BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from January 23, 2022 - January 29, 2022

Accounting Oracle Machine

Creating something like an accounting oracle machine certainly seems conceivable. Computability theory and computational complexity theory seem to provide information about some of the possibilities here. The information in an area of knowledge such as the area of accounting, reporting, auditing, and analysis can be organized using the Cynefin Framework. The information is not "random" or "unorganizable".

The hard part about creating something like an accounting oracle machine is not the computation part; the hard part is more about pulling all the machine-readable rules together effectively and efficiently. This is expensive and time consuming and is not something that any one organization can really do.

But a coordinated group could pull this off and do so effectively and efficiently. The tools of the information age can be brought to bare to help make this happen.

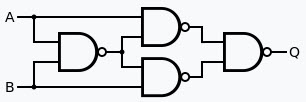

Building an accounting oracle machine is about giving accountants the capabilities to organize the information represented by logic gates that make up the machine-readable knowledge graph that drives the oracle.

Do issues exist when you try and create something like an accounting oracle machine? Certainly. Not every piece of information will be disputed, for example, the accounting equation (“Assets = Liabilities + Equity”) is really not disputed. But there can be areas where multiple perspectives jostle for prominence, the leaders of different factions of each perspective will argue with one another, and dissonance will rule the day.

However, a good conductor can get the orchestra into harmony.

Achieving this harmony can be hard in some cases, but in the area of knowledge such as accounting, because it is an organized profession with clear rules in most cases; something like an accounting oracle machine is quite possible.

An accounting oracle machine will be made up of two things: rules, engine (to process rules). The rules will be created by knowledgeable business professionals and will be declarative as per the Business Rules Manifesto. The rules format will be some global standard, XBRL can work. The engine will be one of the three primary problem solving logic implementation approaches. Here are the beginnings of such an accounting oracle machine:

To the untrained eye, all this seems impossible. When using proper sensemaking techniques, all this is really pretty straight forward to understand. Accounting is a very straightforward mathematical model. For the things that can, and should, be put into something like an accounting oracle machine here is the breakdown; 80% anyone can create, about 18% will be easy for professional accountants to create, about 1.8% will be hard for accountants to create, and .2% will be a complete struggle. About 80% of the effort for accountants is understand WHAT should be defined in such an oracle and 20% of the effort will be doing the work.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

1 Reference

|

1 Reference

|  Email

|

Email

|  Print

Print

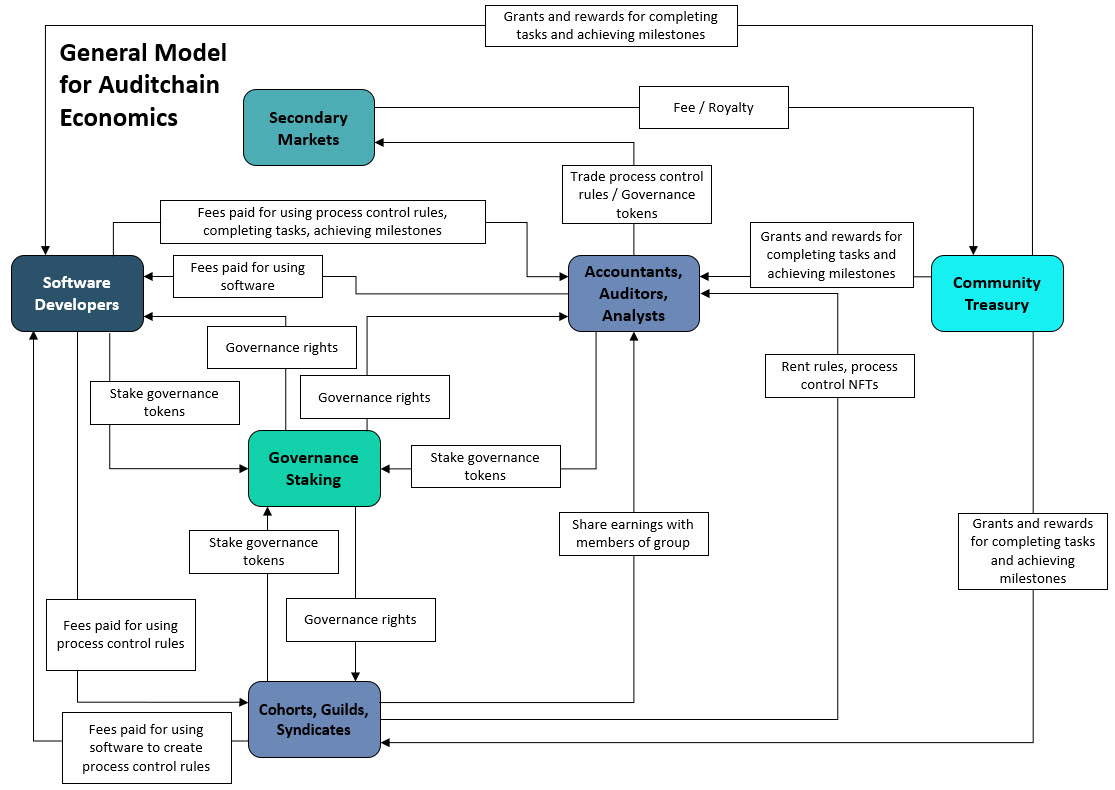

Auditchain Appears to have a Work-to-Earn (W2E) Model

An article by Tatiana Revoredo, Blockchain and the evolution of business models in the game industry, that I was made aware of explains Auditchain's "Work-to-Earn (W2E)" model. That article uses the term "play-to-work" and discusses gaming, but I am taking that same explanation and applying it to work. Here is my explanation:

Work-to-earn (P2E) model

The “work-to-earn” model is exactly what the name suggests: A model where users (accountants, auditors, analysts, software engineers, etc.) can work and earn tokens or cryptocurrency (i.e. AUDT tokens in this case) while working. This model (gamified incentive model) is based on science and has a very powerful psychological incentive, because it combines two activities that have driven humanity since the beginning of time: reward and work.

The main idea in W2E is that contributors are rewarded as they invest more time and more effort in the ecosystem, and thus become part of the economy (tokenomics), creating value for themselves, for other participants in the ecosystem, and also for software developers. They receive an incentive/reward for their participation and work time in the form of digital assets with potential appreciation of those digital assets over time.

Along these lines, the key component in this model is to give workers "ownership" over certain "digital assets" in the ecosystem, allowing them to increase their value by actively participating. This is where blockchain technology has become decisive for work business models.

The article provides a graphic that explains the economics generally for gaming. I have recast that general model specifically to Auditchain and this is what I came up with:

I have updated my document, Auditchain Explained in Simple Terms, with this information.

More information:

Let’s Build A Decentralized Game Economy Using Blockchains [Part 1]

It seems like others get this. See Twali.

########################################

Charlie

in Digital Financial Reporting

|

Post a Comment

|

1 Reference

| Email

| Print