BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from November 14, 2021 - November 20, 2021

Sensemaking

It always seemed that I have some sort of superpower when it comes to accounting information systems. Well, it seems that superpower has a name, "sensemaking".

The following are three definitions of sensemaking that I have run across:

"Sensemaking is the ability to determine the deeper meaning or significance of what is being expressed."

"Sensemaking is the process by which people give meaning to experience."

"Sensemaking or sense-making is the process by which people give meaning to their collective experiences."

Article, Making Sense of Sensemaking

"Sensemaking is literally the act of making sense of an environment, achieved by organizing sense data until the environment “becomes sensible” or is understood well enough to enable reasonable decisions."

Here is my composite definition based on what I am seeing and a synthesis of the definitions from above:

Sensemaking is the process of determining the deeper meaning or significance or essence of the collective experience for those within an area of knowledge.

Sensemaking is a tool. You can use sensemaking to construct a map you can share with others. Sensemaking is the art of analysing, understanding, clarifying, untangling, organizing, and synthesizing. As explained in this video, Introducing SenseMaking, the process of sensemaking involves:

- Looking for patterns in information.

- Making connections among different things.

- Synthesizing lots of information and categorizing it into small chunks.

- Think about the big picture.

- Think about the "why" of a situation.

- Organizing and untangling things.

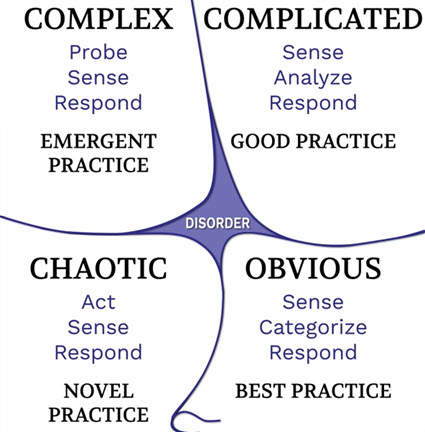

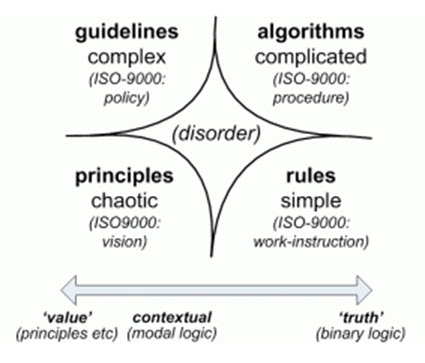

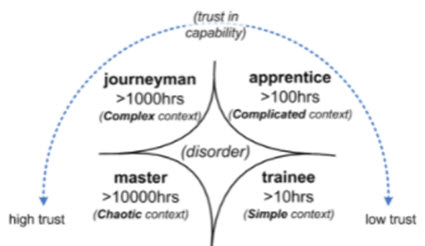

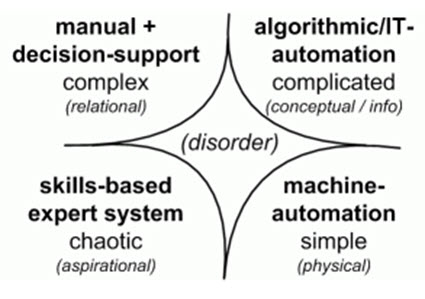

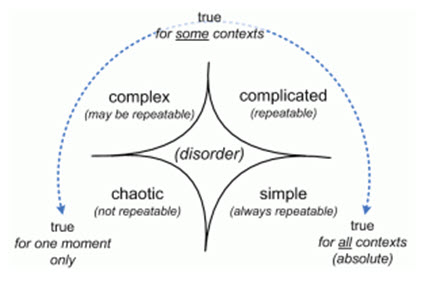

The Cynefin Framework is a sensemaking model. There are other types of sensemaking models. And even more types of sensemaking models. Here are the Cnyefin and other sensemaking models shown graphically:

Cynefin Framework:

ISO 9000 Quality Model:

Skill Level Model: (think CPA firm here; staff=trainee, senior=apprentice, manager=journeyman, partner=master)

Automation/Manual Model:

Repeatability and Truth Model:

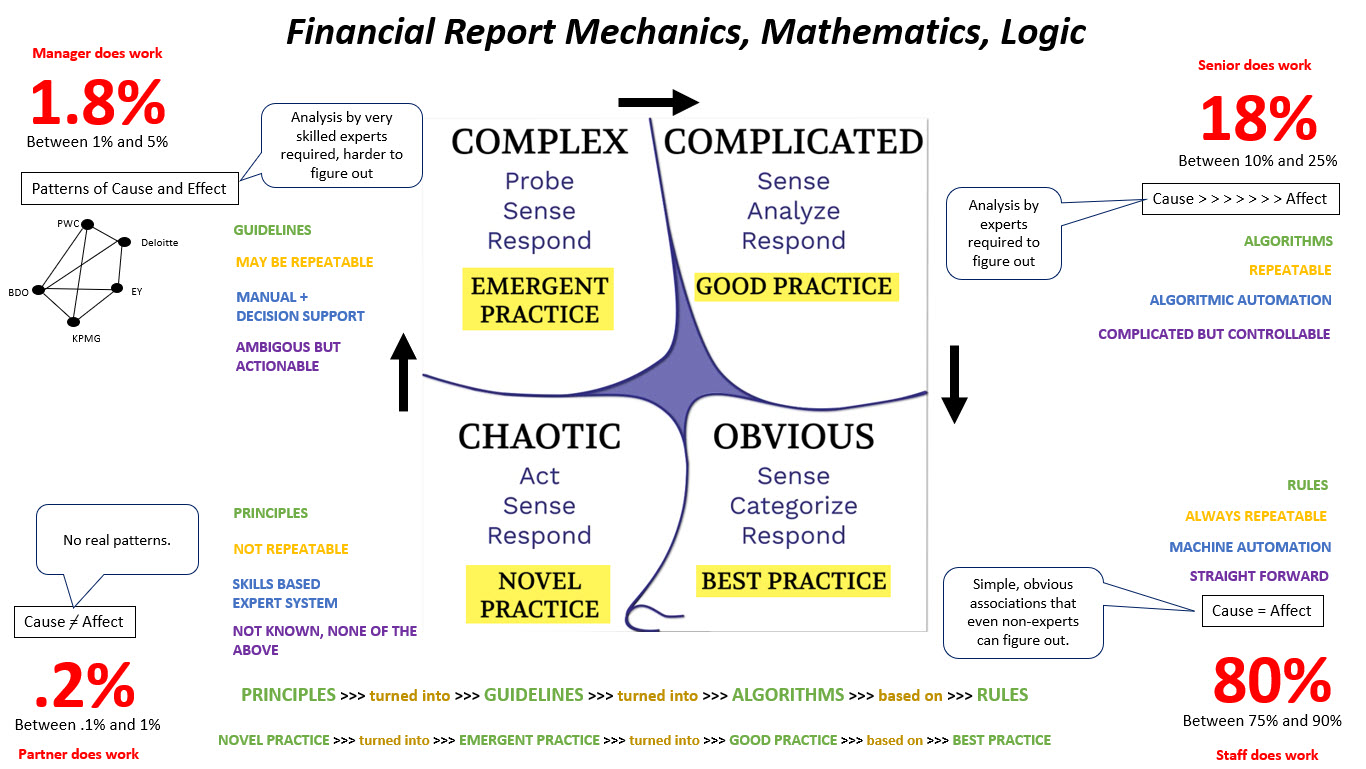

What is interesting is the descriptions of each of the five parts of each graphic above. "Disorder" is always in the center, you have the LOWER RIGHT=simple/obvious, UPPER RIGHT=complicated, UPPER LEFT=complex, and LOWER LEFT=chaotic. Look at the patterns and look at the subtexts.

Information for an area of knowledge can be broken down by those groups. Information in each of those groupings can be processed. The effort involved to process the information in the different groups varies, but all the information can be processed using automation. That processing needs to be controlled.

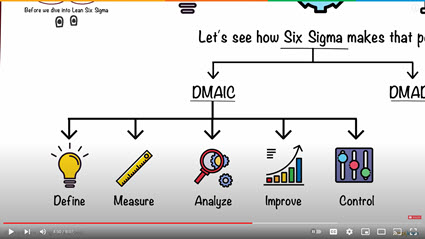

So now, take all of the above and think Six Sigma, Lean, and Lean Six Sigma. Those tools are a match made in heaven in terms of automation of tasks and processes. Have a quick look at Six Sigma and Lean Six Sigma:

Six Sigma in 9 Minutes: (tools for process improvement, tools for removing defects from a process)

Lean Six Sigma in 8 Minutes: (methodology providing value to customer, eliminating waste, continuous imporovement, reducing cycle time)

I have tried to synthesize all the important details into one graphic which I have provided below: (click on the image for a larger view)

If you put all of these pieces together and then think Financial Report Knowledge Graph and the Seattle Method; then you will better understand the future of accounting, reporting, auditing, and analysis.

What is happening is a foundational change: it is highly useful, highly novel, and highly complex. A disruptive innovation is about to occur.

Folks, software engineers are going to be able to automate the heck out of financial report creation tasks and processes. Those tasks and processes will leverage Lean Six Sigma techniques, principles, and practices. Accounting, auditing, and analysis will soon follow.

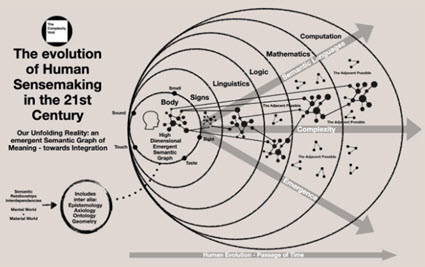

Graphic of the evolution of sensemaking:

##########################

The Hidden Brain: Rebel with a Cause (role of experience, skill, and experimentation in innovation)

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Financial Disclosures are Not Novel Art Projects

As pointed out by Mike Willis when with PriceWaterhouseCoopers, financial disclosures are not novel art projects akin to how highly skilled craftsmen assembled cars by hand prior to Henry Ford’s innovations that include the assembly line and standardization of parts.

This might come as a big surprise to most accountants, perhaps even shock. The term "generally accepted accounting principles" (GAAP) is used for a reason. Using the terminology of the Cynefin Framework, I would suspect that 80% of external financial disclosures follow "best practices", about 18% follow "good practices", perhaps 1.8% are "emergent practices" and maybe .2% are "novel practices".

Further, the average accountant is, well, average. My 10 years of creating XBRL taxonomies for financial reporting using US GAAP and IFRS included meeting many, many accountants who provided input as to what should be in those XBRL taxonomies. The discussions which took place were enlightening. Accountants, just like everyone else, make mistakes.

What I predict the future will bring is heavy use of templates and exemplars for creating financial disclosures. Here is a prototype of a template gallery that I created. Here is another prototype. Works similar to how templates work for, say, Microsoft PowerPoint or Word. This just makes a lot of sense.

What I predict the future will bring is heavy use of templates and exemplars for creating financial disclosures. Here is a prototype of a template gallery that I created. Here is another prototype. Works similar to how templates work for, say, Microsoft PowerPoint or Word. This just makes a lot of sense.

Financial reports are far more consistent than you might think. Don't take my word for it, have a look at all those reports in the EDGAR system. The AICPA publishes a book, Best Practices in Presentation and Disclosure. PPC's Guide to Preparing Financial Statements which is published by Thompson Reuters is a similar guide.

Besides, forget about public companies for a moment. Think about the smaller accounting firms and the millions of companies creating financial reports. Think of that bell shaped curve. Mistakes are made. Templates and best practices guides help avoid mistakes.

Today, these guides are readable only by humans. Soon, this best practices and good practices guidance will also be readable by machines. That information will be used to gulde expert systems for creating financial reports.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print