BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from September 1, 2017 - September 30, 2017

IASB Chairman: The times, they are a-changin’

Chairman of the International Accounting Standards Board Hans Hoogervorst delivered a speech on the future of corporate reporting.

In that speech the chairman said the IASB is ready to adapt to the changing world of corporate reporting by increasing the communication effectiveness of the financial statements, facilitating electronic consumption of financial data and by promoting integrated reporting (including social responsibility reporting and environmental sustainability reporting.

Maybe it is time for professional accountants to get ready for digital financial reporting, accounting, and auditing.

In that speech, the chairman made these comments about the IFRS XBRL Taxonomy and digital financial reporting (emphasis was added):

Better formatting of the primary statements should also facilitate digital reporting. This brings me to the third element of Better Communication, which looks at the changing nature of the consumption of financial information. Increasingly, investors are using electronic means to digest financial information, often produced by data aggregators. To enhance the quality of electronically provided data, it is imperative that the IFRS Foundation continues to develop its IFRS Taxonomy.

The IFRS Taxonomy is already used by a wide variety of market participants and regulators. It is on the verge of making a new quantum leap. The US Securities and Exchange Commission has recently mandated the IFRS Taxonomy for the filing of company reports by foreign private issuers. The European Securities and Markets Authority (ESMA) is looking to do the same in Europe; a proposition that seems to be broadly supported by influential ESMA stakeholders.

I think these developments can do much to improve the accessibility of digital financial information to investors. In addition, it can contribute to improving the quality of IFRS information in the data provided by, for example, the data aggregators. In turn, once regulatory filings become digitised, this will open up a wealth of information about how IFRS Standards are used in practice. The feedback from regulatory filings might inform us, for example, on the formatting decisions we need to take in our project to improve the Primary Financial Statements.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

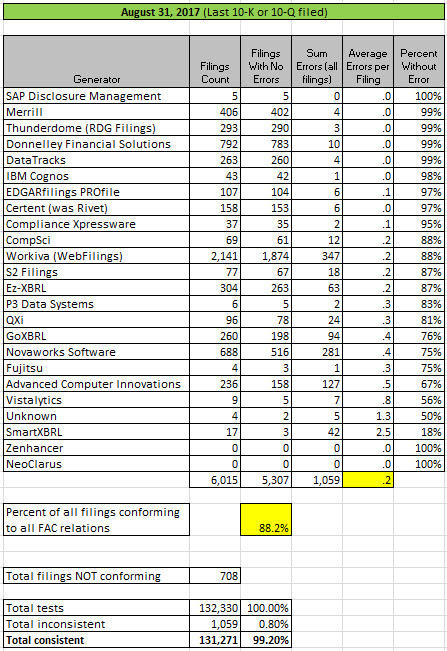

Quarterly XBRL-based Public Company Financial Report Quality Measurement

The graphic below shows the results of my quarterly fundamental accounting concept relations continuity cross checks of XBRL-based financial reports of public companies which are submitted to the SEC.

I have been measuring specific fundamental accounting information of public company XBRL-based financial reports being submitted to the SEC for going on four years now. The quality of the information reported continually increases each time measurements are taken, which is a good sign.

But now in addition; what I am seeing is a specific set of filing agents/software vendors which have repeatable processes which are beginning to consistently yield high quality results per my specific measurements. In the graphic below you can see that Merrill, Thunderdome (RDG Filings), Donnelley Financial Solutions, and DataTracks each are creating 99% of the XBRL-based public company financial reports which are completely consistent with my full set of fundamental accounting concept relations continuity cross checks.

Those four filing agents/software vendors represent almost 30% of all public company filings to the SEC. Another four filing agents/software vendors are closing in on 99% of all their XBRL-based reports being consistent with these basic accounting relations.

This is NOT to say that entire reports are correct or that 99%, which is only approaching Sigma Level 4, is sufficient. My view is that the appropriate quality target is Sigma Level 6 which equates to 99.99966%. The important piece of information, I believe, is that reliable and repeatable processes are beginning to appear from multiple software vendors/filing agents. That statement is verifiable using empirical evidence of 100% of the filer population. This provides good information about what it takes to get XBRL-based reporting which uses the full power of extensibility offered by XBRL to work reliably and predictably.

People might want to reach out to these software vendors/filing agents to see how they achieve these results.

(Click image for larger view)

(Click image for larger view)

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: May 31, 2017; March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

in Becoming an XBRL Master Craftsman, Digital Financial Reporting

|

Post a Comment

| Email

| Print