Business Reporting Logical Model Enhances Comparability and Interoperability

Another thing that the Business Reporting Logical Model does is enhance comparability and interoperability. Or to be more precise, the Business Reporting Logical Model minimizes the effort required to achieve comparability and interoperability. It opens the possibility of a business domain to create comparability, should they desire to do so. Interoperability means easier to use software and less costly software for business users.

Here is why.

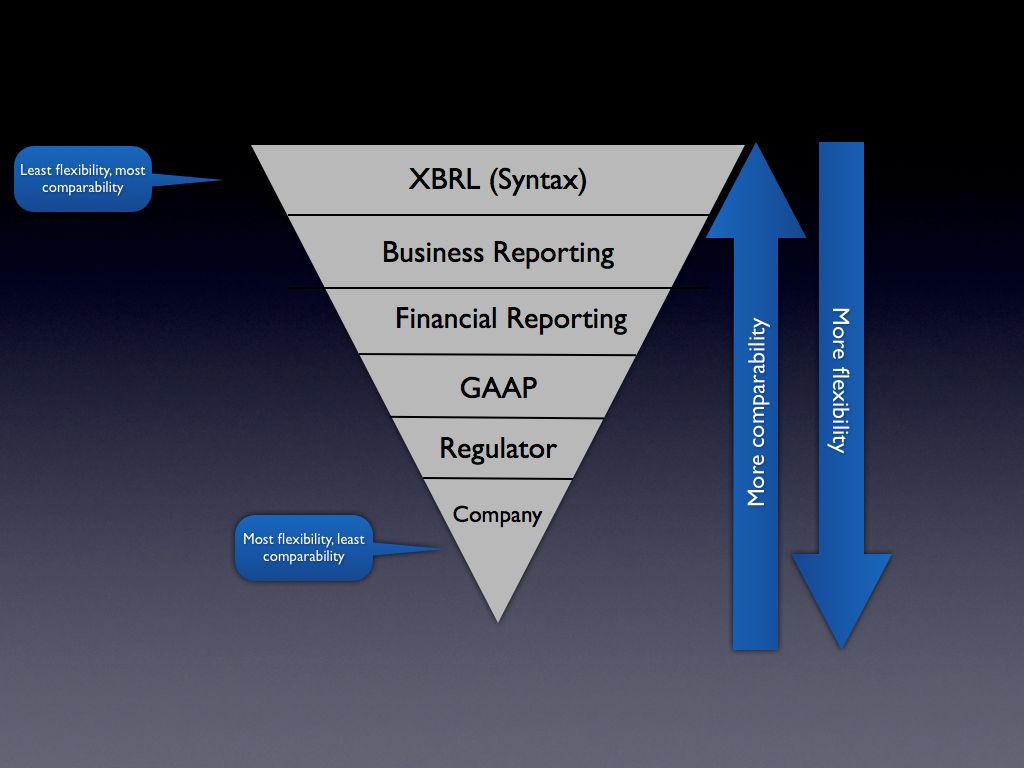

Comparability

(Here is a link to a PDF of this graphic.)

Today, there is no logical model below the XBRL syntax level. The only model any business domain has to work with is the XBRL syntax or some model they create. Creating that model and all the infrastructure to enforce that model takes time and costs money.

Or, another way of looking at this is that each company desiring to use XBRL for, say, financial reporting could create their own model using XBRL. That model could be 100% XBRL compliant (i.e. comply with the global standard). Each company would have to deal with all the "stuff" in the middle such as which GAAP (accounting standards they would use), create their own XBRL taxonomy, and so forth.

The "middle ground" needs to be created. The US GAAP Taxonomy created some of this middle ground. You can see that middle ground in the US GAAP Taxonomy Architecture. But, the US GAAP Taxonomy is not enough. That is why the SEC had to create a boatload of additional EDGAR XBRL Validation tests (see this list of errors, here is the test suite). Of course, the SEC would probably never want XBRL International to deal with 100% that that specific regulator needs to deal with, nor would XBRL International members do that; it would be like everyone agreeing to do business reporting exactly like the SEC does it, that would become the XBRL standard.

Business information exchange is a balancing act. Where agreement is achieved has ramifications for business users. Too much flexibility has its issues, too much comparability (or requiring things too high in the stack) has its issues. Where comparability exists within the "stack" (the diagram above) is up to the business domain's implementation of XBRL. XBRL itself does not control this. How XBRL is used does.

Interoperability

There is another piece to this puzzle. XBRL is a standard. What a system needs to make business information exchange work properly, it seems to me, is a protocol. There is a difference between a standard and a protocol. A difference worth understanding. Erez Ascher (Ascher Consulting & Development) articulates the difference between a protocol and a standard as:

- A protocol is a series of prescribed steps to be taken, usually in order to allow for the coordinated action of multiple parties. In the world of computers, protocols are used to allow different computers and/or software applications to work and communicate with one another. Because computer protocols are usually formalized, many people consider protocols to be standards. However, such is not actually the case.

- Standards are simply agreed-upon models for comparison, such as the meter and the gram. In the world of computers, standards are often used to define syntactic or other rule sets, and occasionally protocols, that are used as a basis for comparison. Some good examples include ANSI SQL, used to compare derivations of the SQL database query language, and ANSI C, used to compare derivations of the C programming language.

In other words, it seems to me that protocols can be standards, but standards may not contain all that is necessary to "allow different computers and/or software applications to work and communicate with one another". Therefore, every business system, such as the SEC XBRL filings system, must add "stuff" to XBRL to turn the standard into a protocol it seems. For every system to have to do this is both inefficient and ineffective because you really don't get cross business system interoperability. What you get is what we have today - many point solutions or one-to-one integrations.

So not only does the Business Reporting Logical Model enhance comparability, it also enhances interoperability. The Business Reporting Logical Model can provide the pieces which can turn the XBRL standard syntax into a business reporting protocol. I am not sure if it is all the pieces, time will tell. But I am sure XBRL alone is not enough to give business users what they need from XBRL.

The Bigger Picture - Financial Reporting in the Age of the Semantic Web

There is a bigger picture here. Consider this blog post titled "Why the Semantic Web Will Fail". The post is pretty good, but what is really interesting are the comments to the post. The way I read that post and all the comments is that the Semantic Web is inevitable, but no one knows when it will arrive.

I contend that the Semantic Web is already here. The US Securities and Exchange Commission (every US public company financial in XBRL by July 2011), XBRL US (US GAAP Taxonomy), Tokyo Stock Exchange, Japan Financial Services Agency, Korean Stock Exchange, China Securities Regulatory Commission and Shenzhen Stock Exchange, Japan's EDINET, the Commission of European Banking Supervisors, the US Federal Deposit Insurance Corporation, the International Accounting Standards Board (IFRS, standardized financial reporting meta data expressed in the XBRL syntax) among others have already created pieces of it for financial reporting. The US SEC, Japan FSA, and IASCF are already reconciling their implementations of the XBRL standard to make them more interoperable. The Business Reporting Logical Model will make it so others don't have to go through this reconciliation process.

Is XBRL perfect? Certainly not. But XBRL is not RDF/OWL. Who cares, both XBRL and RDF/OWL are just syntax. On can convert from one syntax to another easy enough. The hard part, agreeing on the meta data and getting vendors to support the idea, is done (for US GAAP and IFRS). The IASB started on IFRS in the 1970's, even before the Internet existed. Most countries have either switched to IFRS already or will. Even if they all don't (i.e. the US will converge, but may not convert), reconciling US GAAP to IFRS is not that much of a challenge really. Oracle, SAP, and IBM all support XBRL within their software.

Maybe I am wrong, but it seems to me that a better question might be "When will others catch up to how the financial reporting business domain has embraced the Semantic Web?" That may by an over statement, financial reporting has a ways to go. The Business Reporting Logical Model will help others get into the Semantic Web easier than the early pioneers.

How did XBRL International get to where it is? Back in 2003 Joan Starr wrote an article Information politics: The story of an emerging metadata standard. Here is the article's abstract:

Information politics: The story of an emerging metadata standard by Joan Starr

This is the story of how one commercial metadata standard — XBRL, or Extensible Business Reporting Language — has attracted the participation and support of some of the world’s most powerful public and private organizations. It begins with a look at the nature and use of financial information in today's Internet-enabled environment and discusses three information use patterns: Transaction, retrieval, and reporting. While numerous, sometimes competing standards have been developed for transaction information, XBRL alone has emerged to address reporting formats. Today, the XBRL specification has wide support across the accounting, financial, and regulatory communities. This has come about largely through the efforts of the standards’ governing board, which has pursued a strategy of careful definition of market scope, deliberate courtship of important allies, and establishment of a culture of aggressive outreach for members. The results are impressive. Members of the organization are now positioned to take greatest advantage of a number of new entrepreneurial opportunities that have been created by the organization. Additionally, some participants are now representing the XBRL metadata standard as a key tool for the restoration of public confidence in the scandal-rocked accounting and investment industries. This may create a serious problem for researchers and investors as unaudited financial statements formatted in XBRL proliferate on the Web sites of corporations anxious to demonstrate a commitment to what some are calling "the new transparency."

XBRL seems to have achieved the right mix of technical and business participation. While what the technical people did was very good and very important, I think that what the business people who participated in XBRL created was perhaps even more important. Business users of XBRL should try and understand and push for the Business Reporting Logical Model to be standardized within XBRL International.

This will provide the flexibility where flexibility is needed, but also the things needed for a protocol to work well, be effective, and be efficient. Having every implementation of XBRL undertake this task will hurt XBRL, making comparability of XBRL based information more challenging and interoperability of XBRL software and different implementations near impossible.

So that is what I see. How do you see it?

Charlie

in Business Reporting Logical Model, Business reporting logical model, General Information, Modeling Business Information Using XBRL, XBRL General Information, XBRL and the Semantic Web, RDF/OWL, XBRLS, comparability

|

Charlie

in Business Reporting Logical Model, Business reporting logical model, General Information, Modeling Business Information Using XBRL, XBRL General Information, XBRL and the Semantic Web, RDF/OWL, XBRLS, comparability

|

Post a Comment

Post a Comment

View Printer Friendly Version

View Printer Friendly Version Email Article to Friend

Email Article to Friend

Reader Comments