BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries by Charlie (1695)

Accounting Oracle Machine

Creating something like an accounting oracle machine certainly seems conceivable. Computability theory and computational complexity theory seem to provide information about some of the possibilities here. The information in an area of knowledge such as the area of accounting, reporting, auditing, and analysis can be organized using the Cynefin Framework. The information is not "random" or "unorganizable".

The hard part about creating something like an accounting oracle machine is not the computation part; the hard part is more about pulling all the machine-readable rules together effectively and efficiently. This is expensive and time consuming and is not something that any one organization can really do.

But a coordinated group could pull this off and do so effectively and efficiently. The tools of the information age can be brought to bare to help make this happen.

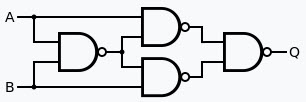

Building an accounting oracle machine is about giving accountants the capabilities to organize the information represented by logic gates that make up the machine-readable knowledge graph that drives the oracle.

Do issues exist when you try and create something like an accounting oracle machine? Certainly. Not every piece of information will be disputed, for example, the accounting equation (“Assets = Liabilities + Equity”) is really not disputed. But there can be areas where multiple perspectives jostle for prominence, the leaders of different factions of each perspective will argue with one another, and dissonance will rule the day.

However, a good conductor can get the orchestra into harmony.

Achieving this harmony can be hard in some cases, but in the area of knowledge such as accounting, because it is an organized profession with clear rules in most cases; something like an accounting oracle machine is quite possible.

An accounting oracle machine will be made up of two things: rules, engine (to process rules). The rules will be created by knowledgeable business professionals and will be declarative as per the Business Rules Manifesto. The rules format will be some global standard, XBRL can work. The engine will be one of the three primary problem solving logic implementation approaches. Here are the beginnings of such an accounting oracle machine:

To the untrained eye, all this seems impossible. When using proper sensemaking techniques, all this is really pretty straight forward to understand. Accounting is a very straightforward mathematical model. For the things that can, and should, be put into something like an accounting oracle machine here is the breakdown; 80% anyone can create, about 18% will be easy for professional accountants to create, about 1.8% will be hard for accountants to create, and .2% will be a complete struggle. About 80% of the effort for accountants is understand WHAT should be defined in such an oracle and 20% of the effort will be doing the work.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|

1 Reference

|

1 Reference

|  Email

|

Email

|  Print

Print

Auditchain Appears to have a Work-to-Earn (W2E) Model

An article by Tatiana Revoredo, Blockchain and the evolution of business models in the game industry, that I was made aware of explains Auditchain's "Work-to-Earn (W2E)" model. That article uses the term "play-to-work" and discusses gaming, but I am taking that same explanation and applying it to work. Here is my explanation:

Work-to-earn (P2E) model

The “work-to-earn” model is exactly what the name suggests: A model where users (accountants, auditors, analysts, software engineers, etc.) can work and earn tokens or cryptocurrency (i.e. AUDT tokens in this case) while working. This model (gamified incentive model) is based on science and has a very powerful psychological incentive, because it combines two activities that have driven humanity since the beginning of time: reward and work.

The main idea in W2E is that contributors are rewarded as they invest more time and more effort in the ecosystem, and thus become part of the economy (tokenomics), creating value for themselves, for other participants in the ecosystem, and also for software developers. They receive an incentive/reward for their participation and work time in the form of digital assets with potential appreciation of those digital assets over time.

Along these lines, the key component in this model is to give workers "ownership" over certain "digital assets" in the ecosystem, allowing them to increase their value by actively participating. This is where blockchain technology has become decisive for work business models.

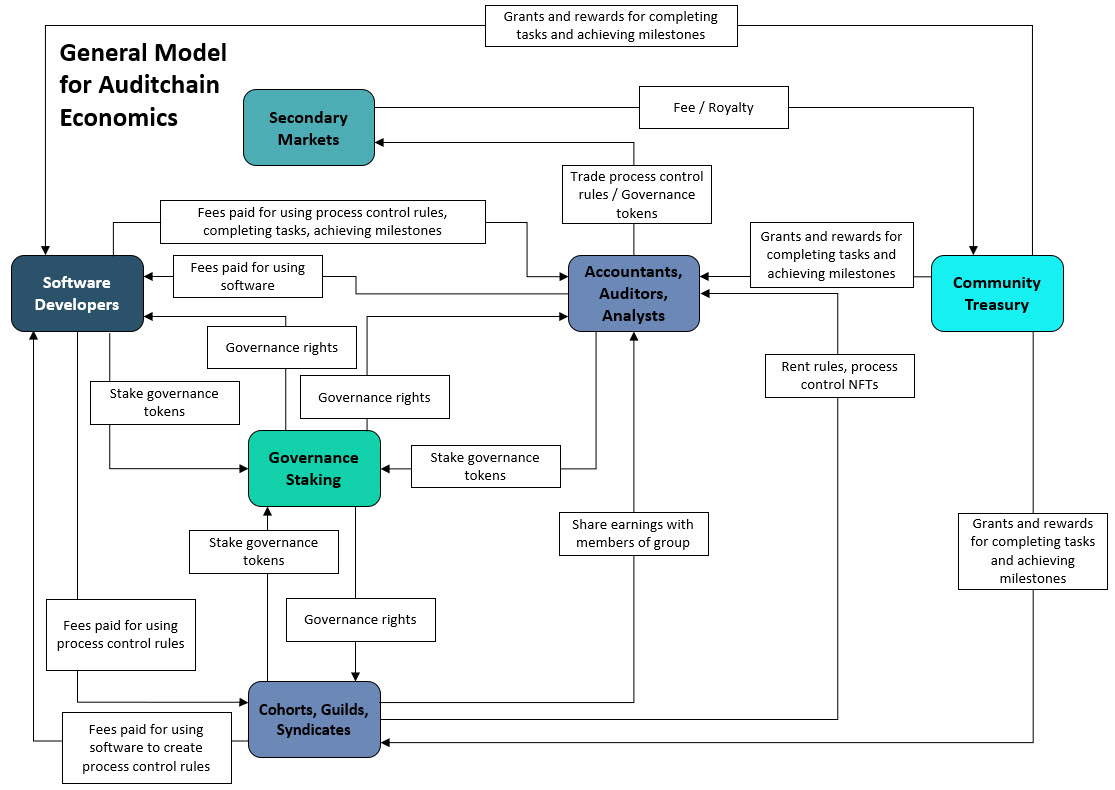

The article provides a graphic that explains the economics generally for gaming. I have recast that general model specifically to Auditchain and this is what I came up with:

I have updated my document, Auditchain Explained in Simple Terms, with this information.

More information:

Let’s Build A Decentralized Game Economy Using Blockchains [Part 1]

It seems like others get this. See Twali.

########################################

Charlie

in Digital Financial Reporting

|

Post a Comment

|

1 Reference

| Email

| Print

Very Basic of Financial Report Validator

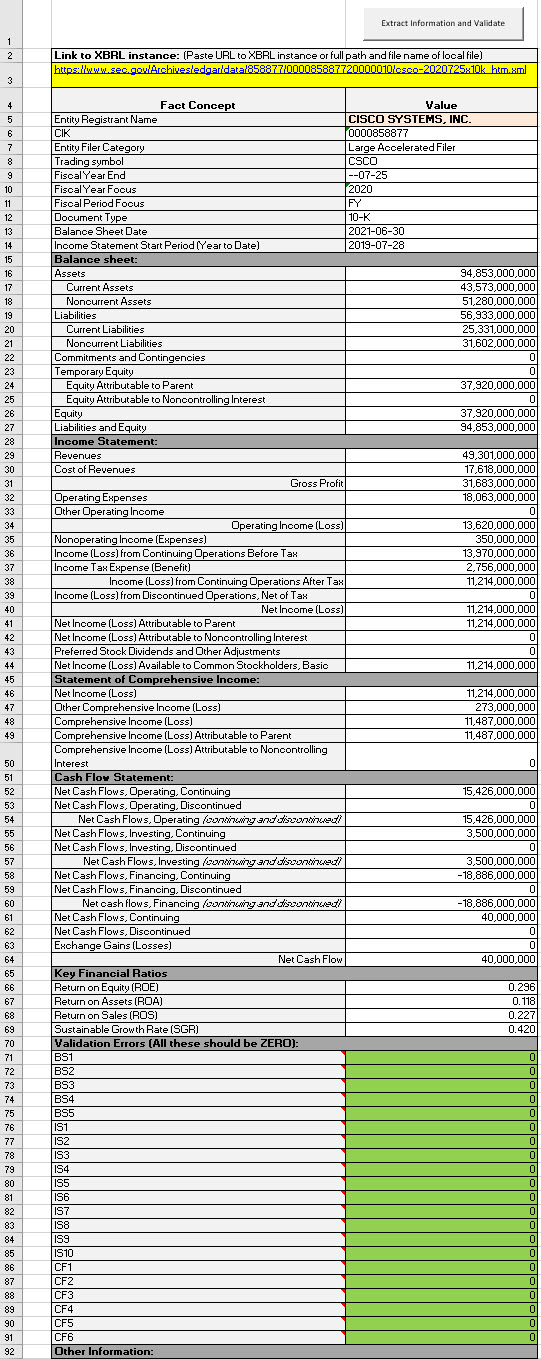

This is a very, very basic XBRL-based financial report validator that I have created using Excel. There are two versions:

There are a bunch of ways these applications can be enhanced and improved such as not hard coding the rules into the validator, doing additional validation tasks, better functionality; my intent here is to simply point out the basics. Reverse engineering is an excellent way to learn.

Here are example Line of Reasoning Reports that are output by the application:

Below is a screen shot of the single report validator. To use the validator all you do is put a URL to an XBRL-based financial report into the YELLOW cell and then press the "Extract Information and Validate" button:

To use the mulitiple reoprt validator, simple click on the "Compare all in List Spreadsheet" in the "Compare" workbook.

Again, this is a very basic validator. The Pacioli Power User Tool is way more powerful but works using the same principles. (For more information about Pacioli, see the Pacioli Logic and Rules Engine.

Charlie

in Digital Financial Reporting

|

Post a Comment

|

1 Reference

| Email

| Print

Auditchain Explained in Simple Terms for Accountants

Over the past year or so I have had the opportunity to understand blockchain, cryptocurrencies, NFTs, DAOs, dApps, and the like by working on a project for Auditchain. I took that opportunity to try and understand what exactly Auditchain is and how that relates to the work I have been doing with XBRL-based digital financial reporting.

I have summarized all my observations in the document Auditchain Explained in Simple Terms.

Here is the executive summary:

Auditchain is a decentralized accounting, reporting, audit, and analysis ecosystem that enables control, reliability, trust, and therefore effective automation of tasks and processes. Auditchain is a mechanism that can be leveraged to implement modern accounting processes.

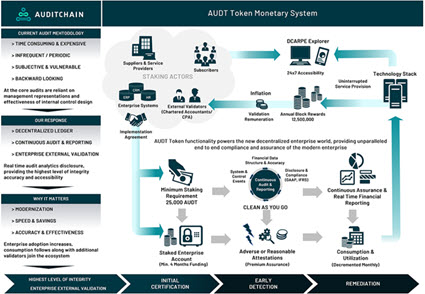

The Auditchain Protocol is the world’s first standards-based gamified incentive model-based decentralized continuous accounting, reporting, audit, and analysis virtual machine (a.k.a. operating system, ecosystem, platform, metaverse, system). Part the Auditchain DAO is the Auditchain Protocol and the AUDT token which are owned and governed by its community of AUDT token holders. The community itself provides orchestration of the system to maximize harmony and minimize dissonance.

Using Auditchain, processes and tasks that relate to accounting, reporting, auditing, and analysis can be controlled within and between enterprises. The Auditchain protocol enables accountants, auditors, and analysts to use software created by software engineers, financial standards created by standards setters and regulators to create machine-readable controls and instantiate those machine-readable controls as NFTs to reliably automate tasks and processes. Value is transferred between parties, paying or receiving, AUDT. System friction is reduced, processes are better, faster, and cheaper.

The Pacioli logic/reasoning/rules engine provides a standards-based PROLOG tool than enables machine problem solving capabilities. Pacioli is both an example of and the first decentralized application (dApp) and a core foundational software application that other dApps will use to provide functionality via the Auditchain utility for accounting, reporting, auditing, and analysis.

The ecosystem has modern software tools that supercharge accountants in the performance of the processes and tasks related to compliance reporting by leveraging artificial intelligence (for example).

Trust is maximized, provenance is established and immutable, rules-based artificial intelligence can be used effectively by business professionals. Enterprises can reliably and effectively stream machine-readable knowledge graphs of financial statements with real-time assurance applied by a cohort of Certified Public Accountants (CPAs) and Chartered Accountants (CAs) and that financial and nonfinancial information can be used by Chartered Financial Analysts, (CFAs), data subscribers, regulators, investors and other business professionals or software developers supporting those business professionals in the performance of their work tasks and processes.

A market place results. Royalties are paid to the participants within the ecosystem when work is performed, NFTs are used, software is created, verification is performed, or value is provided in some other manner.

If you have any additional ideas or think that I am getting something wrong, please let me know.

######################

Auditchain Enters into Agreement with Digital Accountancy Show

Charlie

in Digital Financial Reporting

|

Post a Comment

|

1 Reference

| Email

| Print

Business Events Drive Accounting

I am doing some brainstorming which I have summarized in this document, Accounting Basics (Brainstorming). Thank you to Willi Brammertz who is behind ACTUS (Algorithmic Contract Types Unified Standards) who helped me understand all this better per his use of standard financial contracts.

The bottom line is this:

- Business event patterns exist. (Another name for business event might be Economic Event.)

- Business events drive accounting transactions.

- It is at the business events level that you want to apply expert systems functionality to assist those entering accounting transactions.

Another piece of this puzzle I am trying to piece together is REA or Resource-Event-Agent patterns. This video, REA Models, provides an introduction to REA. This video, Introduction to REA, provides another good introduction. Finally, this video, REA, provides another good introduction. (This appears to be the origional REA academic paper.)

Wikipedia points out that REA is popular when teaching accounting information systems but is rare in actual accounting systems implementations with a few exceptions. One thing REA seems to be trying to do is get rid of the double entry bookkeeping model. That is a BIG MISTAKE in my view. They don't seem to grasp that the double entry bookkeeping model was created to detect errors and differentiate errors from fraud. REA also seems to be used to design accounting systems databases.

I see REA as being valuable in a different place: understanding and documenting business events that exist (or economic events might be a better name) for the purpose of building expert systems functionality for entering the accounting transactions.

So I had been focused on record-to-report. That focus could be wrong. The proper focus might be from business event to report.

More to come...so stay tuned.

#################################

Solitx - Empowering Digital Banks; ARIADNE

Algegraic Models for Accounting Systems

The Theory and Development of a Matrix-based Accounting System

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print