BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from October 1, 2019 - October 31, 2019

Enhanced US GAAP Elements of Financial Statements

The FASB provides SFAC 6, Elements of Financial Statements, which instantiates and defines 10 classes of elements that are the building blocks of financial statements. In the FASB's own words:

Elements of financial statements are the building blocks with which financial statements are constructed—the classes of items that financial statements comprise.

Those financial statement element classes are: assets, liabilities, equity, comprehensive income, investments by owners, distributions to owners, revenues, expenses, gains, losses.

I have created an enhanced set of elements of financial statements. This is summarized in my document Enhanced US GAAP Financial Statement Elements. My enhanced set builds on what the FASB does, improving it in three ways:

- Machine-readable: It puts these concepts and their definitions in machine-readable form. The FASB only provides them in e-paper (i.e. PDF). I also provide the information in human-readable form.

- Mathematical associations: It puts the elements in context by showing the associations between the concepts.

- Add useful missing information: It adds additional important concepts that are ultimately defined implicitly or explicitly somewhere by the FASB to provide a complete set of core high-level financial report elements.

Basically, I provide a complete, explicit, and machine-readable foundation which can be built upon and leveraged. Here is the summary in both human-readable and machine-readable form:

- Human readable: (Human | Machine) This is a human-readable version you can browse and get an idea as to what is going on.

- Elements (terms) (Human | Machine): These are the elements of a financial statement.

- Associations (Human | Machine): These are the associations between the elements.

- Assertions (Human | Machine): These are the assertions that show the mathematical relations between the financial statement elements.

- Facts (Human | Machine): This is an instance (i.e. report) that tests the terms, associations, and assertions to both provide clarity and prove that everything is working as expected.

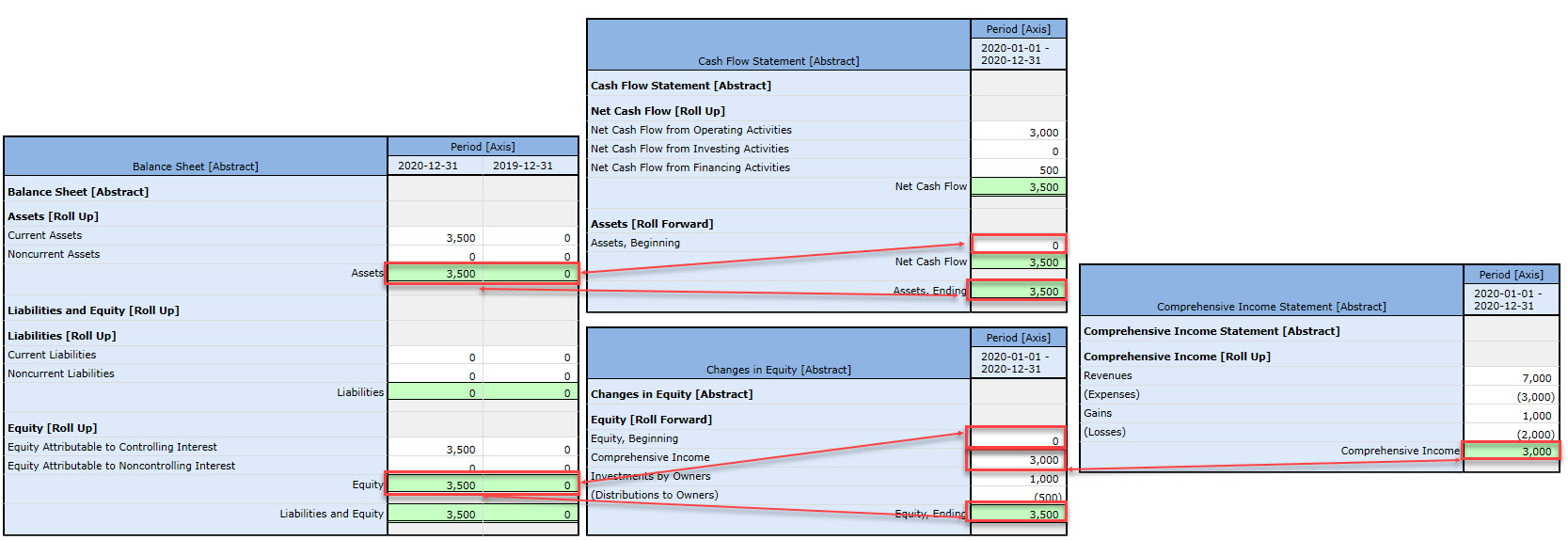

This graphic of the interconnections of the four primary financial statements helps you understand the relationships between the elements.

(Click image for a larger view)

There are a lot of advantages to having this information in machine-readable form. Read the document to understand.

Next up...IFRS, IPSAS, GAS, FRF for SMEs, FAS. Stay tuned! Here is a comparison of the elements of a financial report for a number of financial reporting schemes.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

The AI Ladder

The AI Ladder, by Rob Thomas and published by O'Reilly Media, is by far the best resource that I have run across related to getting your head around artificial intelligence. Here is a summary of why AI projects fail:

- Lack of understanding. 81% of business leaders to not understand AI.

- Bad data. Not having a handle on your data is completely paralyzing. Your AI is only going to be as good as your data.

- Lack of the right skills. The lack of the right skills on part of both business professionals and information technology professionals is problematic.

- Trust. Trusting the recommendations made by your artificial intelligence software is a must. AI should not be a black box, business professionals need justification mechanisms that support conclusions.

- Culture. The Technology Fallacy points out that digital transformation involves changes to organizational dynamics and how work gets done. AI will enable entirely new business models which were impossible in the past.

AI is hard work. Getting AI right involves the right tools, the right skills, and the right mindset. Artificial Intelligence and Knowlege Engineering in a Nutshell can help you navigate AI and help you avoid the snake oil salesment. If you understand AI, then you will likely understand the connection between AI and global standards like XBRL.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Artificial Intelligence Done Right

The Forbes article Demystifying Artificial Intelligence points out that AI is on the minds of 96% of business executives of leading corporations. Another Forbes article, Deep Learning Must Move Beyond Cheap Parlor Tricks, warns that one should avoid creating a fragile house of cards. A third Forbes article, This Week in AI States: Up to 50% Failure Rate in 25% of Enterprises Deploying AI, points out that there is a 50% failure rate in the approximately 25% of organizations implementing AI globally do to lack of skilled staff and unrealistic expectations.

Yet, a PWC study in 2017 points out that:

“Global GDP will be 14% higher in 2030 as a result of AI – the equivalent of an additional $15.7 trillion. This makes it the biggest commercial opportunity in today’s fast changing economy”

AI is hard work as The AI Ladder points out. It requires proper tools, proper methods, and the right mindset.

Here is, in my view, an example of AI done right. A software engineer and I created an extensive working proof of concept of what amounts to an expert system for creating financial reports. If you really want to understand the application, watch the set of videos in this play list.

How did we do it? First, we did not make the "rush to detail" mistake that most people make. We created a solid foundation then we built on top of that foundation. I created a set of principles. With some help I created a theory. We created a model. We put together a framework. We created a method. We did the necessary testing.

All this resulted in our working proof of concept. This document, Guide to Building an Expert System for Creating Financial Reports, helps you to understand important details. While we essentially created a good old fashion expert system, we used the right tool for the job. All this very high-quality metadata will serve as the necessary training data to enable additional functionality using machine learning.

Don't misinterpret what you see. As the Innovator's Dilema points out, "A disruptive product appears as if it's doing everything wrong. Large companies with sophisticated and demanding clients cannot adopt such a technology."

This could be the future of financial reporting. Yes, it has to work well. It can.

A disruption is when new products and services create a new market and significantly weaken, transform or destroy existing product categories, markets or industries.

Maybe we will turn this into a product and get a piece of that $15.7 trillion.

If you are still confused about AI, read this.

###################################

Artificial Intelligence for the Real World, Harvard Business Review

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Demystifying Artificial Intelligence

Forbes article, Demystifying Artificial Intelligence, points out that AI is on the minds of business executives. While 96% of businesses are doing something with AI, most still seem confused about how to put it to use:

O’Reilly Media Founder and CEO Tim O’Reilly observes,

“Everyone is talking about ‘AI’ these days, but most companies have no real idea of how to put it to use in their own business”.

Everyone seems to want to rush to the "sexy" part and don't realize that 80% of their effort will be related to getting their data properly organized and sorted out. Not getting their data sorted out is why most AI projects fail.

O'Reilly Media publishes The AI Ladder to help organizations to help sort out their strategy and tactics. Here is part of the conclusion of that document:

Finally, AI is not magic. It’s hard work. It requires the proper tools, methodologies, and mindset, to overcome the gaps that companies are facing (data, skills, and trust) to truly embrace an AI practice and put it to work across your organization. AI is the biggest opportunity of our time, and yet there’s still a certain fear in the market that AI is going to replace jobs. However, the reality is this: AI is not going to replace managers. Rather, the managers who use AI will replace the managers who do not.

Time to up your digital maturity. A good place to start is Artificial Intelligence and Knowledge Engineering in a Nutshell.

Also, here is how I got my data in order. And this is what I can do as a result.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Auditing XBRL-based Financial Reports

The document, Auditing XBRL-based Financial Reports, proves that an audit strategy can be created for XBRL-based financial reports.

Here are the cliff notes:

A financial report is an allowed interpretation of an expression of the financial position and financial performance of an economic entity per some set of statutory and regulatory rules. Here-to-for, that expression has been in a form that is only readable by humans. However, XBRL and other machine-readable formats change that, making those expressions readable by both humans and by machine-based processes.

Single-entry accounting is how ‘everyone’ would do accounting. In fact, that is how accounting was done before double-entry accounting was invented. Double-entry accounting was the invention of medieval merchants and was first documented by the Italian mathematician and Franciscan Friar Luca Pacioli.

Double-entry accounting adds an additional important property to the accounting system, that of a clear strategy to identify errors and to remove the errors from the system. Even better, double-entry accounting has a side effect of clearly firewalling errors as either accident or fraud. This then leads to an audit strategy. Double-entry accounting is how professional accountants do accounting.

An XBRL-based financial report is not only a machine-readable format; it also is a machine-readable logical system and has the potential to be a well-defined and fully expressed logical system. A well-defined logical system, when fully expressed, will be properly functioning and demonstrably consistent, valid, sound, and complete. These properties can be leveraged to offer a systematic audit strategy for XBRL-based financial reports.

Essentially, an XBRL-based financial report is a set of declarative statements provided in global standard XBRL format. Logic programming software applications such as Prolog, Datalog, Clips, and Answer Set Programming can provide feedback as to whether these statements are consistent, valid, sound, complete and otherwise properly functioning. Even XBRL processors and XBRL formula processors can effectively prove that XBRL-based financial reports are properly functioning to a large degree.

“It must be remembered that there is nothing more difficult to plan, more doubtful of success, nor more dangerous to manage than a new system. For the initiator has the enmity of all who would profit by the preservation of the old institution and merely lukewarm defenders in those who gain by the new ones.” Niccolò Machiavelli

################################

Assurance on XBRL Instance Document: A Conceptual Framework of Assertions

Digital Auditing: Modernizing Government Financial Statement Audit Approach

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print