BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from November 1, 2018 - November 30, 2018

Recognizing that Magic is Not Involved in Getting Computers to Perform Work

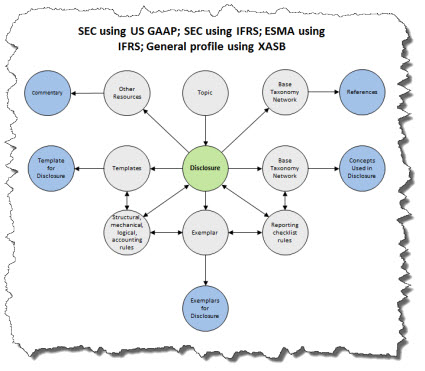

In a prior post, I pointed out the benefits of the notion of a "disclosure". I showed the diagram you see below.

I have expanded that diagram to include actual links to machine-readable metadata and in a separate diagram links to human-readable information that helps you better understand what the diagram is getting at better.

As you learned from reading the document Computer Empathy, computers don't work by magic. What seems to be magic is actually the result of attention to detail, good engineering, a good understanding of a domain of knowledge, and machine-readable metadata.

(Click image to navigate to machine-readable details)

(Click image to navigate to machine-readable details)

(Be sure not to miss the human-readable information. It will give you a sense of what is going on.)

I have been figuring out how to put the puzzle of financial reporting together for several years. The effort started long before Rene van Egmond and I wrote Financial Report Semantics and Dynamics Theory.

I have gone down some wrong paths that have led to dead ends. One dead end was OWL and RDF, basically trying to use the W3C semantic web stack. I found that path too complicated, too low-level, and something that could never be understood by professional accountants. Don't get me wrong, the W3C semantic web stack can work; but I could not make it work.

Another wrong path was creating what amounted to proprietary information formats. That works also, but it made things more complicated than they had to be and you lost the leverage offered by XBRL in some areas.

There were a few other dead ends.

But now, I have a very good framework where all machine-readable information is represented using the XBRL global standard. In my framework there is still one hold out that is represented in RSS. I could, and do, use an XBRL taxonomy schema to essentially provide a "list of options". An economic entity would use ONE item from that RSS list. XBRL does not really have a mechanism for articulating what it is that I want to articulate to the best of my knowledge; but I will check. For now, the single RSS file has to stay.

And so, now pretty much everything in my framework is global standard XBRL.

I added additional items to that "web" I showed in that first diagram. Now everything fits togeter. All the circles are connected but one. The only unconneced circle is the "Model Structure Rules". The reason the model structure rules are not connected is because those rules relate to the report level and not the financial reporting level like all the other information. Model structure relates to the allowed relations between Networks, Tables (hypercubes), Axis (dimensions), Members, Line Items, Concepts (primary items), and Abstracts.

Everything else is financial reporting related.

And while what I am showing in this first diagram relates to US GAAP; the same framework is used for IFRS and for the XASB reportring scheme which I use for testing and prototyping.

Not bad for a CPA. Fact is, there is no software engineer that understands financial reporting enough to do what I was able to do simply by paying attention to the information technology professionals. I honestly could not tell you the difference between "syntax" and "semantics" in 2007. But I fixed that problem by replacing my ignorance with knowledge.

I am now going to refactor the IFRS and XASB reporting scheme profiles to match the US GAAP profile.

Then, let the magic begin. Next step is to use all this metadata in software and show how XBRL-based digital financial reporting does not (a) have to be hard to use and (b) suffer from quality problems like the XBRL-based financial reports which are submitted to the SEC.

Time to disrupt financial reporting and build a modern finance platform because I am personally sick and tired of using outdated, even barbaric, approaches to creating financial reports.

Who else is with me? We have a small but growing group. If you are with me (i.e. you don't want to pave the same old goat path), please find the best information available on this page of my blog.

I still need to explain blocks better, stay tuned...that is next.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Machine Learning: Business Decision Maker

Amazon Web Services (AWS) is making their AI, machine learning, and deep learning internal training material available publically for free. There are courses for developers and for business professionals.

This is an excellent course path for business professionals:

Machine Learning: Business Decision Maker - Demystify machine learning, artificial intelligence, and deep learning.

Understanding the Power of Naming Disclosures

One of the things that I have done that has gotten a good deal of interest from accountants is the notion of "templates" and "exemplars" which I went over in this blog post. In particular, this graphic:

(Click image for a larger view)

What accountants don't generally realize is what it takes to make the notion of templates and exemplars to actually work. Also, they tend to not understand what templates and exemplars are useful for.

I mean, think about that. What exactly is a "template"? What is an "exemplar"? What is the relationship between a "template", an "exemplar", a "fragment" of a report, etc? What are they useful for? All of that will be explained in the future.

What I want to point out is the power of giving a disclosure a computer addressable name. Think about something. How do you actually get "templates" and "exemplars" to actually work and what does "work" even mean?

What templates and exemplars actually do will become crystal clear when I get the functionality working the way I want it to work within a software application. Then, there will be no misperceptions about what a template is, what an exemplar is, and the value the notion of "templates" and "exemplars" bring to financial reporting process, techniques, tasks, workflows, and philosophies.

What I want to explain is how I get all this to work.

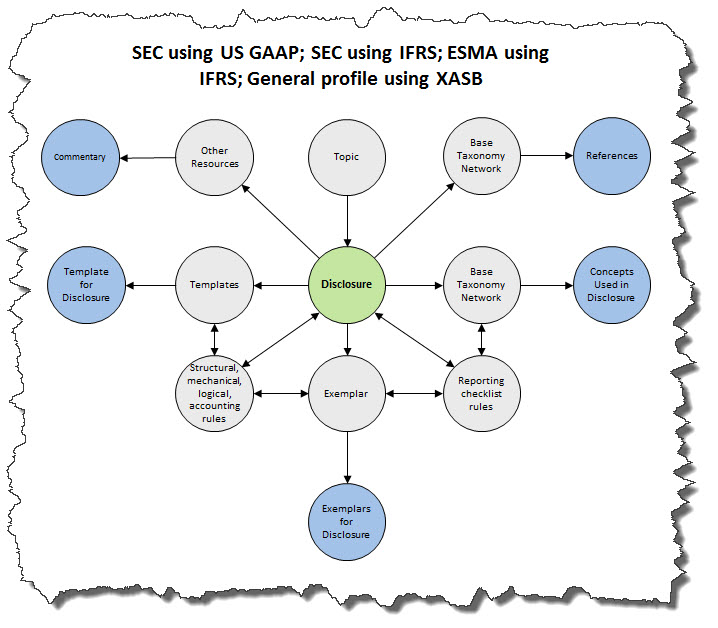

Here is the big picture if you are interested. Key to the notion of "templates" and "exemplars" is the notion of the "disclosure". Take a look at the graphic below (click the image to get a larger view):

(Click image for larger view)

(Click image for larger view)

Note the "disclosure" in the center of the graphic and that there is a lot of stuff hanging off of that part of the graphic. The arrows represent connections between metadata that describe disclosures, templates, exemplars, references, commentary, rules, topics, and the base taxonomy.

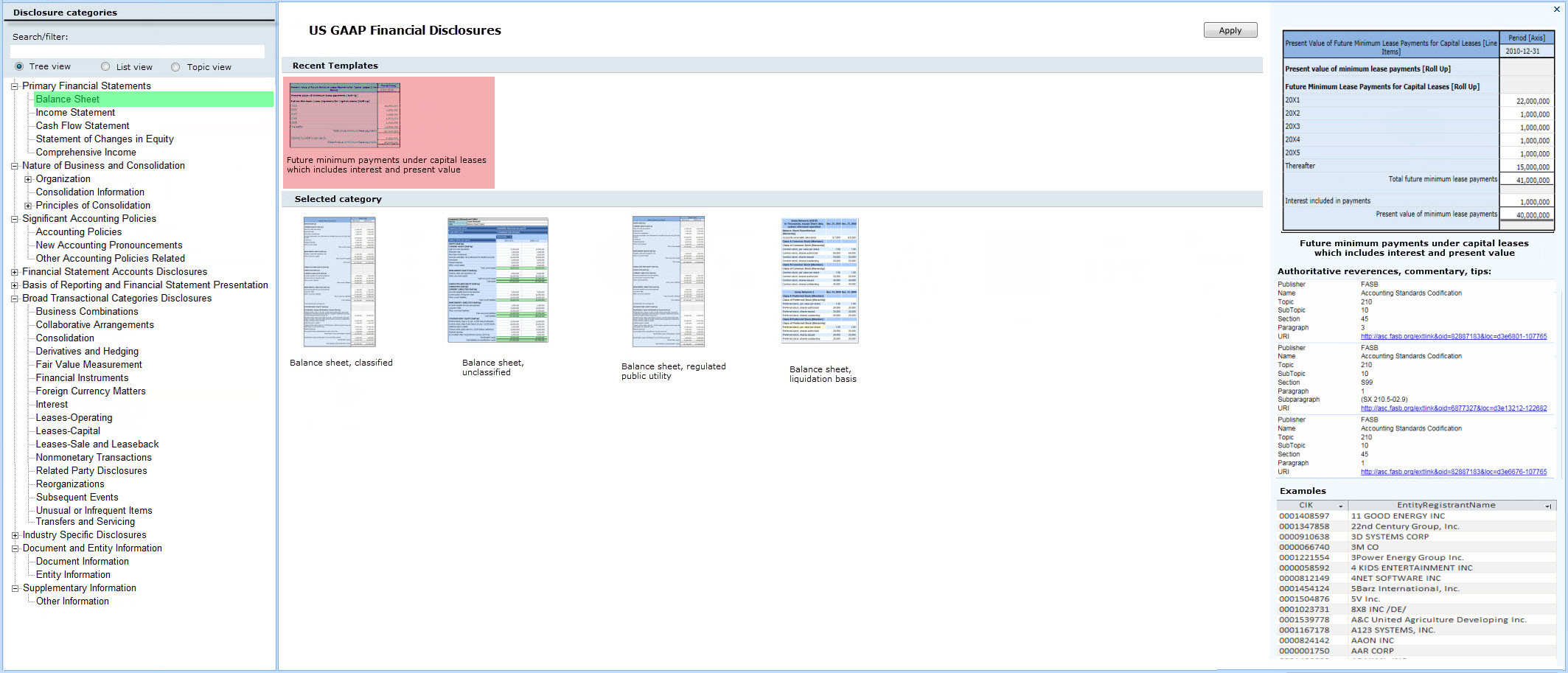

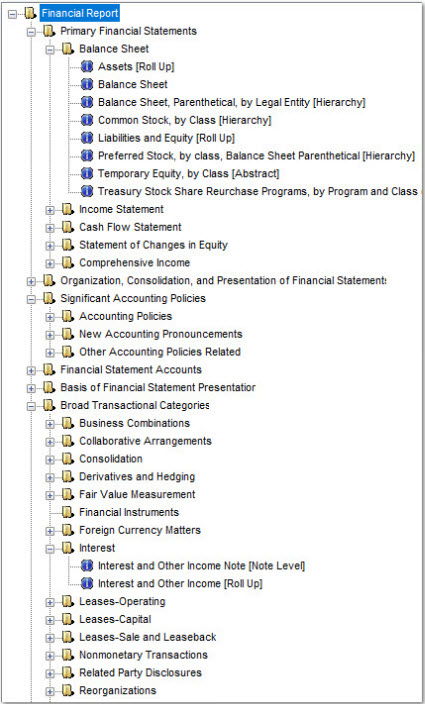

This is a prototype of disclosures organized within a hierarchy of topics:

That is a prototype that I created for US GAAP. I also have prototypes for IFRS and something that I call the XASB reporting scheme that I use for testing and prototyping.

The most important thing to realize here is not about the "templates" or "exemplars" that you see. The most important idea is to recognize that what I created was a FRAMEWORK. The framework is tested using US GAAP, IFRS, and XASB reporting scheme. I don't have the disclosures for any one reporting scheme, US GAAP or IFRS fully complete. What I have is some really comprehensive prototypes.

There is one other piece that is critical to understand that helps you see that what a software engineer and I are doing will work. That idea is what I call the "block". I will explain the block and how all these pieces fit together in future block posts, so stay tuned.

If you are curious or want additional details, please read the document Putting the Expertise into an XBRL-based Knowledge Based System for Creating Financial Reports.

Step-by-step, high-qualty XBRL-based digital financial reporting that works and is approachable by accounting professionals is becoming a reality.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Excellent Dashboard: US National Debt Clock

This US National Debt Clock is an excellent dashboard. From that dashboard you can get to the World Debt Clocks and the US State Debt Clocks.

Another Source for Measuring XBRL-based Report Quality

There is now a fourth source that has created capabilities for measuring/evaluating the quality of XBRL-based financial reports. Here is a list of the sources:

- My quality measurements: My quality measurements of XBRL-based financial reports submitted to the SEC.

- XBRL Cloud dashboard; XBRL Cloud's EDGAR Dashboard provides a broad spectrum of validation of XBRL-based reports submitted to the SEC.

- XBRLogic: XBRLogic now seems to provide quarterly measurements of the quality of XBRL-based financial reports submitted to the SEC. Provides a "quality" score and a "usability" score.

- XBRL US Data Quality Committee: Battery of about 46 different rules related to XBRL-based financial reports submitted to the SEC.

What would be very interesting is to combined the information from these sources to create a composite measurement of quality. XBRL Cloud comes the closest to that because they include my rules, XBRL US Data Quality Committee rules, Edger Filer Manual Rules, XBRL technical syntax rules, and other rules.

Maybe I will work on that. Perhaps this composite measurement could be done as of March 31 each year, after the 10-K filing season.

For more information related to XBRL-based report quality see Blueprint for Creating Zero-defect XBRL-based Digital Financial Reports.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print