BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from March 24, 2019 - March 30, 2019

Quarterly XBRL-based Public Company Financial Report Quality Measurement (March 2019)

The following is a summary of the quality measurements of XBRL-based US GAAP financial reports submitted to the SEC as of March 31, 2019.

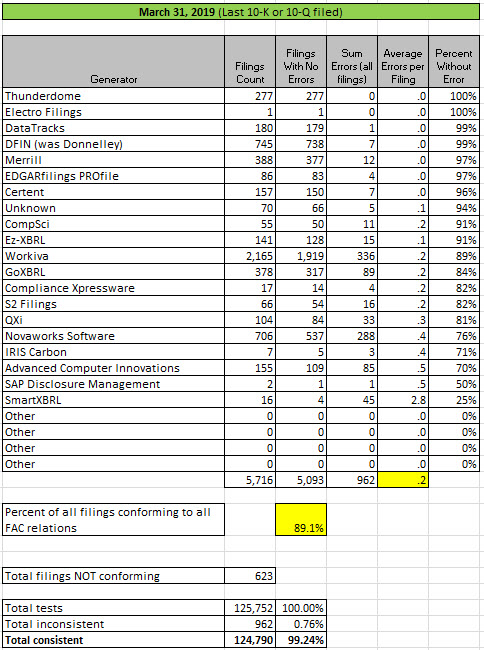

A couple of items worth noting. First, for the very first time a filing agent has 100% of the reports that the have submitted 100% consistent with all the fundamental accounting concept relations. That filing agent is RDG, the software they use is Thunderdome. Honorable mention goes to DataTracks who has only 1 filing that has an error. Second, a total of 5,063 of 5,716 or 89.1% of all XBRL-based financial reports submitted to the SEC are consistent with all of the fundamental accounting concept relations. Only 623 are not.

Fundamental accounting concept relations continuity cross checks

The fundamental accounting concept relations continuity cross checks verifies that high-level reported information is fundamentally usable. The following Excel spreadsheets and other documents provide details related to these quality measurements:

- Negative results from tests (i.e. confirmed errors): Details of 100% of the confirmed errors. 962 errors contained with 623 filings.

- Documentation helpful in understanding errors: Information that is helpful if you want to understand the errors.

- Best Practices for Evaluating an XBRL-based Digital Financial Reports: Explains how to evaluate an XBRL-based digital financial report.

- Overview of US GAAP Reporting Styles: Helps you understand the reporting styles used by US public companies that report using US GAAP.

- Excel base extraction tool: Allows you to extract information from about 4,060 or about 68% of all reports that use different reporting styles. There are also several entity comparisons.

- Consistent Financial Report Core Logic: Shows financial report core logic working for 5,127 public companies. (same information in order By Assets | By Net Income (Loss) | By Net Cash Flow)

- Inconsistent Financial Report Core Logic: Shows financial report core logic NOT WORKING for 589 public companies.

FAC by Generator:

US GAAP fundamental accounting concept relations continuity cross check validation results for last 10-K or 10-Q filed by generator of the report as of March 31, 2019:

(Click image for larger view)

(Click image for larger view)

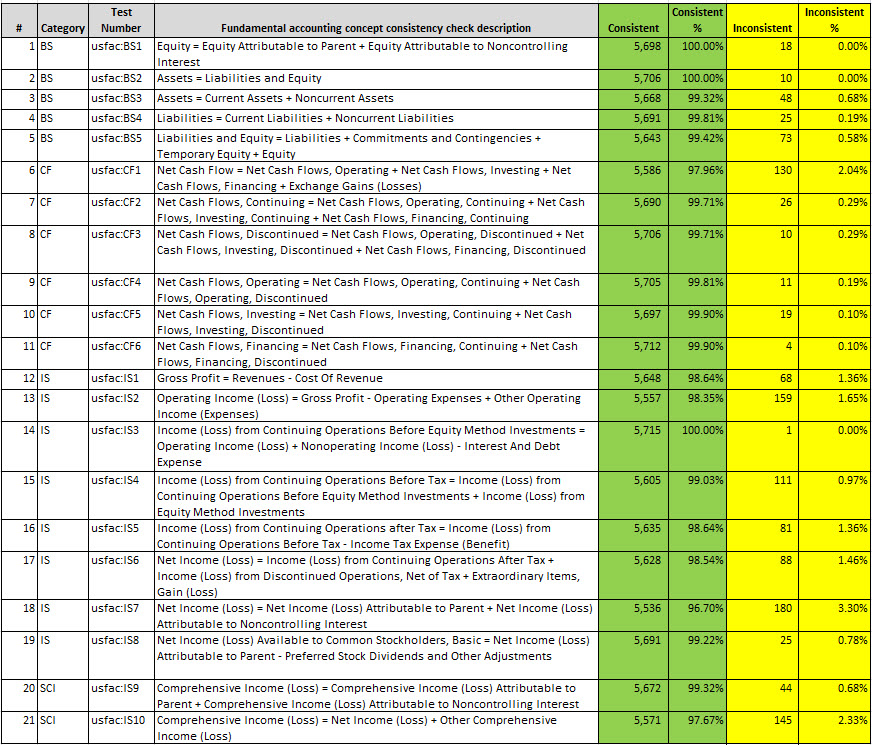

FAC by Test:

Same US GAAP filings as above but a summary of information by test of the reports as of March 31, 2019:

(Click image for larger view)

(Click image for larger view)

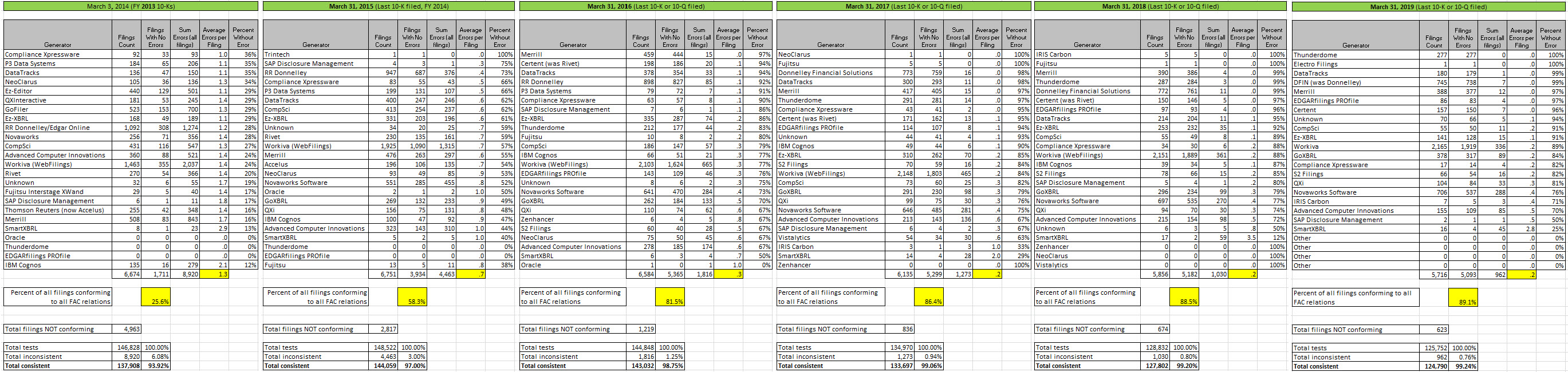

FAC Comparison 2014, 2015, 2016, 2017, 2018, 2019

Fundamental accounting concept relations continuity cross checks for 2014, 2015, 2016, 2017, 2018, and 2019 (last 10-K or 10-Q submitted by company as of March 31):

(Click image for larger view)

(Click image for larger view)

The incremental improvements may seem minor now, but if you consider then nature of compounding; even small changes year-to-year can mean great leaps compounded over longer periods of time. XBRL has only been used for about 10 years so far; XBRL is really only in its infancy.

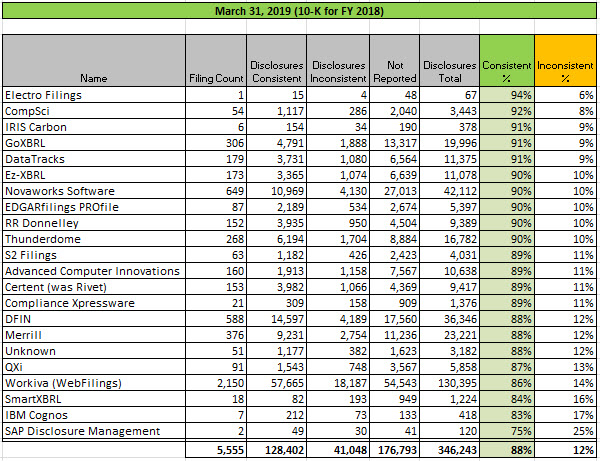

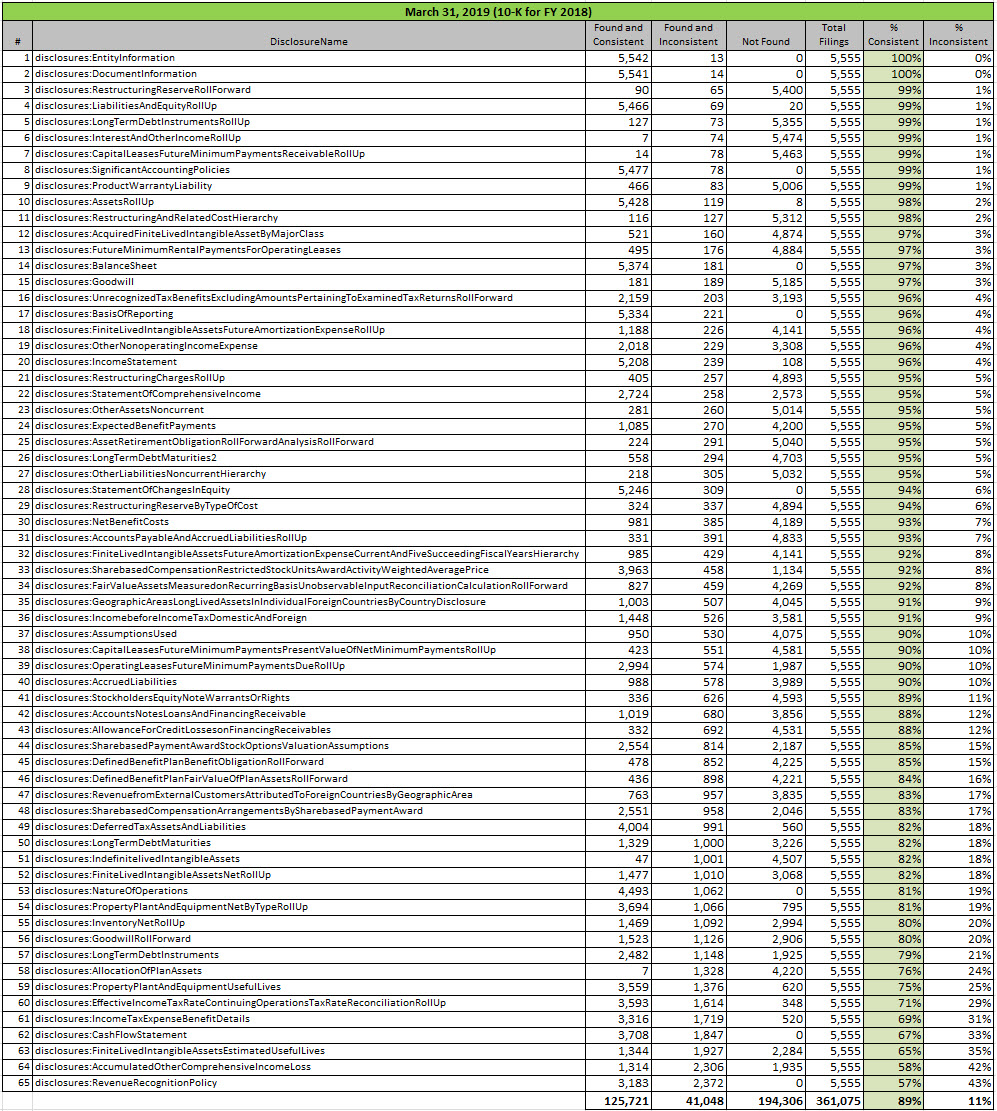

Disclosure mechanics and reporting checklist

There was not much of a change between prior year and this year when it comes to the disclosure mechanics and reporting checklist validation checks. On average, about 89% of disclosures were consistent with expectation.

Disclosure mechanics and reporting checklist results by generator:

(Click image for larger view)

(Click image for larger view)

Disclosure mechanics and reporting checklist results by disclosure:

(Click image for larger view)

(Click image for larger view)

Summary of Analysis of Disclosures

Analysis of 6751 Public Company 10-Ks

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: December 31, 2018; September 30, 2018; June 30, 2018; March 31, 2018; November 30, 2017; August 31, 2017; May 31, 2017; March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; December 31, 3015; September 30, 2015; June 30, 2015; April 1, 2015; November 29, 2014.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Best Practices for Evaluating an XBRL-based Digital Financial Report

XBRL-based general purpose financial reports will undoubtedly play some role in financial reporting going forward. There are already thousands and thousands XBRL-based general purpose financial reports being created every year all around the globe.

While many of these reports do not leverage XBRL's extensibility and are basically forms and easy to work with; there are many other reports that do leverage XBRL's extensibility and are considerably harder to work with. Over time software will improve and become easier to use.

But, most professional accountants are behind the learning curve when it comes to using XBRL. Even those professional accountants involved with creating XBRL-based reports that are submitted to the SEC still have a lot to learn. Why do I say that? Easy to understand errors that you see in the XBRL-based reports submitted by public companies to the SEC.

And so, to help rectify this situation several other CPAs and I have put together two documents. The first document, Best Practices for Evaluating an XBRL-based Digital Financial Report, provides a framework, principles, philosophies, processes, and techniques for evaluating the quality of an XBRL-based general purpose financial report. The second document, XBRL-based Digital Financial Report Analysis Report (Microsoft), is an actual analysis of a report using that guidance.

While other guidance exists, that guidance tends to be too general to be useful and not comprehensive enough to yield a good result.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Examples of Errors in XBRL-based Digital Financial Reports

I have many different blog posts that provide information about errors that exist in XBRL-based digital financial reports. Understanding errors and how to avoid them is a good way to learn about XBRL. To make finding these documents easier, I combined all of the best information into this one blog post where you can find all of this documenation.

These are documentation of fundamental accounting concept relations inconsistencies: (April 2017)

- Summary of 26 different errors

- BDO1

- BDO2

- BDO3

- EY1

- EY2

- EY3

- EY4

- EY5

- KPMG1

- KPMG2

- KPMG3

- KPMG4

- PWC1

- PWC2

- PWC3

- PWC4

- PWC5

- Deloitte1

- Deloitte2

- Deloitte3

- Deloitte4

- Grant Thornton

- Moss Adams

- DeCoria, Maichel & Teague

These documents show disclosure mechanics errors and other information:

- Future miniumum lease payments for capital leases

- Future minimum lease payments for operating leases

- Long term debt maturities

- Deferred tax asset (liability), Net

- Property, plant and equipment components roll up

- Long lived assets by geographic area

- Finite lived intangible assets estimated useful lives

- Capitalized computer software roll forward

- Accounts receivable roll up

- Nature of operations, basis of reporting, significant accounting policies, revenue recognition policy

- Accounts receivable net roll up

- Summary of concepts used to represent about 65 disclosures

- Disclosure best practices

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Additional Information for the Digital Information Reporting Developer

Bill Seddon, a software engineer at Lyquidity and XBRLQuery and creator of an open source XBRL processor, has created a resource page that supplements the information that I provide related to digital financial reporting. The page, Additional Information for the Digital Information Reporting Developer, targets the information needs of a developer looking to add support for Digital Financial Reports.

The page does not really add new stuff to the conceptual model, but rather its purpose is to bring together information across my sites that is relevant to a developer so there is no need to go hunting for that information.

However, it does try emphasise some important points that I seem to take for granted because I have been working with XBRL-based reporting for so long. Of course, once you learn of these points they are self-evident but until you make the connection certain things don't seem to make sense.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print