BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from September 1, 2016 - September 30, 2016

Creating High Performance Teams

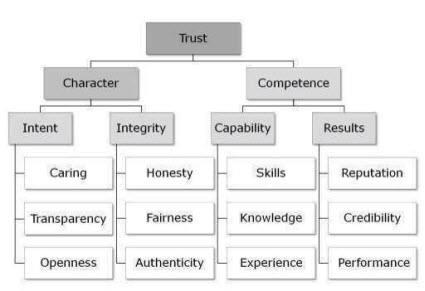

In a video, The New Leadership Paradigm: An Interview with Richard Barrett, Richard Barrett explains that the essential ingredient of a high-performance team is trust. What is trust? The graphic below provides a breakdown of what creates trust. Before trust exists, certain other dependencies must also be present. The principal components of trust (the dependencies) are shown in the following diagram:

(The New Leadership Paradigm)

(The New Leadership Paradigm)

Being a high-performance team provides a competitive advantage. High-performance teams eliminate unnecessary or unproductive work that does not add value; enabling focus on necessary and productive work.

Charlie

in General Information

|

Charlie

in General Information

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Using CLIPS to Understand Expert Systems and Logic Programming

CLIPS is a tool for building expert systems originally developed by NASA. Since it was first released in 1986 it has undergone significant enhancements and was put into the public domain by NASA in about 2002. CLIPS continues to be maintained as public domain software.

Here is documentation and other information that will help get you started with CLIPS should you have the curiosity:

- CLIPS website

- Download CLIPS 6.3

- YouTube Video Introduction to CLIPS, gets you familiar with the software interface and basics related to using the tool

- CLIPS Tutorial (three parts)

- CLIPS Documentation

- Users Guide which provides an elementary introduction to expert systems for people with little or no experience with expert systems.

- Basic Programming Guide

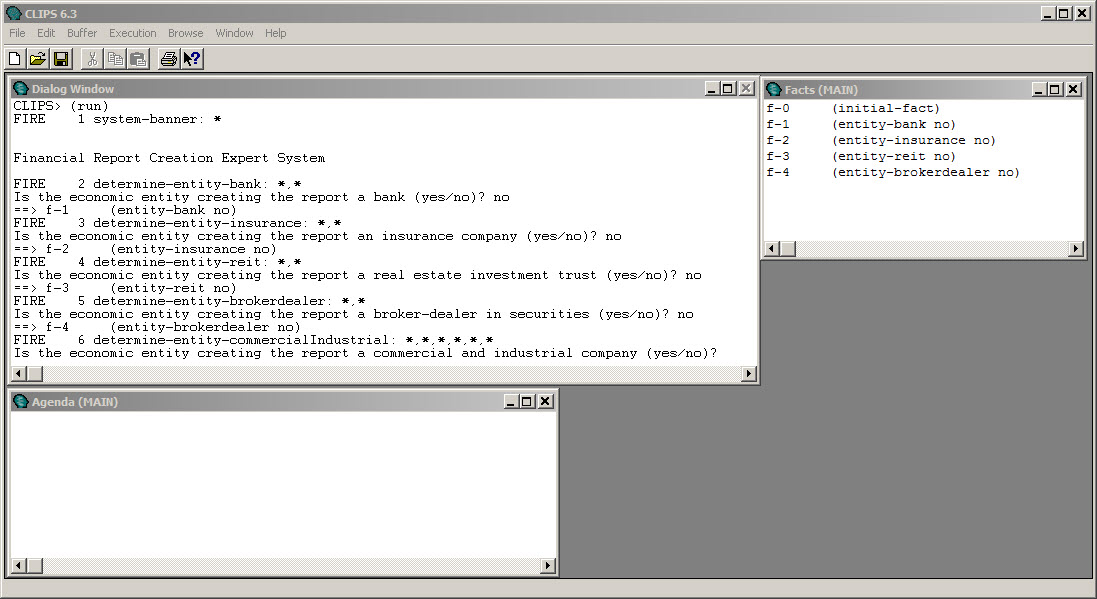

With that documentation above, I had a working expert system in about 4 hours. Here you go:

(Click image for larger view)

(Click image for larger view)

What my first expert system does is help someone understand what reporting style a financial report needs to be based on information about the economic entity creating a financial report. It is not complete yet, but I was able to learn a lot and am off to a good start.

If you want to understand expert systems, CLIPS is an excellent investment. Right off the bat you learn the different between a declarative programming language and a procedural language. I explain the importance of this difference in my document Complete Introduction to Business Rules for Professional Accountants (page 7). You will learn why business rules should be declarative, not procedural.

Another thing you learn is the difference between different programming paradigms. Understanding logic programming helps you see that software programs can be broken into two parts: the logic component and the control component.

Why does all this matter? It matters because it helps you understand (a) that you don't need to understand how to code to get a computer to do work for you; and (b) separating logic and control makes maintenance of things easier.

If none of this make sense to you, please read the document Comprehensive Introduction to Knowledge Engineering for Professional Accountants.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

1 Reference

| Email

| Print

1 Reference

| Email

| Print

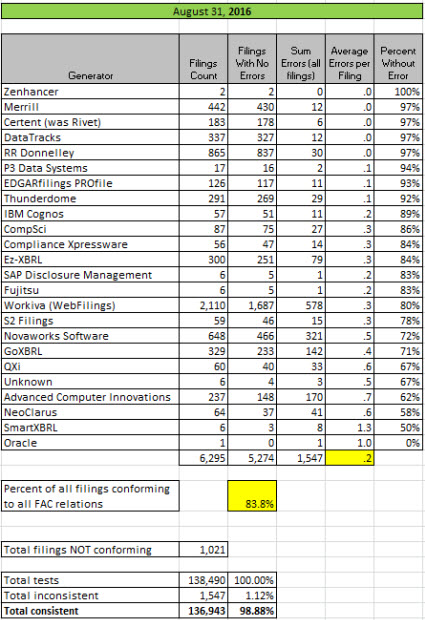

Public Company Quality Continues to Improve, 8 Generators above 90%

The quality of XBRL-based public company financial filings continues to improve steadily. Now, 8 software vendors/filing agents are in the range where 90% of more of their reports are consistent with all of the fundamental accounting concept relations.

EDGARfilers PROfile was the most recent filing agent to reach the 90% level of quality. They were at 76% back in March 31, 2016, moved to 82% at June 30, 2016; and climbed to 93% consistency as of the end of August 2016.

As I pointed out in another blog post, consistency with the XBRL US Data Quality Committee validation criteria averages about 81.7%.

* * * PRIOR RESULTS * * *

Previous fundamental accounting concept relations consistency results reported: June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print