth of good information over the past 15 years.

- If you know of something better, please tell me about it. I would really like to know about it.

Because most professional accountants did not get basic background information in college or pick up the necessary information over their careers, it is very important to start at the foundational level, get a good grounding. What I found useful is all organized in Part 1 - Foundation for Understanding: Background, Framework, Theory, Principles.

If you don't lay a good foundation, you will fall prey to the snake-oil salesmen. Don't fall into that trap.

MORE INFORMATION:

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Campaign to Improve Disclosure Quality of XBRL-based Public Company Financial Reports Submitted to the SEC

I am leveraging the success of my informal campaign to improve the high-level fundamental accounting concept relations of XBRL-based financial filings submitted by public companies to the SEC. I am starting a new informal campaign to improve the quality of disclosures. This is a great learning opportunity.

Between March 2015 and August 2017 filing agents and software vendors were able to reduce the number of errors related to the reporting of basic, fundamental high-level accounting concepts in XBRL-based financial reports from approximately 4,463 to 1,059.

These errors related to reporting high-level facts such as Assets, Liabilities and Equity, Revenues, Net Income (Loss); about 75 or so facts on average. During that period, there were four filing agents/software vendors which had tuned their processes to deliver 99% or better consistency with my basic set of business rules that uses automated processes to detect logical, mathematical, consistency, and continuity related issues within and between these high-level fundamental accounting concepts.

The errors I detected are generally not disputed because they relate to logical and mathematical relations between concept defined by US GAAP, evidence exists within public company financial reports of these relationships, about 99.02% of the actual reported facts within XBRL-based reports are consistent with and therefore support the machine-readable business rules used in my processes, and 88.2% of public companies are consistent with and support all of the business rules used to evaluate reports.

All of this information is publically available on my blog. Anyone can verify or dispute issues by simply looking at any XBRL-based financial report of a public company. I have created summaries that professional accountants can use to examine and understand these errors.

The most important benefit realized from taking these measurements, building rules, and detecting these errors is an excellent understanding of XBRL-based financial reports and what makes them work. Currently, the best understanding of these reports seems to exist within the processes and procedures of four institutions that have been able to create repeatable, reliable processes of creating financial reports that are 99% or higher in consistency with these fundamental accounting concept relations:

- Merrill

- RDG Filings (Thunderdome software)

- Donnelley Financial Solutions

- DataTracks

There are several other software vendors/filing agents that are closing in on repeatable processes that yield high-quality results. How to build repeatable processes that yield high-quality results can be learned.

Building on what I have learned from the measurement of the fundamental accounting concept relations; I am embarking on the next step in my systematic, methodical, deliberate, rigorous journey to understand and be able to create high-quality XBRL-based financial reports: the disclosures.

A grass-roots, market-driven, informal effort to improve the quality of about 65 specific disclosures in the 10-K financial reports of public companies which are submitted to the SEC in the XBRL format will take place during this years "10-K filing season" during December 2017, January 2018, February 2018 and March 2018.

A few software vendors/filing agents already have a jump on others and are improving 10-Ks which will be filed during Q4 of 2017.

What I am trying to do is disseminate information to as many professional accountants, particularly certified public accountants, as possible so that they can better understand the subtleties and nuances of XBRL-based financial reports. This will help the institution of accountancy leverage this useful tool which the SEC has helped to create and is helping to make a real, reliable, working, knowledge media. Analysts also need to understand the subtleties and nuances of such reports. Software engineers creating software need to understand.

The use of this knowledge media will go beyond financial reporting but will be built upon the successful use of XBRL for financial reporting.

Here is information that is helpful in understanding this campaign:

- Summary Information about Campaign: The document Campaign to Improve Disclosure Quality of XBRL-based Public Company Financial Reports Submitted to the SEC summarizes information related to this informal campaign.

- Summary of 65 Disclosures Tested: This is a DRAFT of the disclosures that I will initially target for my campaign. Current measurements show that on average about 85% of these disclosures are consistent with logical, mechanical, structural, and mathematical expectation.

- Details about 65 Disclosures: The document Disclosure Best Practices provides additional details about the 65 targeted disclosures.

- Understanding Business Rules: A big part of this campaign is understanding the role that business rules play in specifying how XBRL-based financial reports should be created. The document Supply Chain Agreeing on Disclosure Business Rules walks you through the process of understanding and revising business rules.

- Creating High Quality Digital Financial Reports: The document Blueprint for Creating Zero Defect XBRL-based Digital Financial Reports helps you understand how to create high quality XBRL-based financial reports.

- Getting ready for the future of financial reporting: The document Getting Ready for the Digital Age of Accounting, Reporting and Auditing: a Guide for Professional Accountants helps you understand that financial reporting will be going through a transformation and helps you understand that you need to get ready for that new paradigm.

- Disclosure Effectiveness: This guide by EY, Disclosure Effectiveness, What companies can do now, provides a helpful framework for thinking about financial report disclosures.

- Commercial Tools Available:

- XBRL US Statement of Cash Flow Guidance

- Disclosures by Topic (Prototype)

This is a HUGE learning opportunity. You will get out of this in proportion to what you put into it. Because Donnelley Financial Solutions, Merrill, RDG Filings and DataTracks did so well to get their filings free from the fundamental accounting concept relations continuity cross check errors, I am very motivated to help them continue on and get their disclosures to the same 99% consistency that they were able to achieve. But, I will help anyone that shows true effort.

What I am doing here in no way takes away from what the XBRL US DSC is doing. It supplements that work. The more rules the better because the more rules, the more than can be automated. The more that can be automated; the more machines can augment human effort…just like a calculator augments a humans capabilities to do math.

If you are unclear where I am going, I would suggest that you read or reread this document: Getting Ready for the Digital Age of Accounting, Reporting and Auditing: a Guide for Professional Accountants.

The enemy is not each other. The enemy is the status quo. If you want to expand your market from the 10,000 public companies that are REQUIRED to use XBRL-based digital financial reporting, to the 26 million private companies in the US that might WANT to leverage XBRL-based digital financial report capabilities; you MUST make it better than the current old school approaches that they use. If XBRL-based reporting does not fundamentally work, that will never happen.

Once the initial batch of 65 disclosures are tuned; I will add the next batch of 500. Then the next batch of 2,000. I really have no idea how many unique disclosures there are, but I will find out. I suspect somewhere between 2,000 and 5,000 perhaps. But between now and March 31, 2018 I will focus on the 65 easy targets.

If you want to join the XBRL-based digital financial report study group, please contact me.

If you want additional information, feel free to contact me. Follow my blog for information flowing from this grass roots campaign.

Analysis summaries:

Charlie

in Becoming an XBRL Master Craftsman, Creating Investor Friendly SEC XBRL Filings

|

Post a Comment

| Email

| Print