BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from May 28, 2017 - June 3, 2017

Public Company Quality Continues to Improve, Trend is Good

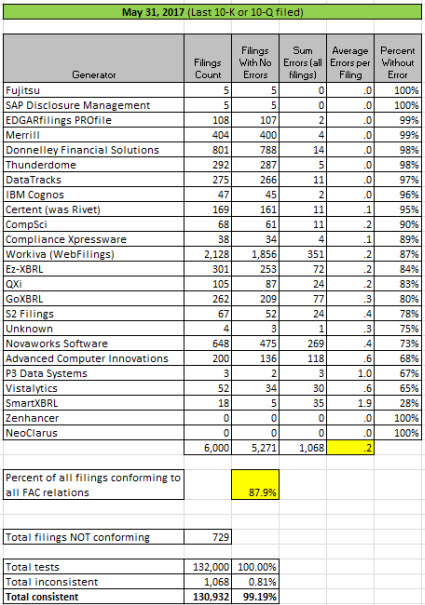

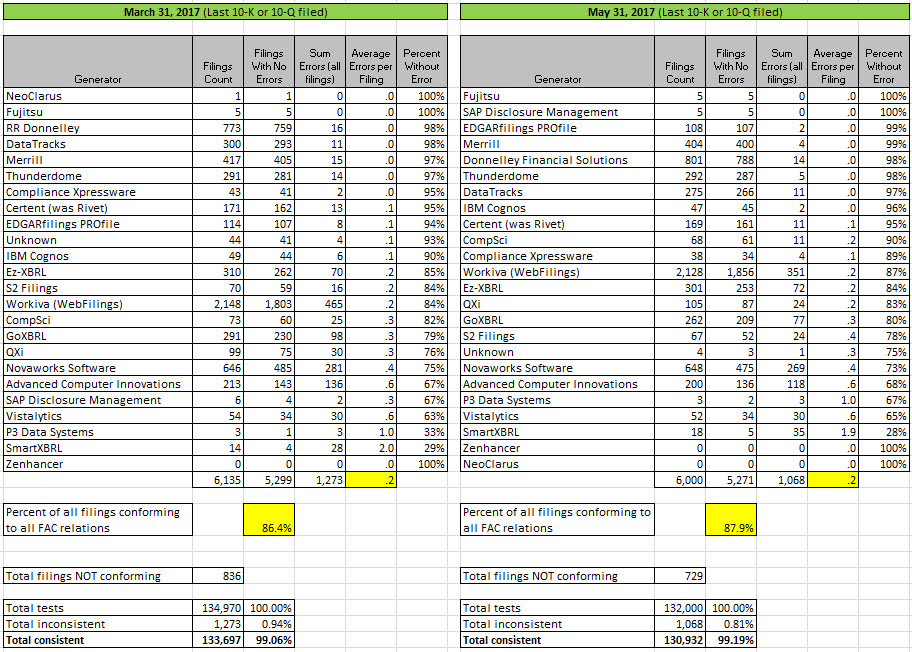

The quality improvement trend continues. There are currently 10 software generators and filing agents that have 90% or more of their XBRL-based public company financial reports consistent with all of the fundamental accounting concept relations continuity cross-checks. Average is 87.9%. On a per test basis, 99.19% of all relations are consistent with expectation.

Here are the current results of my measurements:

The biggest notable item is that Workiva went from 84% consistency to 87% consistency, fixing about 114 specific errors.

(Click image for larger view)

(Click image for larger view)

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Garry Kasparov: Don't fear intelligent machines. Work with them.

Who is the world chess champion today; a computer or a human? In 1997, IBM's Deep Blue took the title. Today, a computer is no longer the world chess champion. Neither is a human. Today, a team of computers and humans working together can beat any computer or any human working alone.

That is how the power of computers will be harnessed; by human and computer teamwork. Human are good at some tasks; not as good at other tasks. Computers are good at some tasks; not as good at other tasks. Teaming humans and computers together and leveraging the strengths of each is how work will get done in the future.

This TED Video, Garry Kasparov: Don't fear intelligent machines. Work with them, helps you recognize that human-machine partnerships is the way work will be done in the future. It also helps you recognize that you need to understand how to partner with machines.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

Excellent Learning Opportunity: Creating IFRS Templates, Examples, Metadata

I am working with a small group of people who are creating for IFRS what I created for US GAAP and for a general reporting scheme example that I created called XASB.

This is an excellent learning opportunity for professional accountants. Software vendors can also learn from this and test their software using the IFRS, US GAAP and XASB examples.

What we are going to do is create all the stuff that makes this expert systemwork for an IFRS-based financial report. To do that, we need to create what is described in this Blueprint for Creating Zero-Defect XBRL-based Digital Financial Reports.

I have a lot of the pieces already. The pieces just need to be more completely built out and tested. Below are all the existing pieces that I have for IFRS and the equivalent pieces for US GAAP and the XASB prototype:

- IFRS template library: A template library is simply a set of example disclosures for fragments of a financial report. (US GAAP equivlent; XASB does not have a template library).

- IFRS reference implementation: The reference implementation tests all the rules to make sure that everything works as expected. (US GAAP equivalent, XASB equivalent)

- IFRS model structure relations: The model structure tests the relationships between the Networks, Tables (or hypercubes), Axes (or dimensions), Members, Line items (or primary items), and concepts that make up the XBRL presentation relations of an XBRL taxonomy. (US GAAP equivalent, XASB equivalent)

- IFRS type or class relations: The type or class relations test how specific concepts are used relative to other specific concepts. (US GAAP equivalent, XASB equivalent)

- IFRS fundamental accounting concept relations: The fundamental accounting concept relations are continuity tests to make sure concepts are used correctly relative to other concepts in a report. (US GAAP equivalent; XASB equivalent)

- IFRS disclosure mechanics: The disclosure mechanics rules test the logical, structural, and specific mathematical relations related to specific disclosures. (US GAAP equivalent, XASB equivalent)

- IFRS reporting checklist: The reporting checklist rules test for the existence of specific disclosures relative to certain reported line items or relative to other reported disclosures. (US GAAP equivalent, XASB equivalent)

- IFRS disclosures: The disclosures is simply things that can be disclosed. (US GAAP equivalent, XASB equivalent)

- IFRS topics: The topics are simply ways of grouping disclosures. (US GAAP equivalent, XASB equivalent)

- IFRS disclosure exemplars: An exemplar is simply an example of how to create a disclosure. (US GAAP equivalent, XASB does not provide this)

I have been working with a software developer and we have a working expert systemthat is driven by the above metadata. The US GAAP and XASB metadata is all tested and works. Some of the IFRS stuff works.

Another thing that I want to test out is digital distributed ledgers. What I am going to do is offer POINTS or TOKENS to those that contribute to creating the IFRS metadata. With those POINTS or TOKENS, you can get a license to the expert system software and software support. I still have to work out details, but basically the more you contribute, the more you will learn, and the better the software license you can earn and you can get earlier versions of the expert system software.

Interested in participating and positioning your self well for the future? Send me an email (Charles.Hoffman@me.com) and I will put you on my distribution list. Slots are limited.

As is said, "The best way to predict the future is to create it." (Abraham Lincoln)

Also, "I skate to where the puck is going to be, not where it has been." (Wayne Gretzky)

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print