BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from December 1, 2017 - December 31, 2017

Making the Case for Reporting Styles

There is a method to my madness. In the document Making the Case for Reporting Styles I am trying to tie together many things that might appear to be separate. Here is the executive summary:

- Reporting styles is an example of the type of metadata that will drive the digital age of accounting, reporting, and auditing.

- Financial reports are not forms, but they are not random either.

- The fragments that make up a financial report can be distilled down to high-level patterns.

- One example of such high-level patterns is the reporting styles of the primary financial statements of public companies.

- The high-level patterns offer leverage helpful in both the creation of financial reports and the querying of information the reports contain.

- Software leveraging these high-level patterns can be constructed which is easier to use than software which does not leverage the patterns.

- The exercise of creating reporting styles for 100% of all public companies helps discover and correct accounting errors made by public companies and ambiguity in US GAAP.

- The reporting styles of the primary financial statements is only an example of high-level patterns; patterns exist within every disclosure also.

- The campaign to improve disclosure quality will do for the rest of the financial report what the reporting styles and fundamental accounting concepts did for the primary financial statements.

- While these ideas have been proven using US GAAP based financial reporting which is probably the most complex business reporting use case; other financial reporting schemes such as IFRS can likely use these ideas as can other business reporting use cases.

I am getting closer and closer to being able to effectively explain what I am trying to explain for probably 15 years now. The first step is understanding it myself.

Charlie

in Becoming an XBRL Master Craftsman

|

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

Benard Lund: Shy XBRL emerges blinking onto the Blockchain Economy stage to power Equity Tokens

Benard Lund explains why XBRL will power equity tokens on blockchain, Shy XBRL emerges blinking onto the Blockchain Economy stage to power Equity Tokens.

Download Information Extraction Prototype

I updated a prototype application that I created for extracting information from XBRL-based financial reports submitted to the SEC. It is an Excel spreadsheet application. You can download the application which is contained in this ZIP archive.

Just press the button "Compare all on List" on the "Compare" sheet. What will happen is the application will extract information from 375 financial reports from banks. It takes about 3 minutes to run depending on you Internet connection speed.

What happens is that information for each bank is loaded into a row in the spreadsheet. Notice that there are ZERO ERRORS in the data. The reason for that is that I selected only banks that had no errors in their information.

This is an excellent learning tool if you want to reverse-engineer how to extract information.

Email me if you have any questions.

Charlie

in Digital Financial Reporting

|

Post a Comment

| Email

| Print

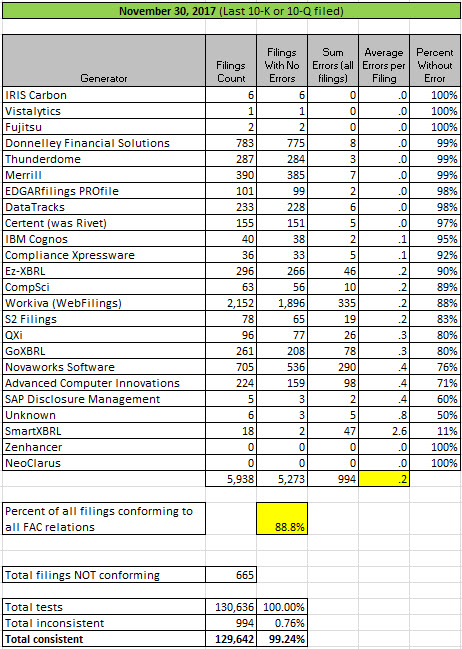

Quarterly XBRL-based Public Company Financial Report Quality Measurement (Nov 2017)

The graphic below shows the results of my quarterly measurements of fundamental accounting concept relations continuity cross checks of XBRL-based financial reports of public companies which are submitted to the SEC.

I have been measuring specific fundamental accounting information of public company XBRL-based financial reports being submitted to the SEC for going on four years now. The quality of the information reported continually improves each time measurements are taken, which is a good sign.

Highlights for this quarter include three new filing agents/software vendors that have reached the point where 90% or more of the XBRL-based reports they create are consistent with all of my business rules: Compliance Xpressware, EZ-XBRL, and IRIS Carbon.

You can download a ZIP file that contains an Excel spreadsheet that a list of all 994 errors.

Here is a comparison of March, August, and November 2017.

Information Extraction Prototype: Lets you extract data from 375 XBRL-based financial reports, Download ZIP Archive containing Excel spreadsheet

(Click for larger image)

(Click for larger image)

Here are the errors by test:

Click image for larger view)

Click image for larger view)

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: August 31, 2017; May 31, 2017; March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Charlie

|

Post a Comment

|

1 Reference

| Email

| Print

1 Reference

| Email

| Print