BLOG: Digital Financial Reporting

This is a blog for information relating to digital financial reporting. This blog is basically my "lab notebook" for experimenting and learning about XBRL-based digital financial reporting. This is my brain storming platform. This is where I think out loud (i.e. publicly) about digital financial reporting. This information is for innovators and early adopters who are ushering in a new era of accounting, reporting, auditing, and analysis in a digital environment.

Much of the information contained in this blog is synthasized, summarized, condensed, better organized and articulated in my book XBRL for Dummies and in the chapters of Intelligent XBRL-based Digital Financial Reporting. If you have any questions, feel free to contact me.

Entries from June 1, 2018 - June 30, 2018

Quarterly XBRL-based Public Company Financial Report Quality Measurement (June 2018)

The following is a summary of the quality measurements of XBRL-based US GAAP financial reports submitted to the SEC as of June 30, 2018. The following Excel spreadsheets and other documents provide details related to these quality measurements:

- Positive results from tests (i.e. proof): Set of Excel spreadsheets contained in a ZIP archive that lets you duplicate testing, proving that over

- Negative results from tests (i.e. confirmed errors): Details of 100% of the confirmed errors. 974 errors contained with 639 filings.

- Accounting errors discovered during validation process: This PDF provides details of rather obvious accounting errors that exist in the financial reports of public companies. This validation process leads to the detection of such errors.

- Prototype validation tools: Some working prototype, proof-of-concept validation tools you can use. Only provided for one reporting style. I added a "line of reasoning" text file that helps you review the validation results.

- US GAAP Rules: Current publicly available version of the validation rules by reporting style for US GAAP. As of March 31, 2018. Contact me if you want the most current version.

- IFRS Rules: Current publicly available version of the validation rules by reporting style for IFRS.

- Templates: A financial report can be broken down into fragments. The same techniques for validating the primary financial statements also applies to other disclosures, only the rules are different.

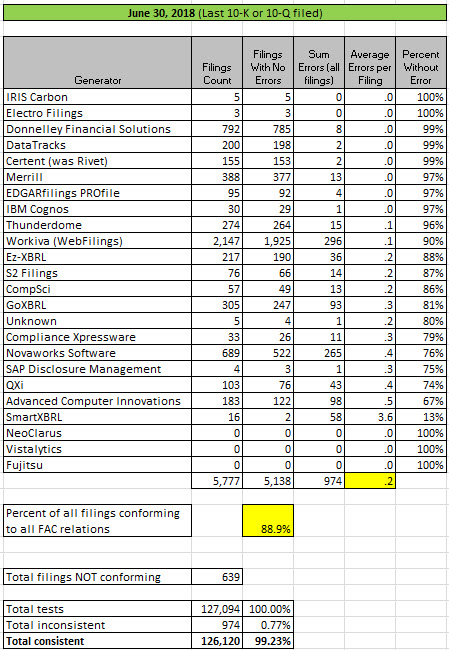

US GAAP fundamental accounting concept relations continuity cross check validation results for last 10-K or 10-Q filed by generator of the report as of June 30, 2018:

(Click image for larger view)

(Click image for larger view)

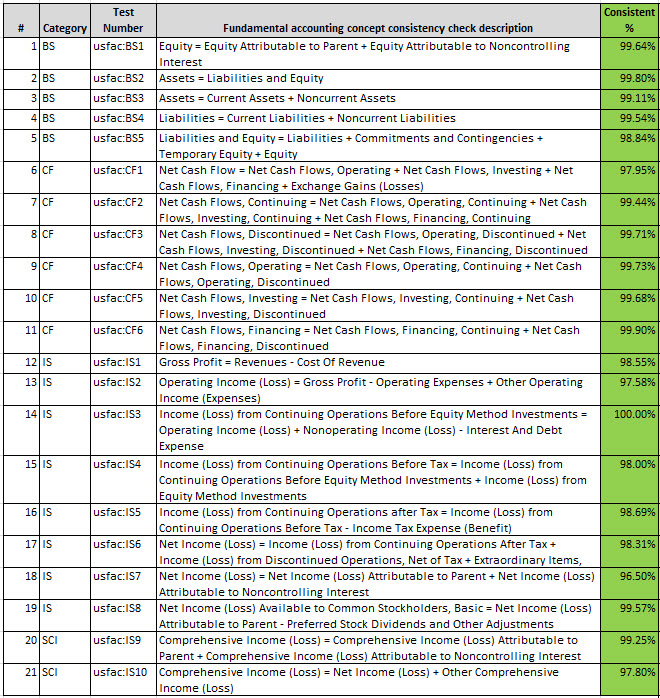

US GAAP fundamental accounting concept relations continuity cross check by logical accounting relation tested (same filings as above):

(Click image for larger view)

(Click image for larger view)

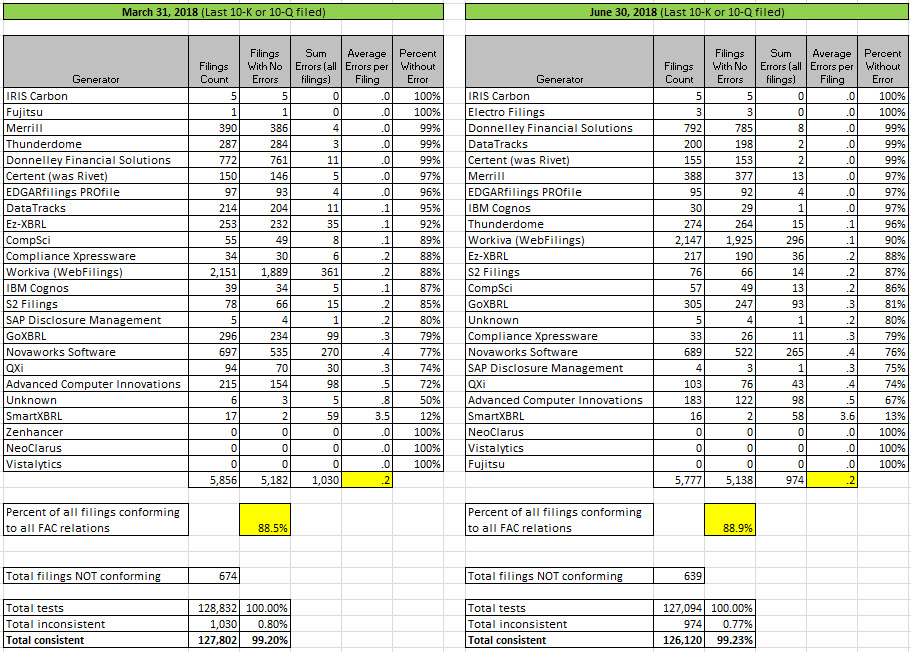

Comparison of the prior results as of March 31, 2018 and the current results as of June 30, 2018 by generator:

(Click image for larger view)

(Click image for larger view)

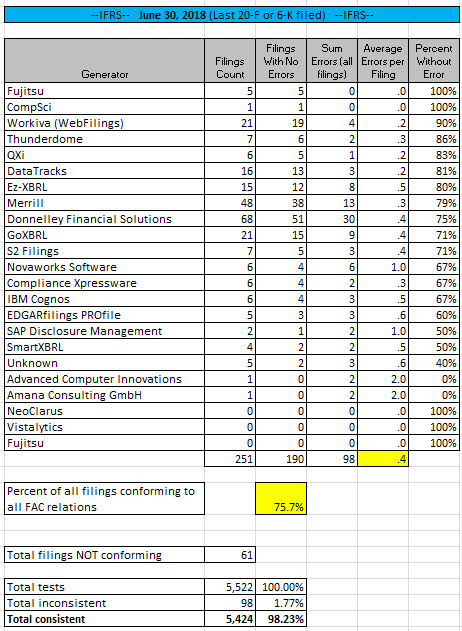

NEW!!! IFRS Fundamental Accounting Concept Relations (Work in Progress) I am going to start testing IFRS filings also! These results are a work in progress but very accurate. I have all the balance sheet and cash flow statement reporting styles working; but I only have a couple of the income statement reporting styles working.

(Click Image for Larger View)

(Click Image for Larger View)

**********************PRIOR RESULTS**********************

Previous fundamental accounting concept relations consistency results reported: March 31, 2018; November 30, 2017; August 31, 2017; May 31, 2017; March 31, 2017; November 28, 2016; August 31, 2016; June 30, 2016; March 31, 2016; February 29, 2016; January 31, 2016; December 31, 3015; November 30, 2015; October 31, 2015; September 30, 2015; August 31, 2015; July 31, 2015; June 30, 2015; May 29, 2015; April 1, 2015; November 29, 2014.

Information helpful to understanding errors, learn how to create quality XBRL-based digital financial reports.

Blueprint for Creating Zero-defect XBRL-based Digital Financial Reports, helps you understand how to test other aspects of a digital financial report.

Computer Empathy, the best way to get dialed into accounting, reporting, auditing, and analysis in a digital environment.

McKinsey: Five lessons from history on AI, automation, and employment

In the article Five lessons from history on AI, automation, and employment, Susan Lund and James Manyika provide a framework to think about the changes that AI will bring to the accounting profession over the coming years.

Charlie

in Digital Financial Reporting

|

Charlie

in Digital Financial Reporting

|

Post a Comment

|

Post a Comment

|  Email

|

Email

|  Print

Print

SEC published draft Strategic Plan for 2018-2022

The Securities and Exchange Commission have published a draft strategic plan for 2018 to 2022. The strategic plan summarizes the SEC's mission, vision, values, and goals.

Charlie

in Creating Investor Friendly SEC XBRL Filings

|

Post a Comment

| Email

| Print

Understanding Reporting Styles

I used to call them "reporting frames" or "reporting pallets". Now I call them "reporting styles". If you want to understand reporting styles, read this document.

I built the US GAAP reporting styles first. Now I am creating IFRS reporting styles. Here are both sets:

One thing that I want to revise is the coding scheme that I use. The coding scheme that I have now for US GAAP just evolved as I methodically created the reposting styles. Now that I see all the moving parts, in retrospect I wish I would have done a few things differently. I am going to make those changes for IFRS. I have not done so yet, but I am going to go back and revise the coding scheme.

Another thing that I am recognizing is that these fundamental accounting concept relationships and the reporting styles are not only useful for validating XBRL-based reports to make sure they are created correctly; the machine-readable metadata is also useful for extracting information from the filings AND for doing comparisons between IFRS and US GAAP reports.

Here are the mappings for one reporting style for US GAAP. And here are mappings for that same reporting style for IFRS. The IFRS and US GAAP concepts are different; but the FAC (fundamental accounting concepts) are the same. Unfortunately, I used different schemas and different namespaces for IFRS and US GAAP. I will fix that.

So, here are the impute rules and consistency cross check rules: IFRS | US GAAP. Those rules are essentially the same. There are a couple of differences because IFRS does not use "commitments and contingencies" and "temporary equity" as US GAAP does. (Note that extraordinary items was dropped from US GAAP, so that needs to be removed from my FAC concepts and rules.)

Basically, I believe that I can create one set of impute/consistency rules that will work for US GAAP and IFRS for some reporting styles. For others, probably not. Time will tell.

Also, note that the versions above use the OLD SYNTAX of articulating the impute and consistency cross check rules. Note that the rules are basically a controlled natural language with information stored in a text file.

The NEW SYNTAX is 100% pure XBRL. Here is the new style for both US GAAP and IFRS:

- US GAAP (Currently supports the most used 67 of the approximately 99 reporting styles that exist in the old syntax.)

- IFRS (Currently supports only ONE reporting style for the new syntax; that was created to test the new syntax and make sure I was creating these correctly in our software.)

If this is a bit confusing, sorry. I am figuring this stuff out as I create it. That is how it works being on the leading edge. Sometimes you have to backtrack because you went the wrong way.

Charlie

in Becoming an XBRL Master Craftsman

|

Post a Comment

| Email

| Print

Future ESMA Filers Currently Filing with SEC

So this is a work in progress, but I am posting where I am thus far.

As it has been explained to me, there are 86 companies that submit form 20-F filings to the SEC using the XBRL format that will ultimately be submitting the same information or very similar information to the ESMA.

Of that 86, there are 56 that I have reliable rules for and the companies pass 100% of my fundamental accounting concept relations continuity cross checks.

To verify those 86 filings, and the full set of about 253 IFRS filings, I have created as set of reporting styles and the related machine-readable rules to automatically verify that the reports are following those reporting styles. NOTE!!! The IMPUTE and CONSISTENCY rules are in an OLDER FORMAT that is not XBRL currently. I am doing this becuase XBRL Cloud uses the OLDER FORMAT and I am using XBRL Cloud to help me create these rules. But, I do have the NEW 100% pure XBRL Format. I will convert all the IFRS fundamental accounting concept relations continuity cross checks to the pure XBRL format.

Ultimatly, I will have all the same sorts of rules for US GAAP and IFRS that are covered in this document. If you don't understand why I am going through all this trouble, then read the Computer Empathy document.

This blog post will help you understand where I am going. Particularly this for IFRS and this for US GAAP. This video walks you through what you can do with that information. But don't think just human-readable. Think human-readable AND machine-readable. And XBRL will be used to link everything together.

This extraction tool grabs information from the 88 companies financial reports. The tool is not working 100% correctly yet. I still need to figure out the business rules to extract information from the filings.

But ask yourself a question; or ask the ESMA: How do you know the whole extracting information from XBRL-based reports actually works? What proof do you have? That seems like a reasonable question given that companies spend a lot of time representing information in the XBRL format. If this is not achievable for these 88 XBRL-based financial reports, then why would you think it would be achievable from the full set of companies that will be required to report to the ESMA using XBRL?